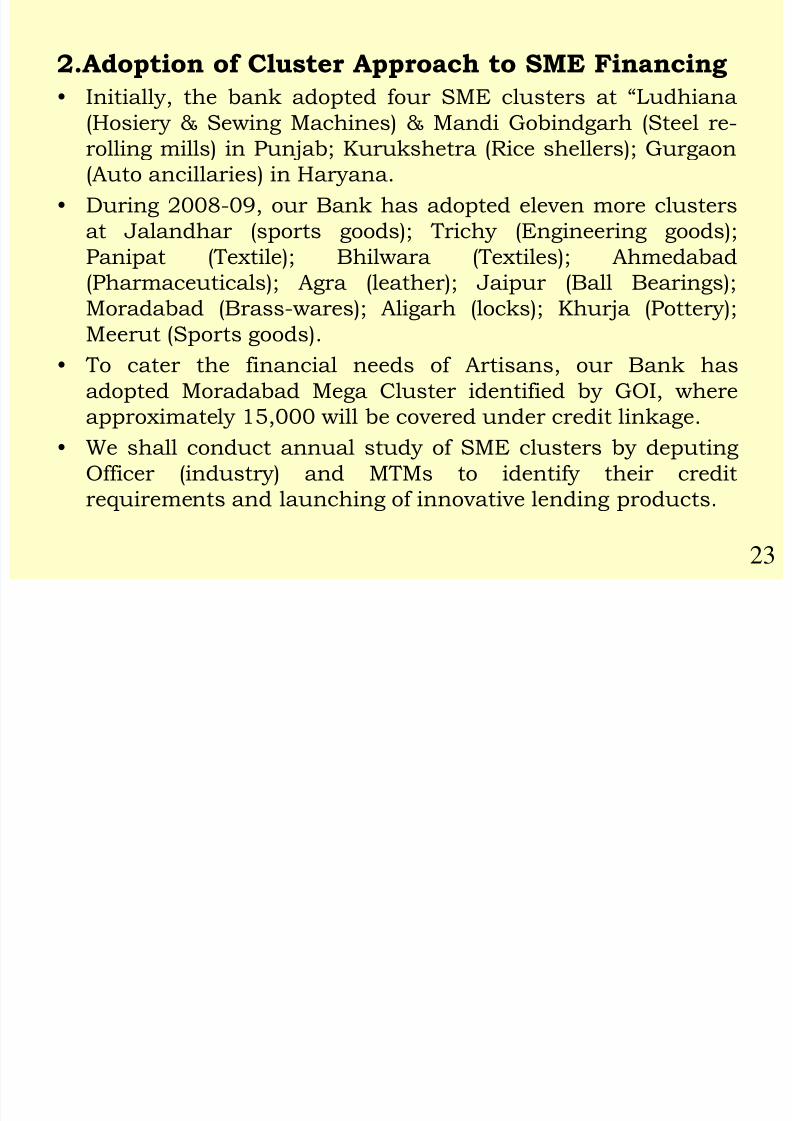

8-SME 30092009

102

1 Presentation On Micro, Small & Medium Enterprises

-

Upload

rishabh-bajpai -

Category

Documents

-

view

223 -

download

0

Transcript of 8-SME 30092009

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 1/102

1

PresentationOn

Micro, Small & Medium

Enterprises

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 2/102

The Small & Medium Enterprisesare critical to the nation’s economy – they contribute

approximately 40% of India’s domestic production,almost 50% of the total exports and 45% of Industrial

Employment. More important, they are the second

largest manpower employer overall after Agriculture.

SME in India are mostly in un-organised sector and

are the source of livelihood for millions of people. The

social contribution made by SMEs is even more

significant than its economic contribution. Within

SME sector, the Small Enterprises sector serves as

seed-bed for nurturing entrepreneurial talent and

originating units to grow eventually to Medium &

Large Enterprises.

2

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 3/102

3

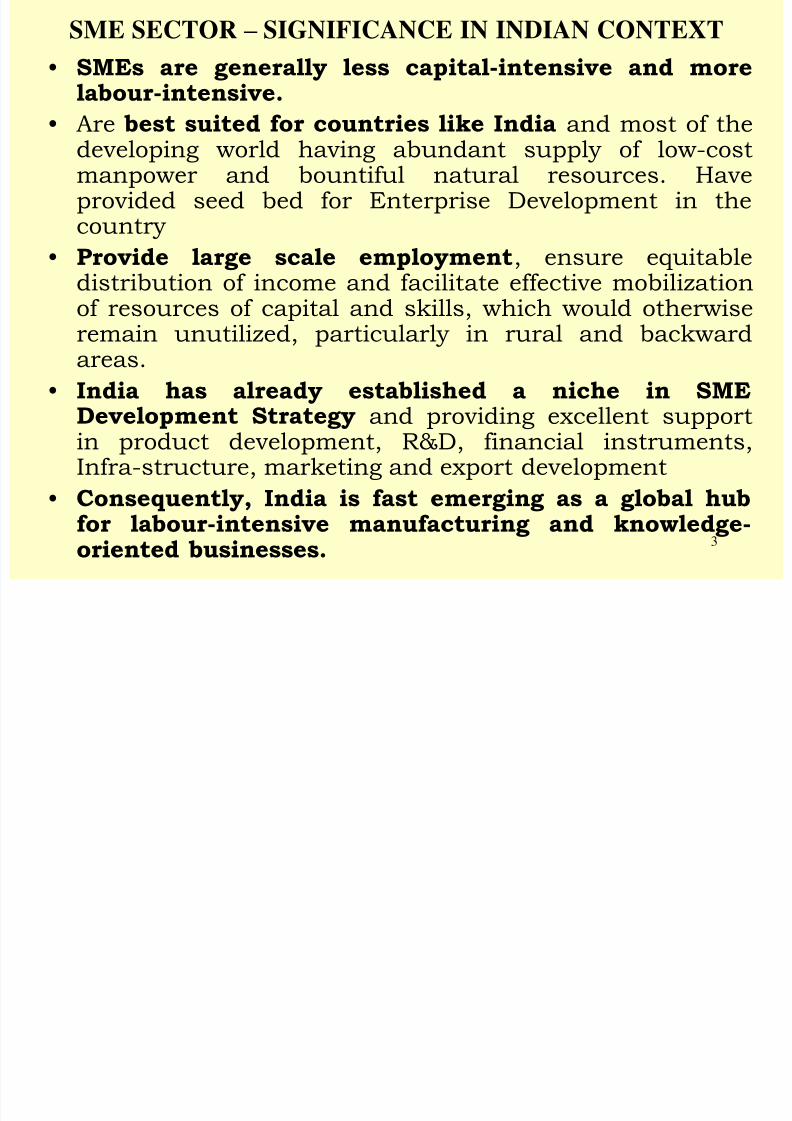

SME SECTOR – SIGNIFICANCE IN INDIAN CONTEXT

• SMEs are generally less capital-intensive and morelabour-intensive.

• Are best suited for countries like India and most of thedeveloping world having abundant supply of low-costmanpower and bountiful natural resources. Haveprovided seed bed for Enterprise Development in thecountry

• Provide large scale employment, ensure equitabledistribution of income and facilitate effective mobilizationof resources of capital and skills, which would otherwiseremain unutilized, particularly in rural and backwardareas.

• India has already established a niche in SMEDevelopment Strategy and providing excellent supportin product development, R&D, financial instruments,Infra-structure, marketing and export development

• Consequently, India is fast emerging as a global hubfor labour-intensive manufacturing and knowledge-

oriented businesses.

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 4/102

Back DropHighlights of SMEs; Born out of Individual initiatives & skills.

Operational flexibility.

Low cost of production.

High propensity to adopt technology.

High capacity to innovate and exports.

High employment orientation.

Utilisation of locally available human and material

sources. Reduction of regional imbalance.

4

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 5/102

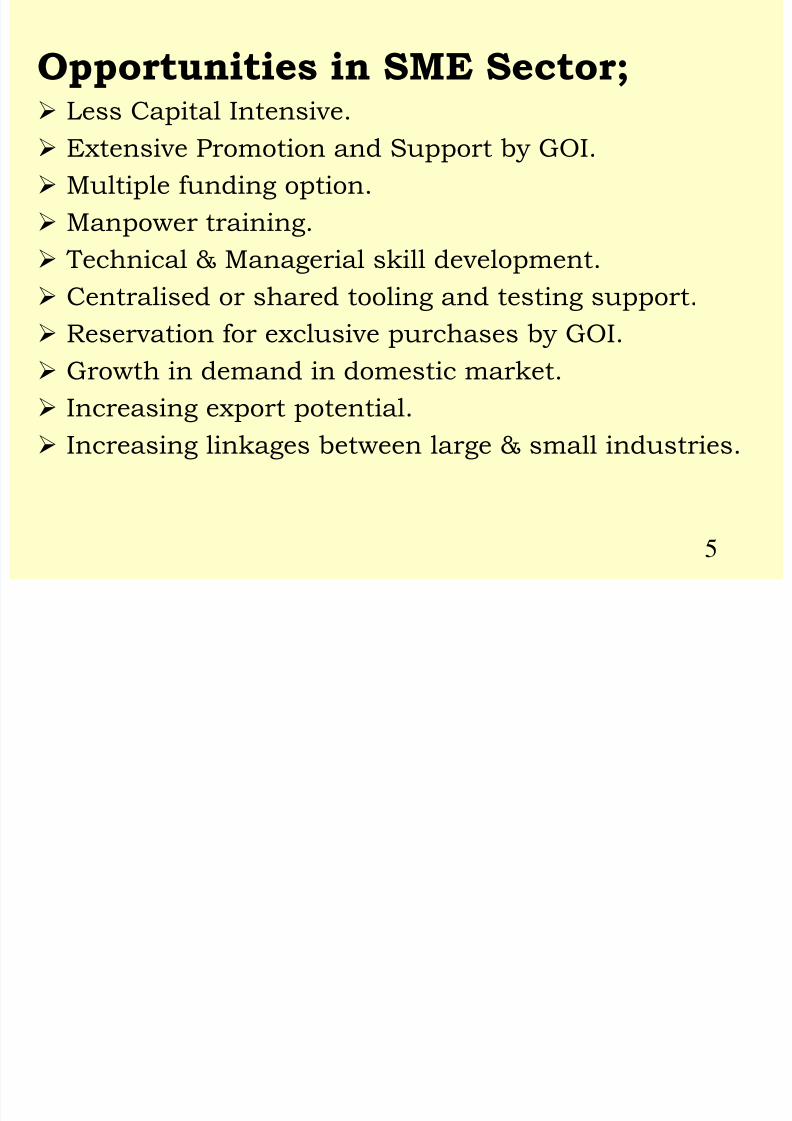

Opportunities in SME Sector; Less Capital Intensive.

Extensive Promotion and Support by GOI.

Multiple funding option.

Manpower training.

Technical & Managerial skill development.

Centralised or shared tooling and testing support.

Reservation for exclusive purchases by GOI.

Growth in demand in domestic market.

Increasing export potential. Increasing linkages between large & small industries.

5

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 6/102

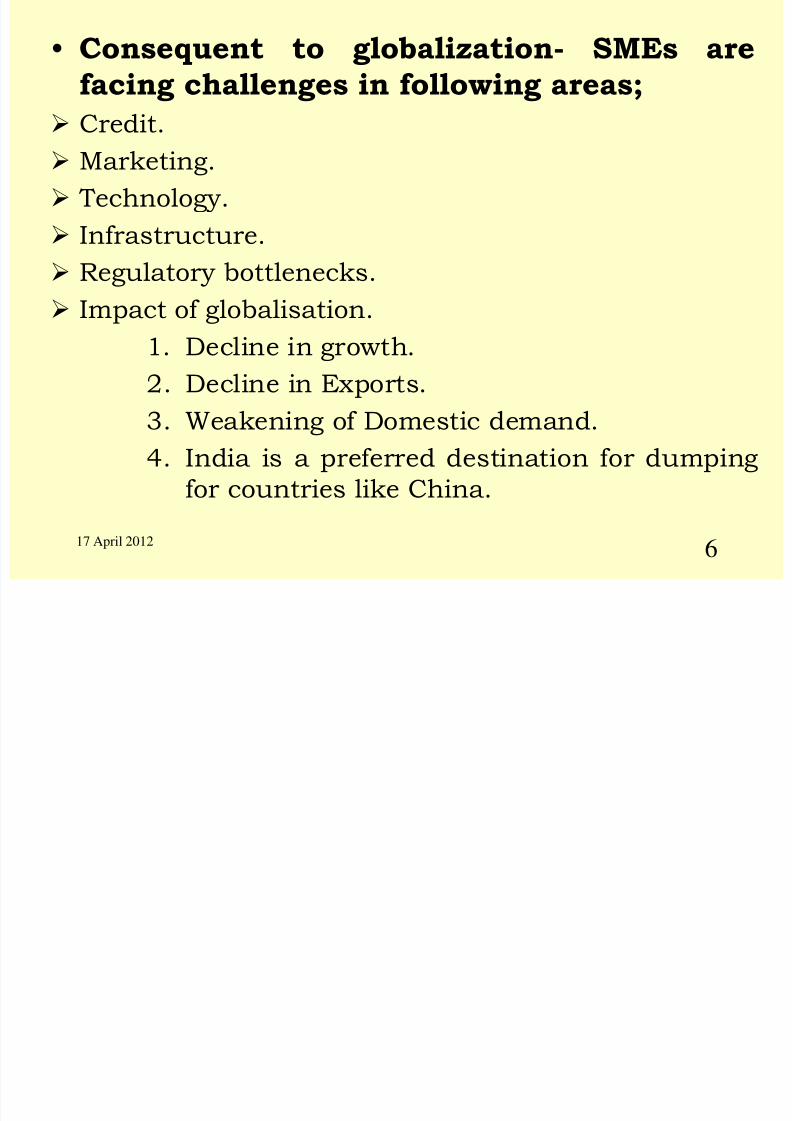

• Consequent to globalization- SMEs are

facing challenges in following areas;

Credit.

Marketing.

Technology.

Infrastructure.

Regulatory bottlenecks. Impact of globalisation.

1. Decline in growth.

2. Decline in Exports.

3. Weakening of Domestic demand.

4. India is a preferred destination for dumping

for countries like China.

17 April 2012 6

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 7/102

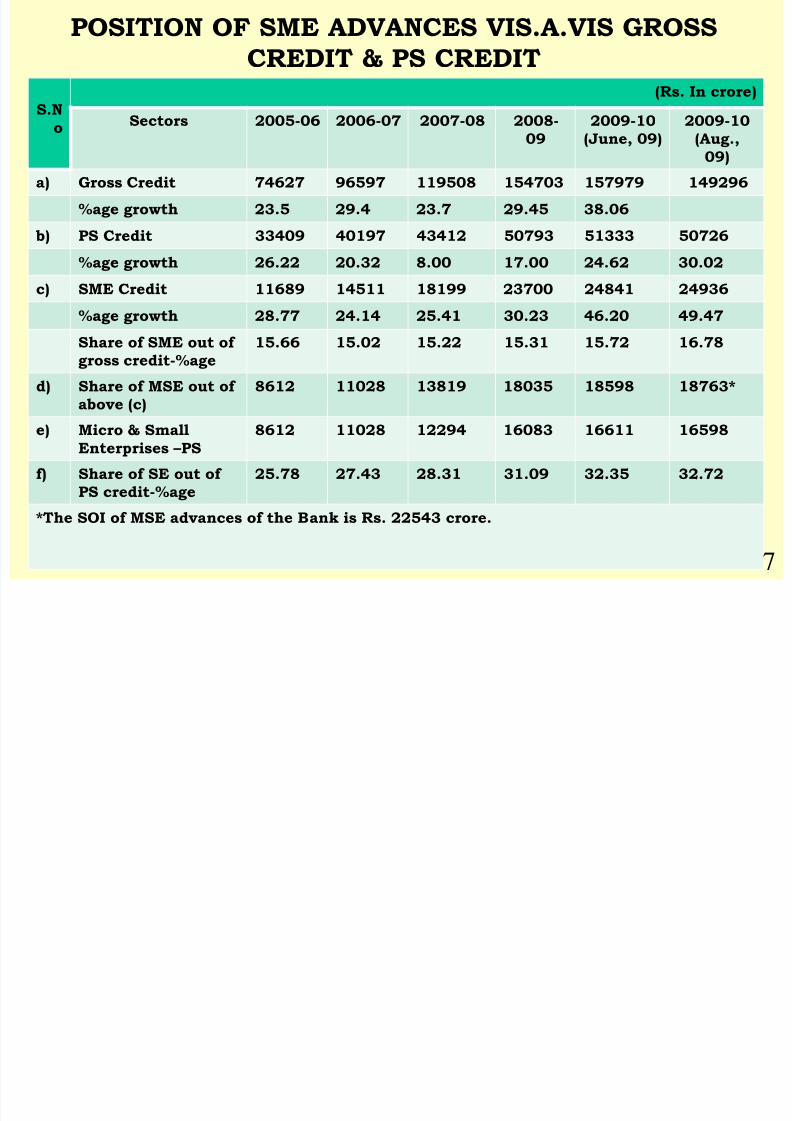

POSITION OF SME ADVANCES VIS.A.VIS GROSS

CREDIT & PS CREDIT

S.N

o

(Rs. In crore)

Sectors 2005-06 2006-07 2007-08 2008-

09

2009-10

(June, 09)

2009-10

(Aug.,09)

a) Gross Credit 74627 96597 119508 154703 157979 149296

%age growth 23.5 29.4 23.7 29.45 38.06

b) PS Credit 33409 40197 43412 50793 51333 50726

%age growth 26.22 20.32 8.00 17.00 24.62 30.02

c) SME Credit 11689 14511 18199 23700 24841 24936

%age growth 28.77 24.14 25.41 30.23 46.20 49.47

Share of SME out of

gross credit-%age

15.66 15.02 15.22 15.31 15.72 16.78

d) Share of MSE out of

above (c)

8612 11028 13819 18035 18598 18763*

e) Micro & Small

Enterprises – PS

8612 11028 12294 16083 16611 16598

f) Share of SE out of

PS credit-%age

25.78 27.43 28.31 31.09 32.35 32.72

*The SOI of MSE advances of the Bank is Rs. 22543 crore.

7

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 8/102

ISSUES……….

• Lack in knowledge of;

1. Importance of MSME sector in financing.2. Schemes/products of Financing.

3. Details of Promotional schemes for MSME sector

like Credit Guarantee Scheme of CGTMSE, Soft

loan assistance scheme i.e National Equity Fund& Mahila Udyam Nidhi Yojana and incentive

scheme for obtention of ISO 9000 certification.

4. GOI subsidy/incentive benefits for technology

upgradation & modernisation under Textile & Jutesector (TUFS), Small Enterprises Sector in select

products/by products (CLCSS) and Food & agro

Processing sector extended to these sectors through

Banks.

8

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 9/102

Cont…. 5. Branches not offering focused approach towards

financing of Service Sector activities, as this sectoroffers comparatively large scope of financing

comparatively to Manufacturing Sector.

6. Despite simplification of appraisal system,

dependence on services of Technical Officers forproject appraisal even though in small cases.

9

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 10/102

Over view on SME

17 April 2012 10

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 11/10211

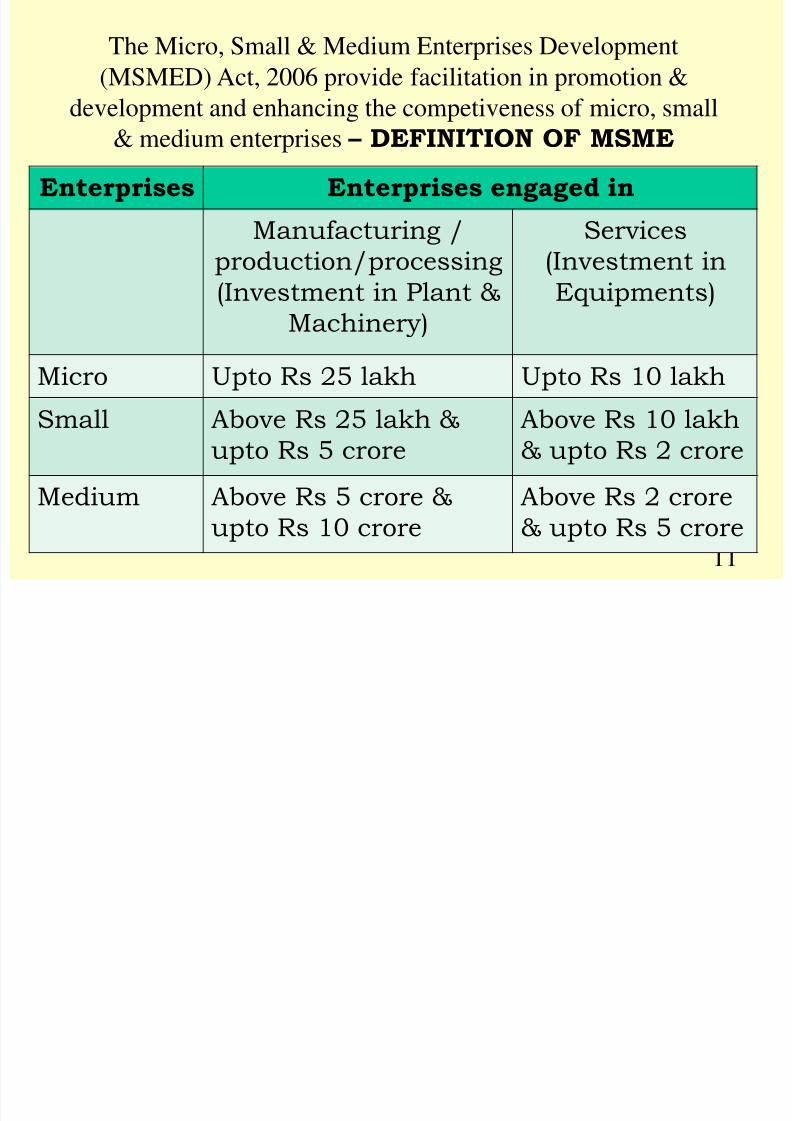

Enterprises Enterprises engaged in

Manufacturing /

production/processing(Investment in Plant &

Machinery)

Services

(Investment inEquipments)

Micro Upto Rs 25 lakh Upto Rs 10 lakh

Small Above Rs 25 lakh &

upto Rs 5 crore

Above Rs 10 lakh

& upto Rs 2 crore

Medium Above Rs 5 crore &

upto Rs 10 crore

Above Rs 2 crore

& upto Rs 5 crore

The Micro, Small & Medium Enterprises Development

(MSMED) Act, 2006 provide facilitation in promotion &

development and enhancing the competiveness of micro, small

& medium enterprises – DEFINITION OF MSME

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 12/102

The Scope of the MSMED Act, 2006 hasbeen enlarged by incorporating advances to

all business & Service activities under theambit of MSME sector like financing to Retail

Trade, Educational Institutes, Architects and

interior design consultants, Packaging &

Transport/taxi services, Event management, Travel & Tour operators, Storage & warehouse

services, Clearing & forwarding agents,

Telecom & communication services,

Healthcare centres, Hotel & Restaurants,

Coaching Centres, Publicity & media coverage

and Market research agencies. The illustrative

list of the service activity ………………………...

17 April 2012 12

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 13/102

Illustrative List of Service activities

1. Consultancy Services including Management Services

2. Renting of Agricultural Machinery (Harvesting)

3. Composite Broker Services in Risk and Insurance

Management

4. Third Party Administration (TPA) Services for Medical

Insurance Claims of Policy Holders

5. Seed Grading Services

6. Training-cum-Incubator Centres

7. Educational Institutions

8. Training Institutes

9. Retail Trade

10. Practice of Law, i.e., legal services

11. Trading in medical instruments (brand new)

12. Placement and Management Consultancy Services

17 April 2012 13

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 14/102

13. Advertising agency

14. Advances to Transport Sector

15. Advances to Small & Large Business activities

16. Advances to Professionals & Self Employed17. Nursing homes/clinics

18. Courier Services

19. Architecture Designers

20. Events Management

21. Catering

22. Gems & Jewellery designing

23. Equipment Rental & Leasing

24. Typing Centres

25. Xeroxing

26. Industrial Photography

27. Industrial R & D Labs.

28. Industrial Testing Labs

29. Desk Top publishing 14

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 15/102

30. Internet Browsing/Setting up of Cyber Cafes.

31. Auto Repair and service centers

32. Documentary Films on themes like Family Planning, Social forestry,

energy conservation and commercial advertising33. Laboratories engaged in Testing of Raw Materials, Finished Products

34. “Servicing Industry” Undertakings engaged in maintenance, repair, testing

or electronic / electrical equipment / instruments i.e. measuring / control

instruments servicing of all types of vehicles and machinery of any

description including televisions, tape recorders, VCRs, Radios,Transformers, Motors, Watches etc.

35. Laundry and Dry Cleaning

36. X-Ray Clinic

37. Tailoring, boutiques

38. Servicing of agriculture farm equipment e.g. Tractor, Pump, Rig, Boring

Machine etc.

39. Weight Bridge

40. Photographic Lab

41. Blue printing and enlargement of drawing / design facilities 15

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 16/102

42 ISD / STD Booths

43. Teleprinter / FAX Services

44. Sub-contracting Exchanges (SCXs) established by Industry Associations

45. Coloured or Black & White Studios equipped with processing laboratory46. Ropeways in hilly areas

47. Installation and operation of Cable TV Network

48. Operating EPABX under franchises

49. EDP Institutes established by Voluntary Associations / Non-Government

Organisations

50. Beauty Parlors and Crèches

16

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 17/102

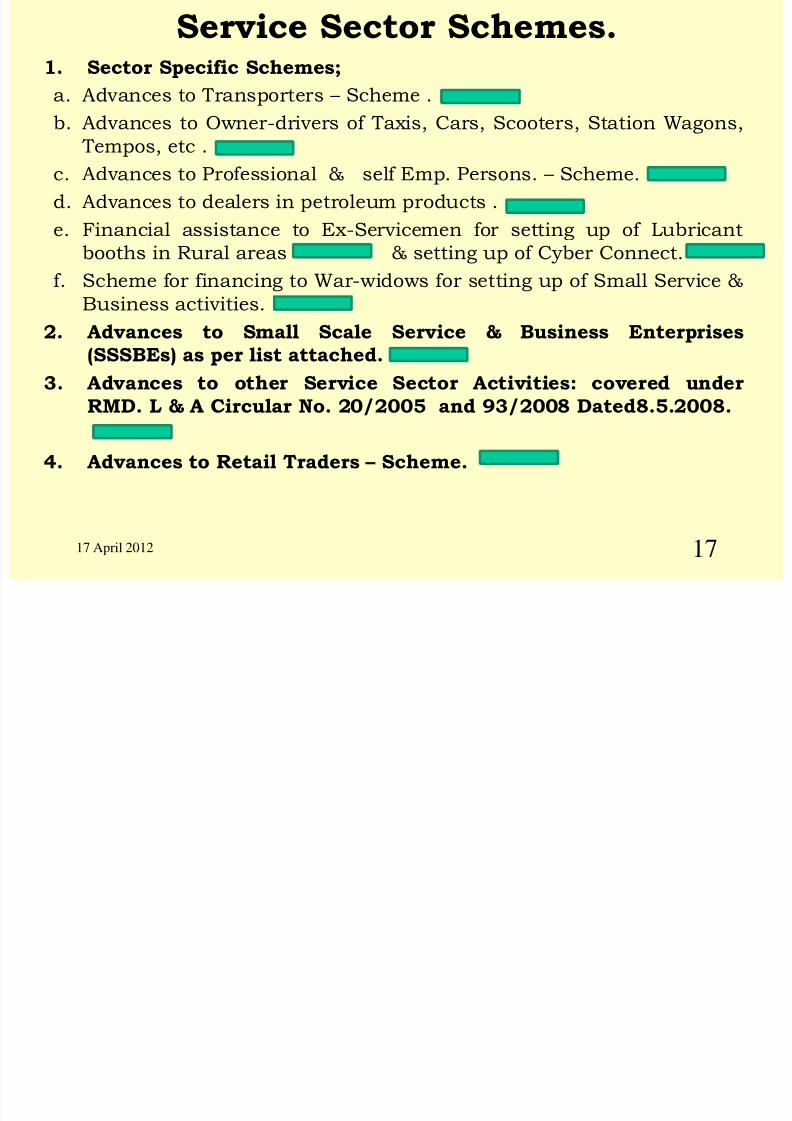

Service Sector Schemes.1. Sector Specific Schemes;

a. Advances to Transporters – Scheme .

b. Advances to Owner-drivers of Taxis, Cars, Scooters, Station Wagons,

Tempos, etc .

c. Advances to Professional & self Emp. Persons. – Scheme.

d. Advances to dealers in petroleum products .

e. Financial assistance to Ex-Servicemen for setting up of Lubricant

booths in Rural areas & setting up of Cyber Connect.

f. Scheme for financing to War-widows for setting up of Small Service &Business activities.

2. Advances to Small Scale Service & Business Enterprises(SSSBEs) as per list attached.

3. Advances to other Service Sector Activities: covered under

RMD. L & A Circular No. 20/2005 and 93/2008 Dated8.5.2008.

4. Advances to Retail Traders – Scheme.

17 April 2012 17

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 18/102

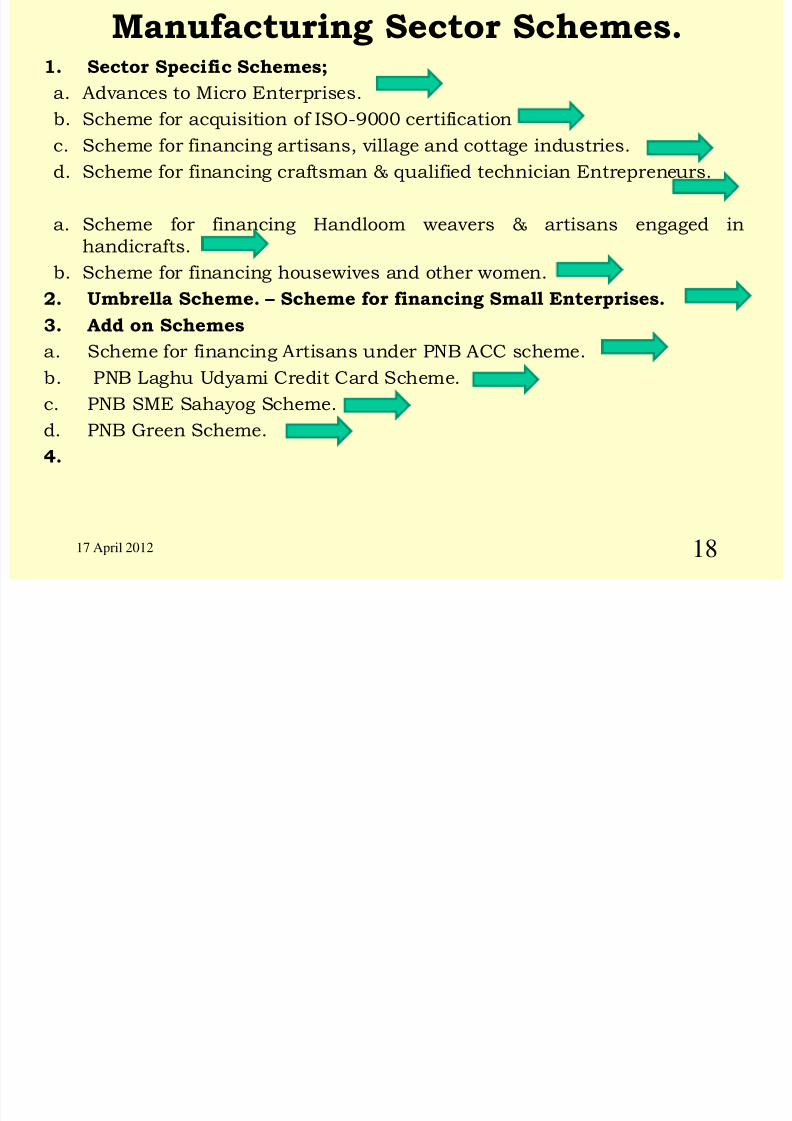

Manufacturing Sector Schemes.1. Sector Specific Schemes;

a. Advances to Micro Enterprises.

b. Scheme for acquisition of ISO-9000 certification

c. Scheme for financing artisans, village and cottage industries.

d. Scheme for financing craftsman & qualified technician Entrepreneurs.

a. Scheme for financing Handloom weavers & artisans engaged in

handicrafts.

b. Scheme for financing housewives and other women.2. Umbrella Scheme. – Scheme for financing Small Enterprises.

3. Add on Schemes

a. Scheme for financing Artisans under PNB ACC scheme.

b. PNB Laghu Udyami Credit Card Scheme.

c. PNB SME Sahayog Scheme.d. PNB Green Scheme.

4.

17 April 2012 18

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 19/102

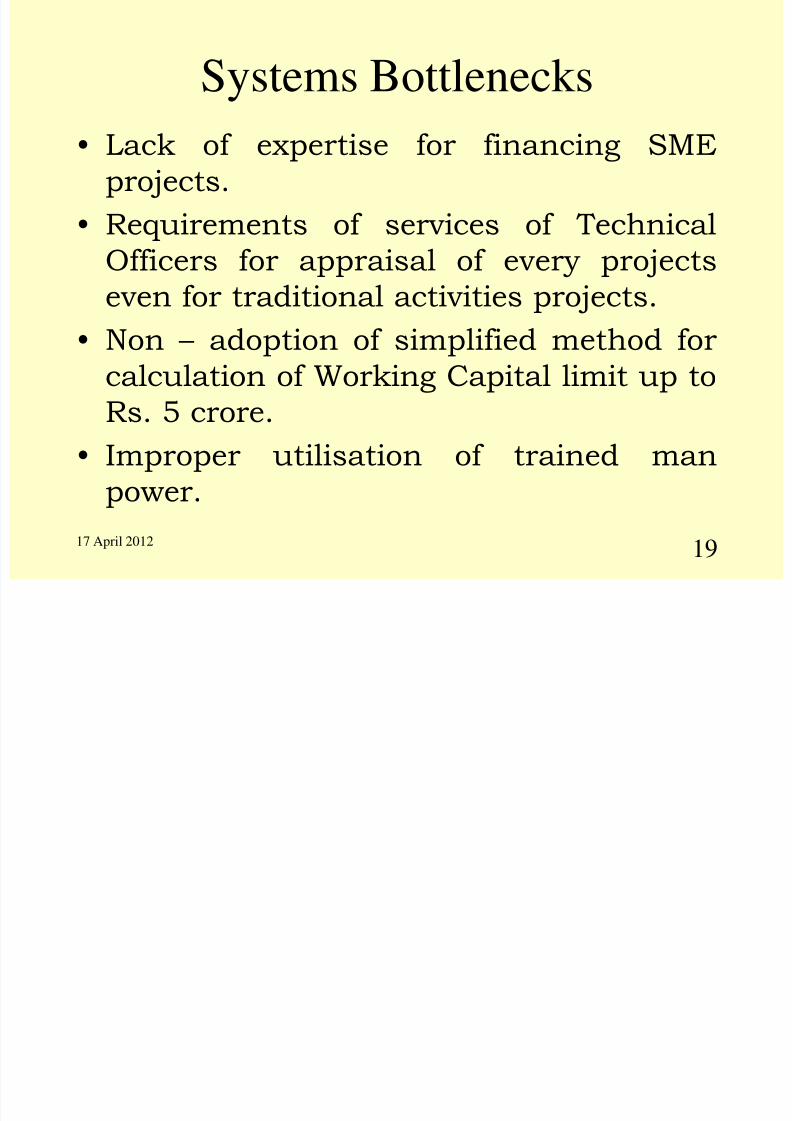

Systems Bottlenecks

• Lack of expertise for financing SMEprojects.

• Requirements of services of Technical

Officers for appraisal of every projectseven for traditional activities projects.

• Non – adoption of simplified method for

calculation of Working Capital limit up to

Rs. 5 crore.• Improper utilisation of trained man

power.

17 April 2012 19

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 20/102

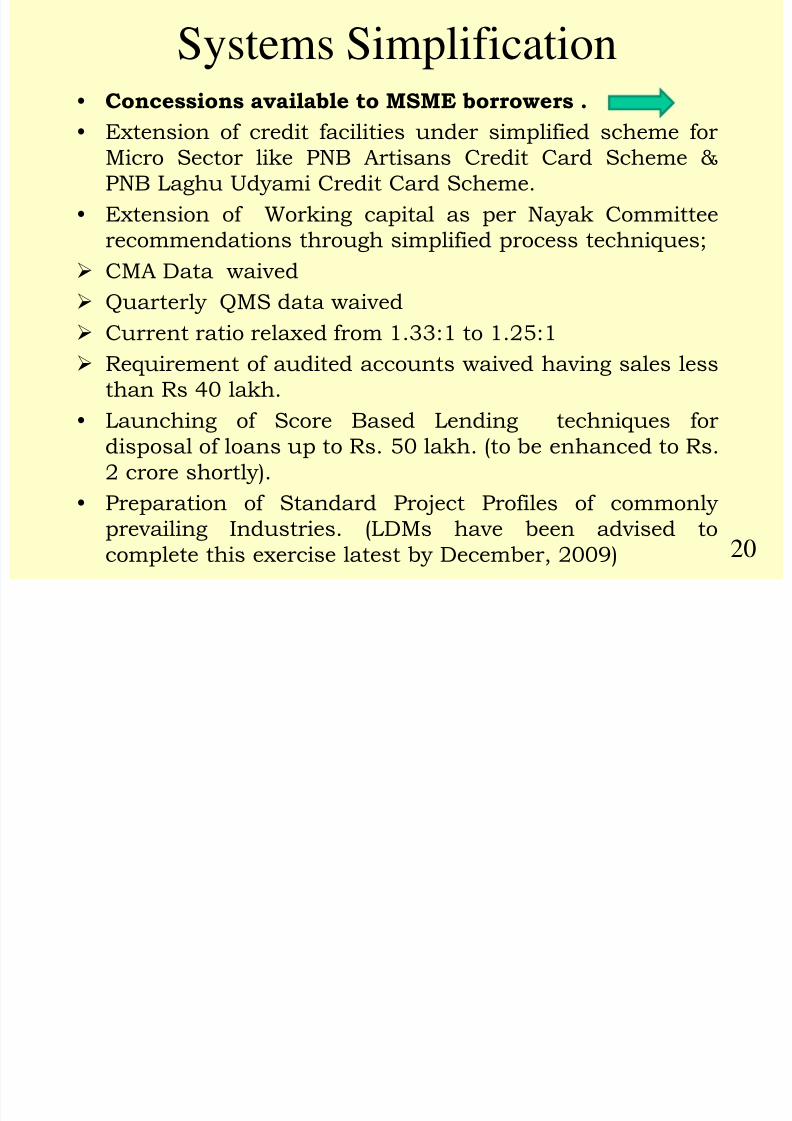

Systems Simplification• Concessions available to MSME borrowers .

• Extension of credit facilities under simplified scheme forMicro Sector like PNB Artisans Credit Card Scheme &

PNB Laghu Udyami Credit Card Scheme.

• Extension of Working capital as per Nayak Committee

recommendations through simplified process techniques;

CMA Data waived Quarterly QMS data waived

Current ratio relaxed from 1.33:1 to 1.25:1

Requirement of audited accounts waived having sales less

than Rs 40 lakh.

• Launching of Score Based Lending techniques for

disposal of loans up to Rs. 50 lakh. (to be enhanced to Rs.

2 crore shortly).

• Preparation of Standard Project Profiles of commonly

prevailing Industries. (LDMs have been advised to

complete this exercise latest by December, 2009) 20

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 21/102

INITIATIVES TAKEN BY

BANK TO BOOST SMEADVANCES

17 April 2012 21

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 22/102

17 April 2012

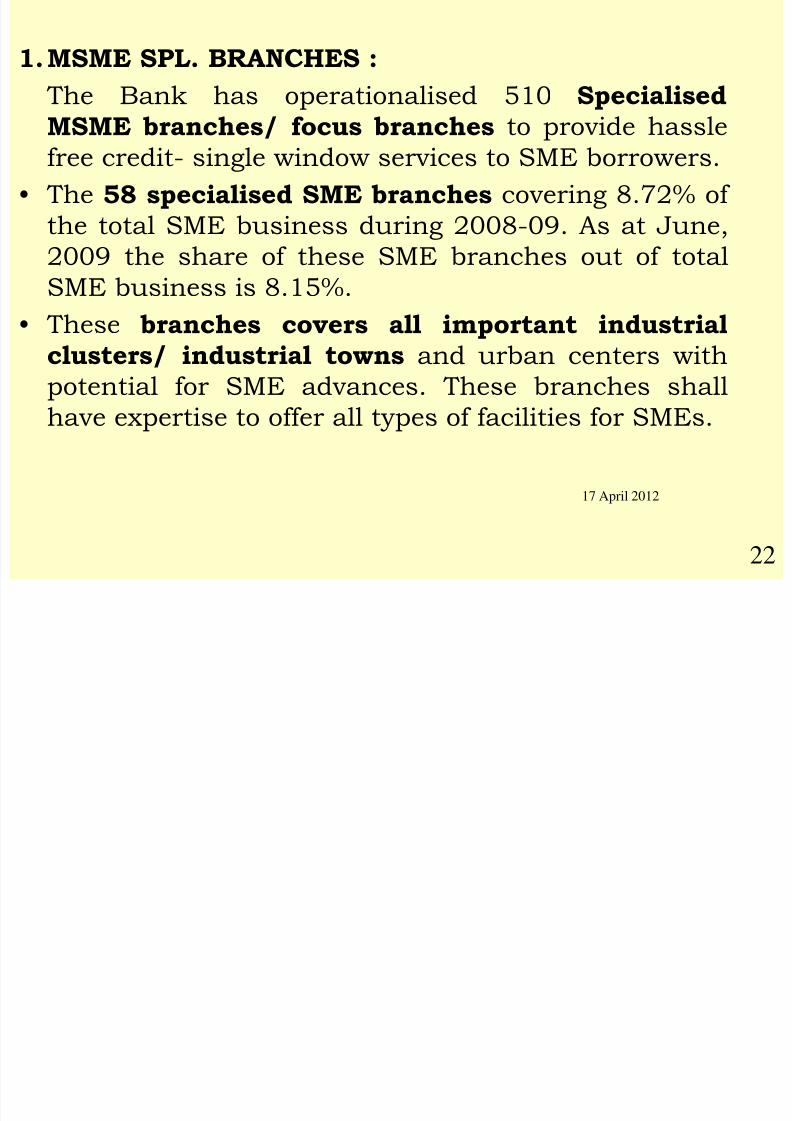

1. MSME SPL. BRANCHES :

The Bank has operationalised 510 Specialised

MSME branches/ focus branches to provide hasslefree credit- single window services to SME borrowers.

• The 58 specialised SME branches covering 8.72% of

the total SME business during 2008-09. As at June,

2009 the share of these SME branches out of total

SME business is 8.15%.

• These branches covers all important industrial

clusters/ industrial towns and urban centers with

potential for SME advances. These branches shall

have expertise to offer all types of facilities for SMEs.

22

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 23/102

2.Adoption of Cluster Approach to SME Financing

• Initially, the bank adopted four SME clusters at “Ludhiana

(Hosiery & Sewing Machines) & Mandi Gobindgarh (Steel re-

rolling mills) in Punjab; Kurukshetra (Rice shellers); Gurgaon

(Auto ancillaries) in Haryana.

• During 2008-09, our Bank has adopted eleven more clusters

at Jalandhar (sports goods); Trichy (Engineering goods);

Panipat (Textile); Bhilwara (Textiles); Ahmedabad

(Pharmaceuticals); Agra (leather); Jaipur (Ball Bearings);Moradabad (Brass-wares); Aligarh (locks); Khurja (Pottery);

Meerut (Sports goods).

• To cater the financial needs of Artisans, our Bank has

adopted Moradabad Mega Cluster identified by GOI, where

approximately 15,000 will be covered under credit linkage.

• We shall conduct annual study of SME clusters by deputing

Officer (industry) and MTMs to identify their credit

requirements and launching of innovative lending products.

23

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 24/102

3.Special focus- Service Sector Financing

• This segment presently constitutes 15% of SMEfinance and it was proposed to increase by 40% of

total MSME advances by focused attention.

• Special emphasis has been given for advances to

service sector.

• Growing opportunities /scope available by new

MSME definition in Services sub sectors i.e.

Transport, Educational Institutes, Hospitality

,Health and Retail Trade shall be explored by better

focus on segments by creating independent desks.

.

24

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 25/102

25

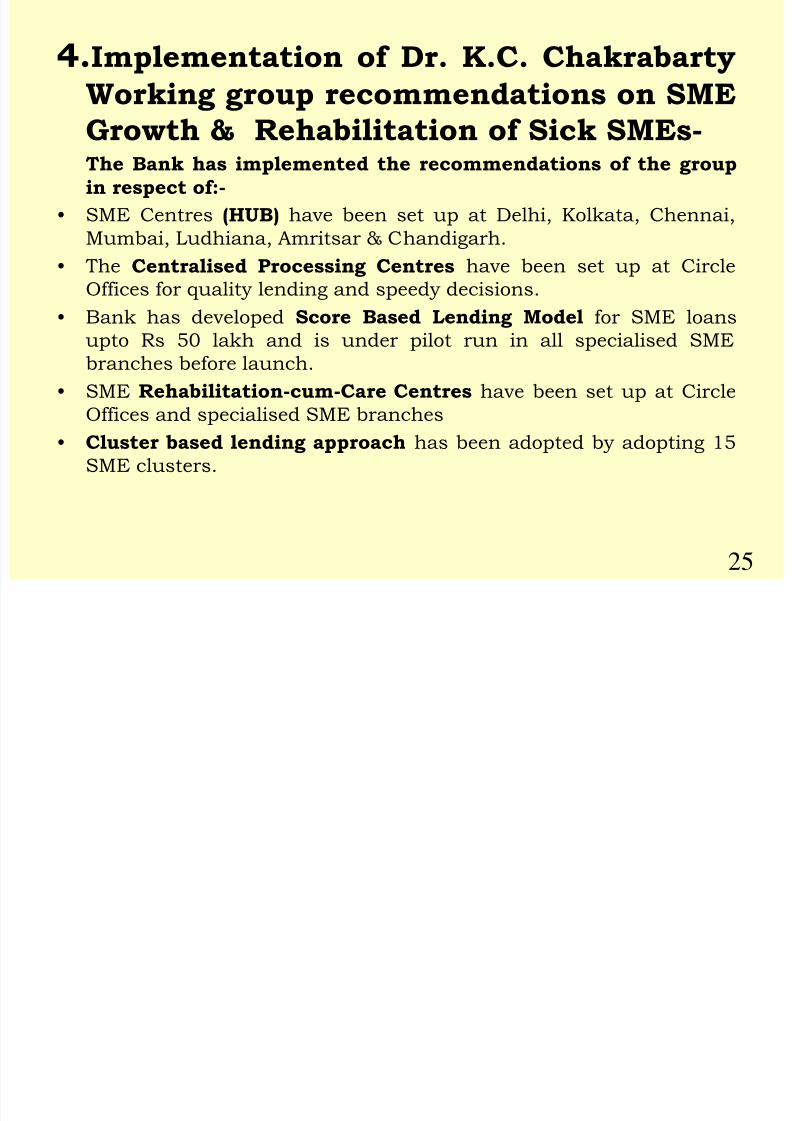

4.Implementation of Dr. K.C. Chakrabarty

Working group recommendations on SME

Growth & Rehabilitation of Sick SMEs-The Bank has implemented the recommendations of the group

in respect of:-

• SME Centres (HUB) have been set up at Delhi, Kolkata, Chennai,

Mumbai, Ludhiana, Amritsar & Chandigarh.

• The Centralised Processing Centres have been set up at CircleOffices for quality lending and speedy decisions.

• Bank has developed Score Based Lending Model for SME loans

upto Rs 50 lakh and is under pilot run in all specialised SME

branches before launch.

• SME Rehabilitation-cum-Care Centres have been set up at Circle

Offices and specialised SME branches

• Cluster based lending approach has been adopted by adopting 15

SME clusters.

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 26/102

5.Adoption of Code of Conduct for Micro

Small Enterprises (MSE Code) .

– We have adopted the above Code for

implementation.

– In line with the commitments madeunder the Code, Micro and Small

Enterprises customers shall be provided

easy access to our services.

– We shall also maintain desired standardsof service and ensure transparency in our

dealings.

26

6 Mi E t i

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 27/102

6. Micro EnterprisesFor quick disposal of Micro Enterprises loan proposals:

The cases of Micro enterprises are kept outside the ambit of SME

HUBS/ Central Credit Processing Centers.

Simplified loan application for loans up to Rs. 50 lakh.

Branch Managers have been vested with powers to directly

dispose of proposals at Branch Level.

To ensure maximum sanction at Branch Level for

cutting delays, BM’s have been vested with special higherloaning powers for financing micro enterprises

(manufacturing/service) covered under CGTSME Scheme :

Scale – II Managers vested with the powers of Scale-III for

disposal of MSME advances.

Scale – III Managers vested with 125% of their vested loaningpowers.

“Focused attention for extending Collateral freeloans up to Rs. 100 lakh” and Next Higherauthority can permit acceptance of guarantee/

Collaterals.

27

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 28/102

17 April 2012

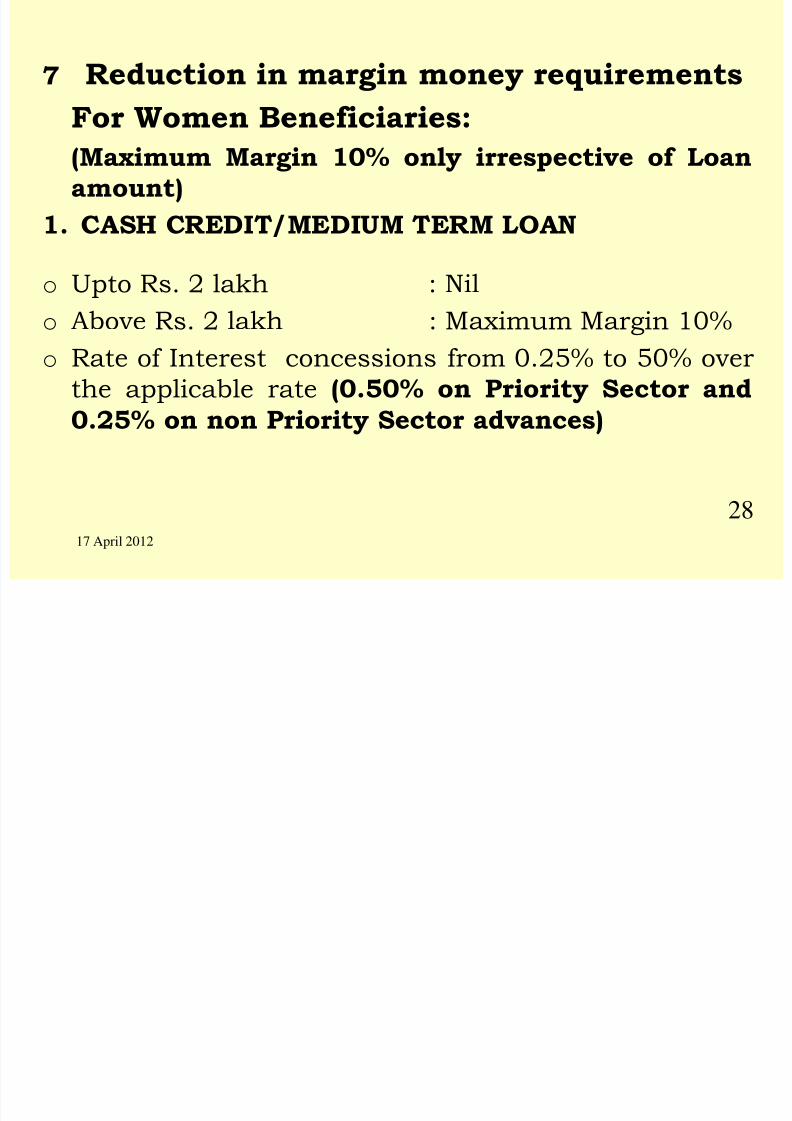

7 Reduction in margin money requirements

For Women Beneficiaries:

(Maximum Margin 10% only irrespective of Loan

amount)

1. CASH CREDIT/MEDIUM TERM LOAN

o Upto Rs. 2 lakh : Nil

o Above Rs. 2 lakh : Maximum Margin 10%

o Rate of Interest concessions from 0.25% to 50% over

the applicable rate (0.50% on Priority Sector and

0.25% on non Priority Sector advances)

28

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 29/102

17 April 2012

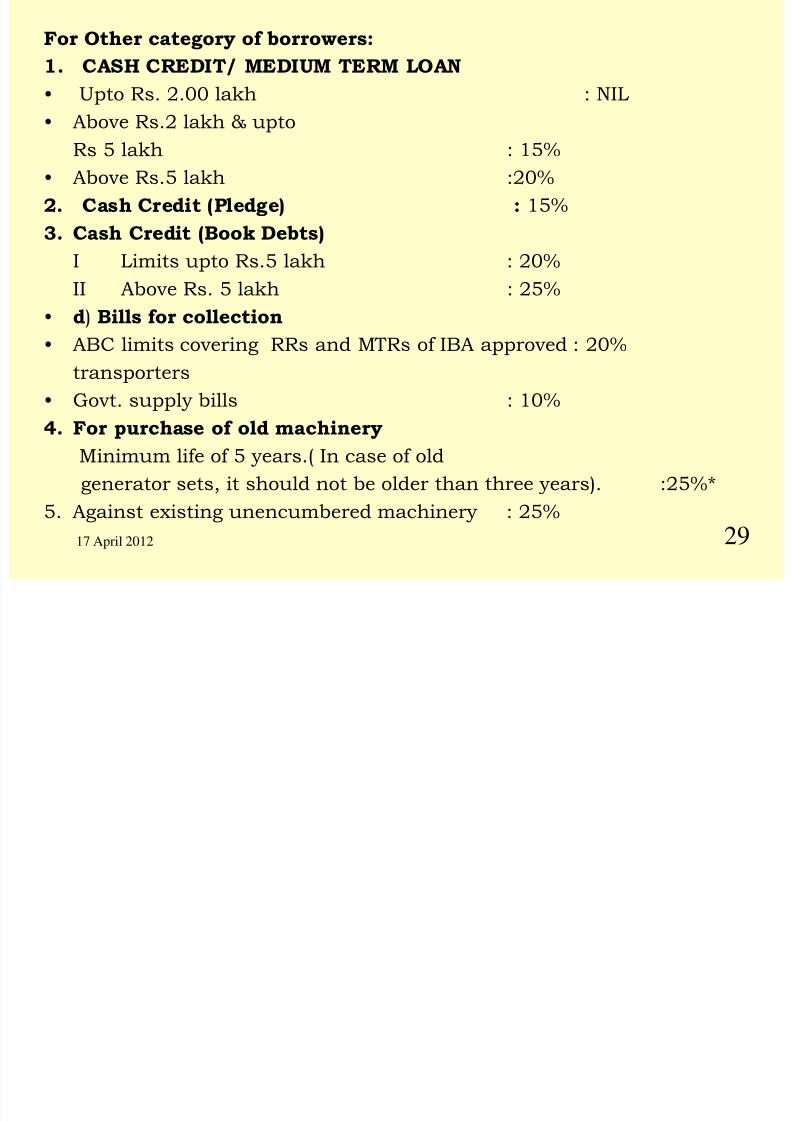

For Other category of borrowers:

1. CASH CREDIT/ MEDIUM TERM LOAN

• Upto Rs. 2.00 lakh : NIL

• Above Rs.2 lakh & upto

Rs 5 lakh : 15%

• Above Rs.5 lakh :20%

2. Cash Credit (Pledge) : 15%

3. Cash Credit (Book Debts)

I Limits upto Rs.5 lakh : 20%

II Above Rs. 5 lakh : 25%

• d) Bills for collection • ABC limits covering RRs and MTRs of IBA approved : 20%

transporters

• Govt. supply bills : 10%

4. For purchase of old machinery

Minimum life of 5 years.( In case of old

generator sets, it should not be older than three years). :25%*

5. Against existing unencumbered machinery : 25%

29

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 30/102

17 April 2012

8. Assessment of Working Capital

Working capital to SME borrowers is assessed

as per simplified turn over method (NayakCommittee ) for cash credit limit up to Rs.

5 crore.

For assessment of working capital;

CMA Data waived

Quarterly QMS data waived

Current ratio relaxed from 1.33:1 to 1.25:1

Requirement of audited accounts waivedhaving sales less than Rs 40 lakh.

30

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 31/102

17 April 2012

9. Credit facilities in emergent circumstances – over & above Drawing Power

Special credit limit under PNB SME SAHAYOG Scheme is extended

for an amount equal to 20% of the aggregate working capital limits(i.e. fund based and non fund based separately) sanctioned,subject to a maximum of Rs.25 lakh with out linking to DP forcontingencies like additional purchase of raw materials includingpacking materials/handling charges for the execution of bulkorders, taking part in national/international trade exhibitions for

creating market base, payment of consultancy charges, repairs tomachinery, labour payments, etc.

In order to meet payment of statutory dues exclusively like incometax, sales tax, excise duty and other expenses like electricity charges, custom duties, telephone expenses by SSI units in

emergent circumstances, bank will provide/ sanction 5% GreenCash Credit facility maximum upto Rs.2.00 lakh of the fund basedsanction limit/assessed permissible bank finance, over & aboveregular adhoc facility or Credit Facility availed by SSI units underSME Sahayog and available drawing Power.

31

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 32/102

17 April 2012

10. Project Financing: Relaxation in level of Debt

Equity Ratio (from acceptable level of 2:1 for project

financing;

The Circle Heads shall relax up to 2.50:1. The GeneralManager(HO) relax up to 3.00:1 and ED/CMD shall relax up

to 4.00:1.

11. Processes for speedy disposal of SMEprojects

SME Centres (HUB) : have been set up at Delhi, Kolkata,

Chennai, Mumbai, Ludhiana, Amritsar & Chandigarh. The Centralised Credit Processing Centers have been set

up at Circle Offices for quality lending and speedy decisions.

32

12 Di t i t i P j t R t

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 33/102

12. District-wise Project Reports

With a view to obviate the need for detailed project

reports with every proposal, common industrialactivities prevailing in a district are being identified

for preparation of standard project reports

initially for projects up to Rs. 1 crore to be

extended subsequently up to Rs. 2 crore. Theseproject reports are approved for a district. This shall

help the borrowers to use these standard project

reports while developing their projects while the

branch do not undertake specific techno-economicviability study for proposals under these activities

where the standard project reports have been

prepared. 33

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 34/102

17 April 2012

13. Setting up of SME Rehabilitation cum

care centers

The Bank has set up Rehabilitation cum Care

Centers at Circle Offices / SME branches

manned by officials having expertise in financing

SMEs. These Centers have SME Managers forgrowth and development and SME Managers for

counseling. They guide the MSME units on the

matters relating to their financial needs and the

facilities available from the Banks / Govt. / RBI.

The Circle wise list and names of the dealing

officials are available on Bank’s web-site.

34

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 35/102

14. Credit Ratings: The Bank has approved SMERA,

CRISIL rating companies for providing independent

risk rating of SME projects. As at March, 09 SMERA

& CRISIL have rated 231 and 188 SME accounts of our bank respectively.

The Bank is extending concession of 0.50% and

0.25% in chargeable rate of interest to the borrowers

of SMERA & CRISIL rating having rating grade 1 & 2

and grade 3 respectively.

Bank is having equity participation in SME rating

agency (SMERA).

3517 April 2012

CGTMSE

SCHEME FOR FINANCING TRANSPORT OPERATORS

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 36/102

SCHEME FOR FINANCING TRANSPORT OPERATORS

ELIGIBILITY:

• An individual or an association desirous of owning

transport vehicle(s), for carrying passengers or goods onhire, hold the necessary driving license or engage driver

(s) possessing valid license and granted a permit by an

appropriate authority to ply vehicle (s) for passengers or

goods traffic for hire.

EXTENT OF LOAN - FOR NEW TRUCK(S)/BUS (S) : • 90% loans of the invoice cost of the vehicle inclusive of

the cost of chassis, construction of body thereon.

MARGIN

For new Trucks/ Buses For New Trucks: 10%

For New Buses : 10%

For Old Vehicle: 15%

36

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 37/102

COLLATERAL SECURITY :

• No collateral security or third party guarantee

should be taken for loans up to Rs. 100 lakh covered

under Credit Guarantee Scheme of CGTMSE. Interms of Loans & Advances Circular No. 34 dated 7th

March 2008 and PSLB/SME Circular No. 55/2008

dated 6th August, 2008, permission of Circle Head be

obtained for accepting collateral security.• INTEREST : As per bank’s guidelines issued from

time to time as applicable to Micro, Small & Medium

Enterprises (Service Sector) according to the amount

of loan.. (As per Loans & Advances Circular. No.16/2009 dated 31st January 2009) “Subject to

change from time to time”.

37

SCHEME FOR FINANCING TO OWNER DRIVERS OF

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 38/102

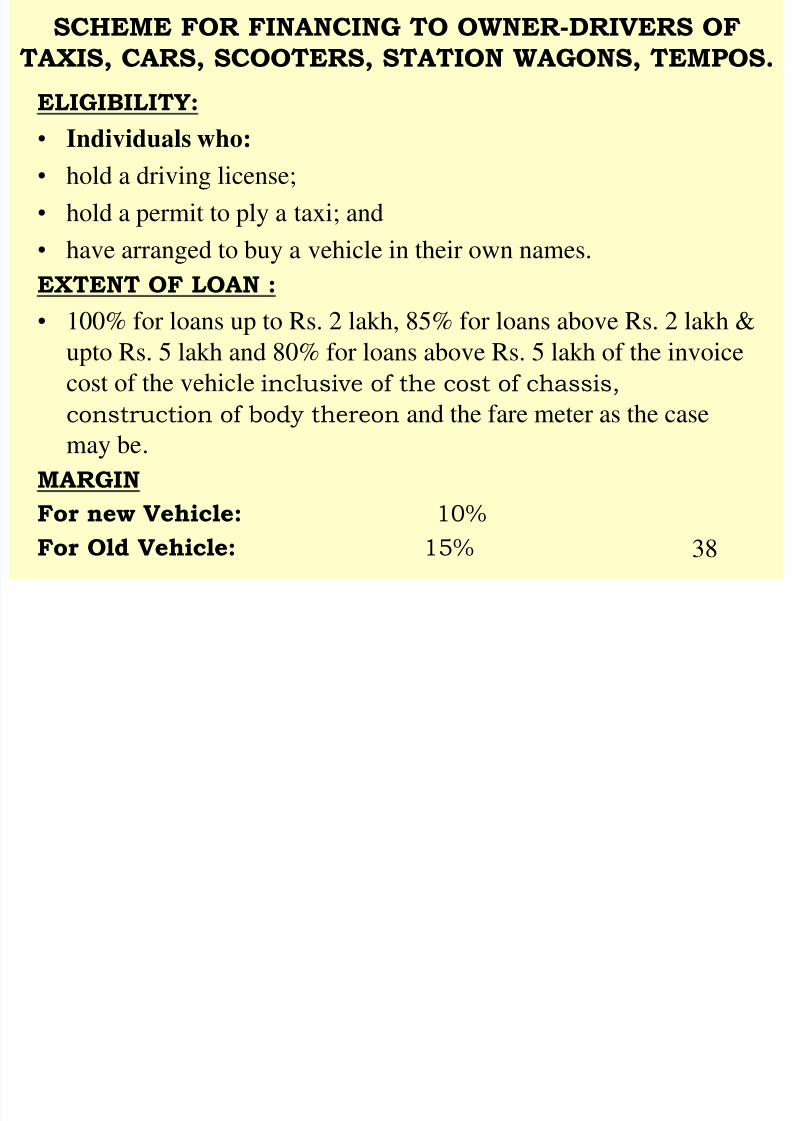

SCHEME FOR FINANCING TO OWNER-DRIVERS OF

TAXIS, CARS, SCOOTERS, STATION WAGONS, TEMPOS.

ELIGIBILITY:

• Individuals who: • hold a driving license;

• hold a permit to ply a taxi; and

• have arranged to buy a vehicle in their own names.

EXTENT OF LOAN :

• 100% for loans up to Rs. 2 lakh, 85% for loans above Rs. 2 lakh &

upto Rs. 5 lakh and 80% for loans above Rs. 5 lakh of the invoice

cost of the vehicle inclusive of the cost of chassis,

construction of body thereon and the fare meter as the casemay be.

MARGIN

For new Vehicle: 10%

For Old Vehicle: 15% 38

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 39/102

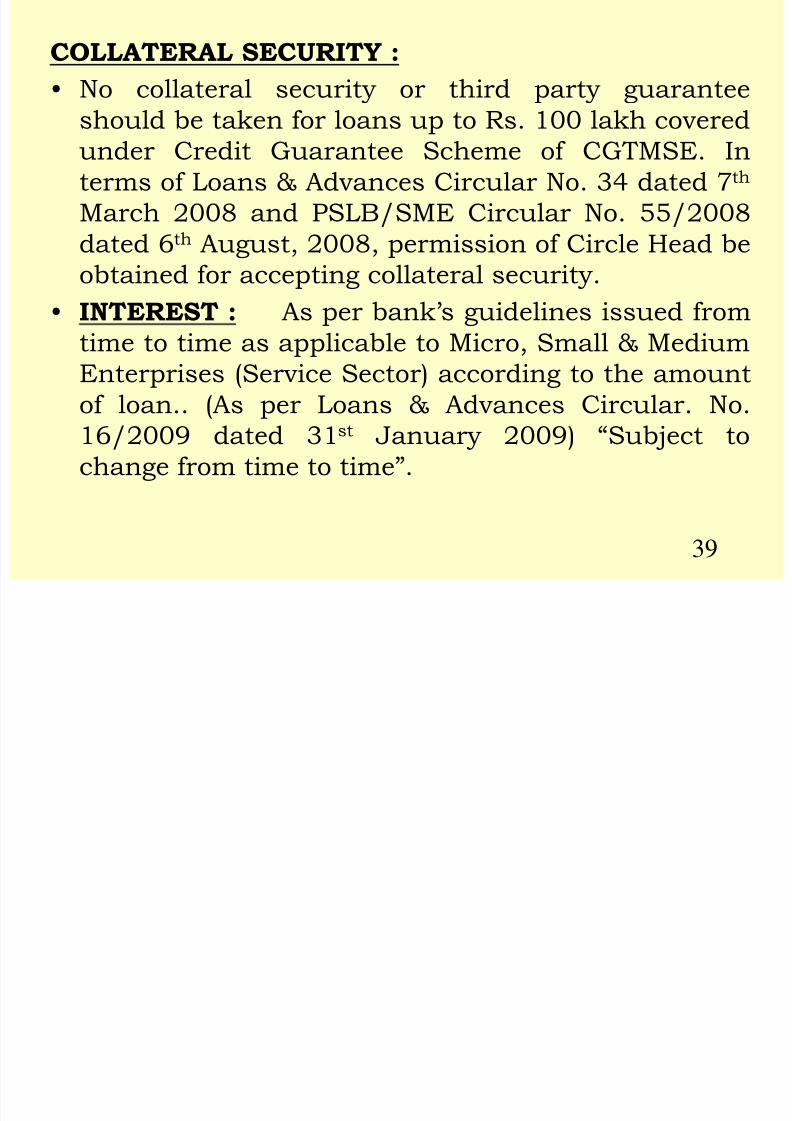

COLLATERAL SECURITY :

• No collateral security or third party guarantee

should be taken for loans up to Rs. 100 lakh covered

under Credit Guarantee Scheme of CGTMSE. Interms of Loans & Advances Circular No. 34 dated 7th

March 2008 and PSLB/SME Circular No. 55/2008

dated 6th August, 2008, permission of Circle Head be

obtained for accepting collateral security.• INTEREST : As per bank’s guidelines issued from

time to time as applicable to Micro, Small & Medium

Enterprises (Service Sector) according to the amount

of loan.. (As per Loans & Advances Circular. No.16/2009 dated 31st January 2009) “Subject to

change from time to time”.

39

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 40/102

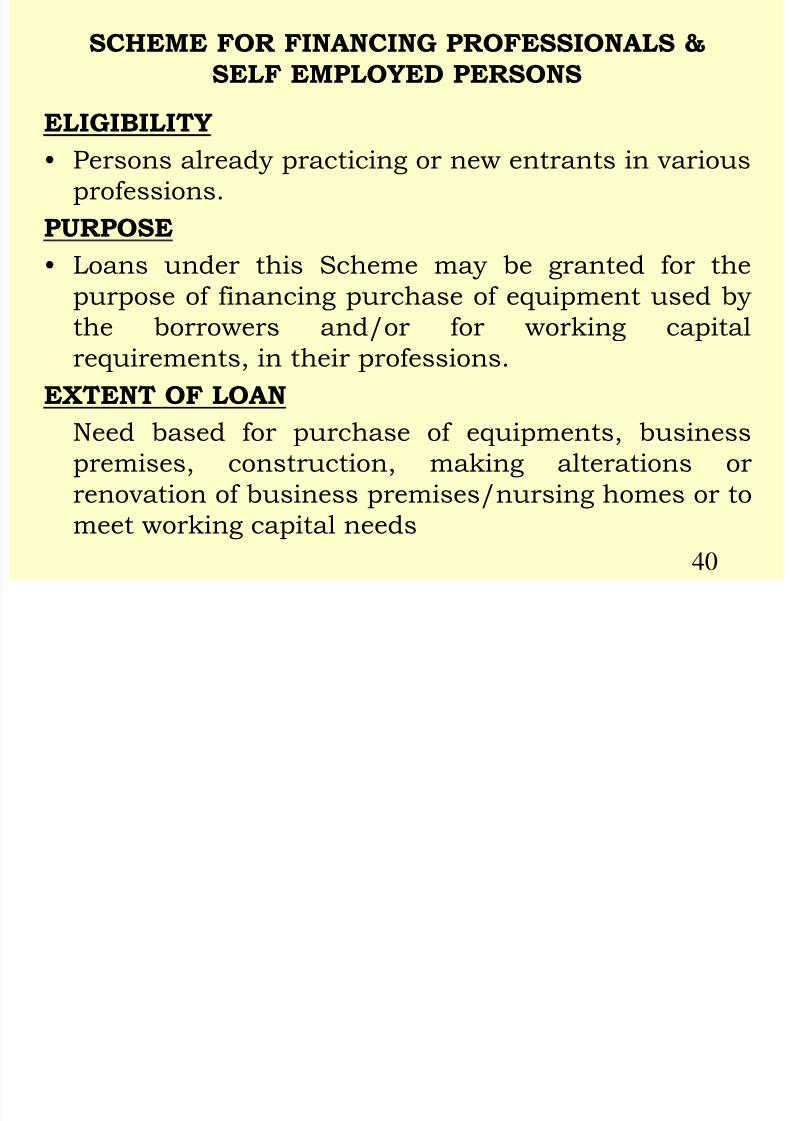

SCHEME FOR FINANCING PROFESSIONALS &

SELF EMPLOYED PERSONS

ELIGIBILITY

• Persons already practicing or new entrants in various

professions.

PURPOSE

• Loans under this Scheme may be granted for thepurpose of financing purchase of equipment used by

the borrowers and/or for working capital

requirements, in their professions.

EXTENT OF LOAN

Need based for purchase of equipments, business

premises, construction, making alterations or

renovation of business premises/nursing homes or to

meet working capital needs

40

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 41/102

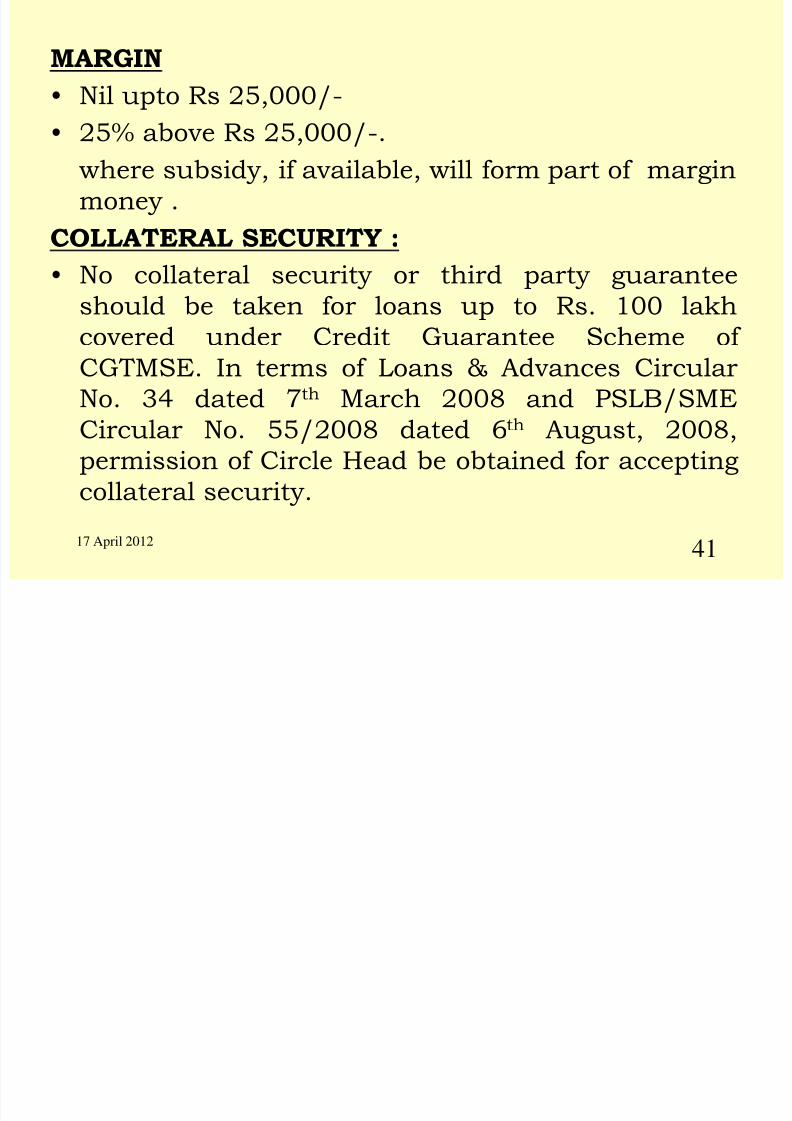

MARGIN

• Nil upto Rs 25,000/-

• 25% above Rs 25,000/-.where subsidy, if available, will form part of margin

money .

COLLATERAL SECURITY :

• No collateral security or third party guaranteeshould be taken for loans up to Rs. 100 lakh

covered under Credit Guarantee Scheme of

CGTMSE. In terms of Loans & Advances Circular

No. 34 dated 7th March 2008 and PSLB/SME

Circular No. 55/2008 dated 6th August, 2008,

permission of Circle Head be obtained for accepting

collateral security.

17 April 2012

41

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 42/102

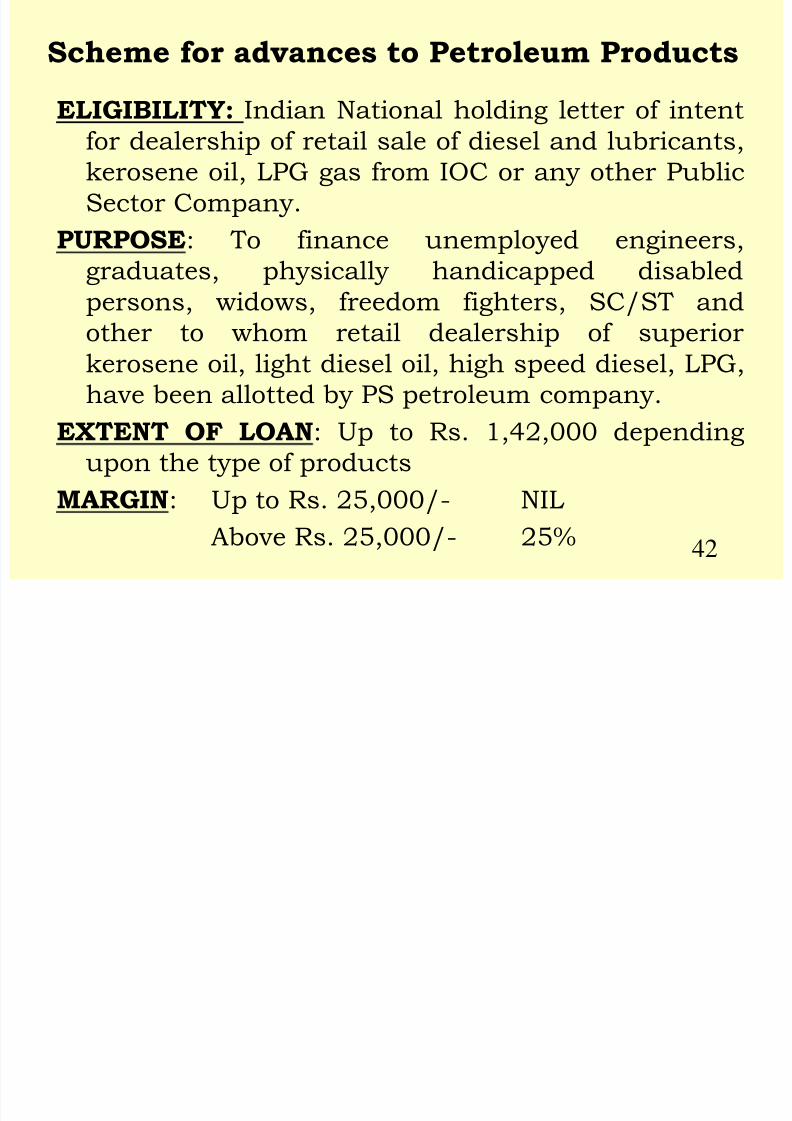

Scheme for advances to Petroleum Products

ELIGIBILITY: Indian National holding letter of intent

for dealership of retail sale of diesel and lubricants,kerosene oil, LPG gas from IOC or any other Public

Sector Company.

PURPOSE: To finance unemployed engineers,

graduates, physically handicapped disabledpersons, widows, freedom fighters, SC/ST and

other to whom retail dealership of superior

kerosene oil, light diesel oil, high speed diesel, LPG,

have been allotted by PS petroleum company.

EXTENT OF LOAN: Up to Rs. 1,42,000 depending

upon the type of products

MARGIN: Up to Rs. 25,000/- NIL

Above Rs. 25,000/- 25% 42

Ad t E S i f tti f

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 43/102

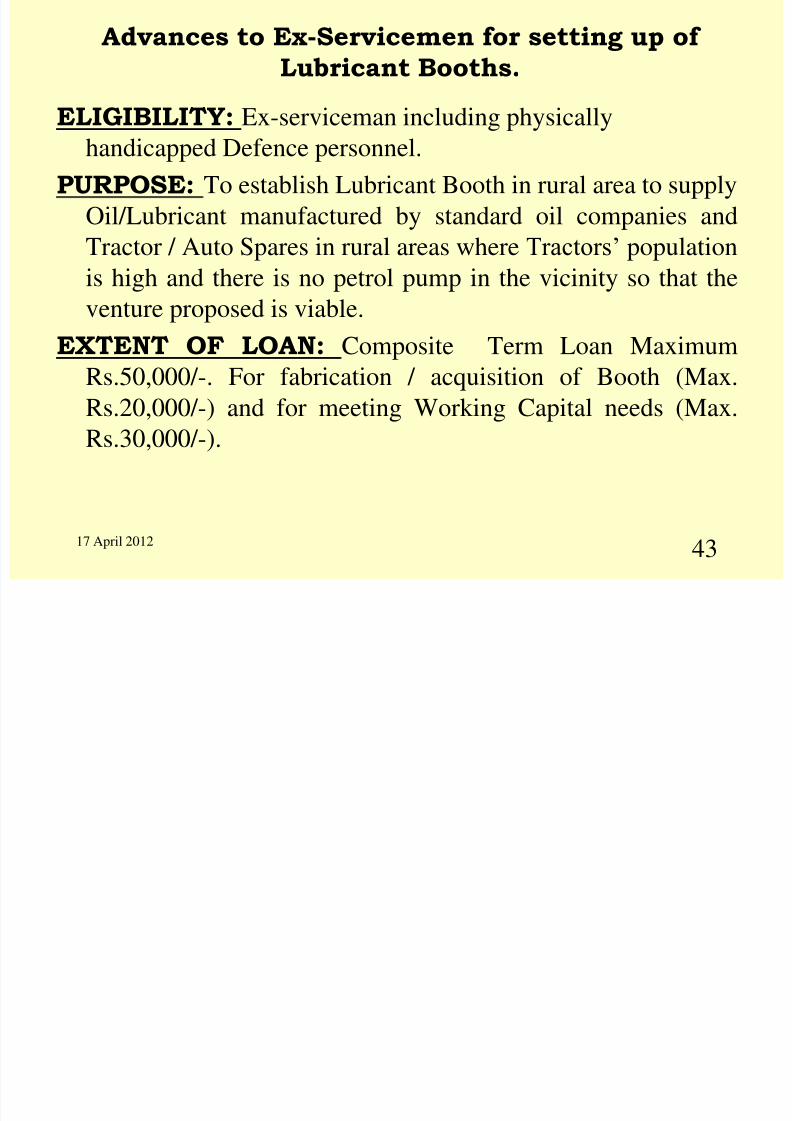

Advances to Ex-Servicemen for setting up of

Lubricant Booths.

ELIGIBILITY: Ex-serviceman including physically

handicapped Defence personnel.

PURPOSE: To establish Lubricant Booth in rural area to supply

Oil/Lubricant manufactured by standard oil companies and

Tractor / Auto Spares in rural areas where Tractors‟ population

is high and there is no petrol pump in the vicinity so that theventure proposed is viable.

EXTENT OF LOAN: Composite Term Loan Maximum

Rs.50,000/-. For fabrication / acquisition of Booth (Max.

Rs.20,000/-) and for meeting Working Capital needs (Max.Rs.30,000/-).

17 April 2012

43

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 44/102

17 April 2012 44

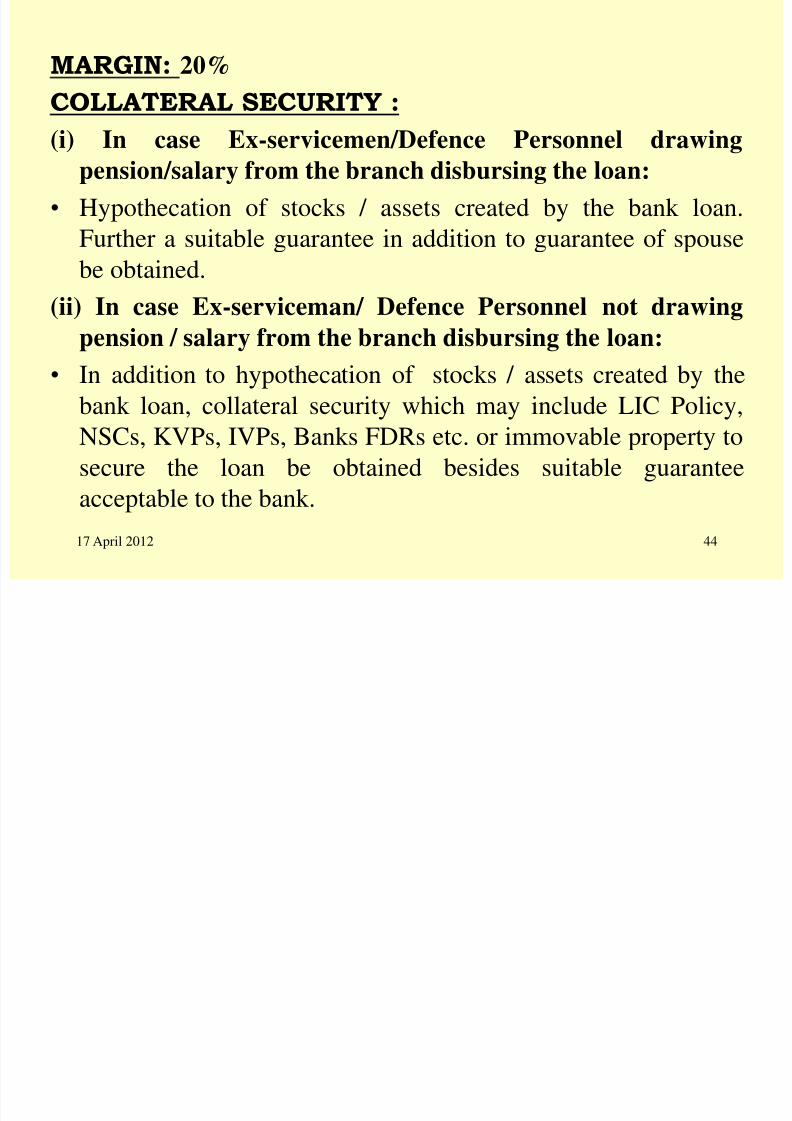

MARGIN: 20%

COLLATERAL SECURITY :

(i) In case Ex-servicemen/Defence Personnel drawingpension/salary from the branch disbursing the loan:

• Hypothecation of stocks / assets created by the bank loan.

Further a suitable guarantee in addition to guarantee of spouse

be obtained.(ii) In case Ex-serviceman/ Defence Personnel not drawing

pension / salary from the branch disbursing the loan:

• In addition to hypothecation of stocks / assets created by the

bank loan, collateral security which may include LIC Policy,NSCs, KVPs, IVPs, Banks FDRs etc. or immovable property to

secure the loan be obtained besides suitable guarantee

acceptable to the bank.

Ad t E S i f tti f

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 45/102

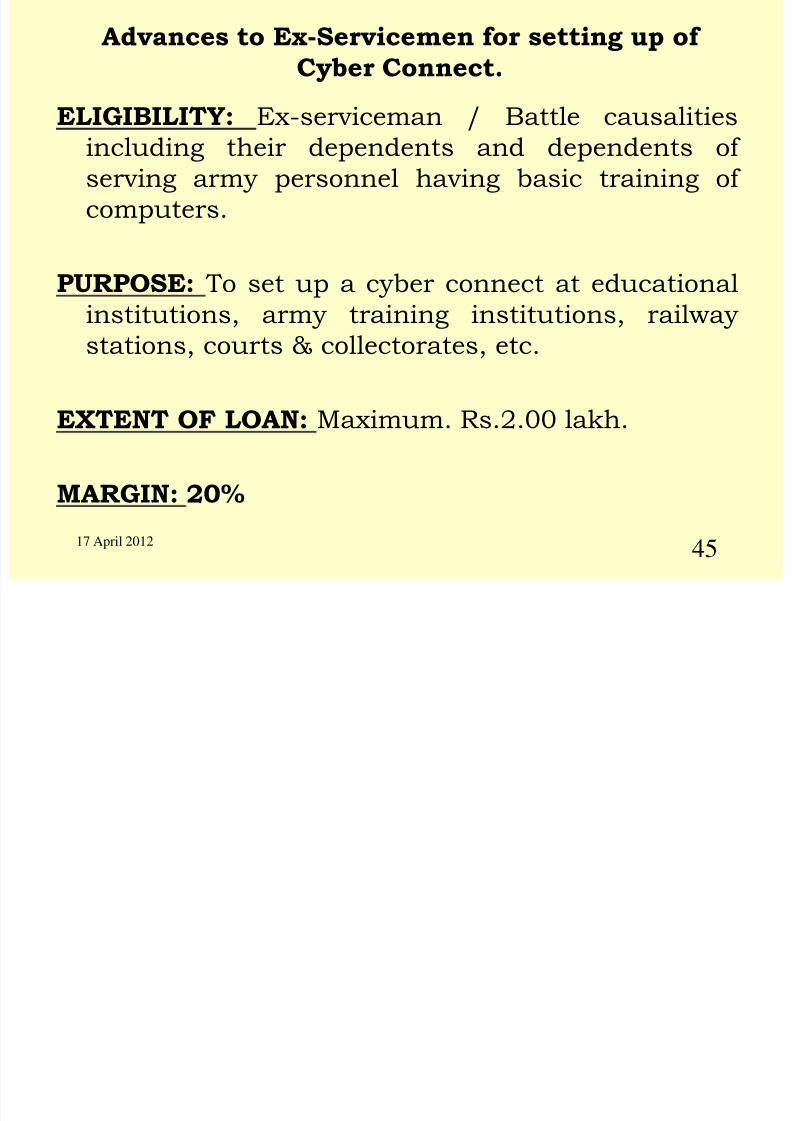

Advances to Ex-Servicemen for setting up of

Cyber Connect.

ELIGIBILITY: Ex-serviceman / Battle causalities

including their dependents and dependents of serving army personnel having basic training of

computers.

PURPOSE: To set up a cyber connect at educationalinstitutions, army training institutions, railway

stations, courts & collectorates, etc.

EXTENT OF LOAN: Maximum. Rs.2.00 lakh.

MARGIN: 20%

17 April 2012

45

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 46/102

17 April 2012 46

COLLATERAL SECURITY :

(i) In case Ex-servicemen / Defence Personnel drawingpension / salary from the branch disbursing the loan:

Hypothecation of Computers, Cyber connect Kit, NIC,

Power Conditioning Equipment, Computer Diaries,

Printers and Stabilizers etc. Further a suitable guarantee

in addition to guarantee of spouse be obtained.

In case of loans to dependents, parents/spouse will stand

as guarantor in addition to suitable guarantee acceptableto the bank.

(ii) In case Ex-serviceman / Defence Personnel not

drawing pension / salary from the branch disbursing

the loan:

In addition to hypothecation of assets as stated above,collateral security which may include LIC Policy, NSCs,

KVPs, IVPs, Banks FDRs etc. or immovable property to

secure the loan be obtained besides suitable guarantee.

Ad t W id f tti g f S ll

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 47/102

Advances to War-widows for setting up of Small

Service & Business Activities.

ELIGIBILITY: War widows

PURPOSE: To set up Small Service & Business Activities.

The illustrative list of activities, which can be undertaken, has

been given as per Appendix. Activities other than as

mentioned in illustrative list can also be undertaken by the warwidows if found technically feasible and economically viable

by the sanctioning authority.

• EXTENT OF LOAN: Maximum Rs.2.00 lakh (In RuralAreas)

• Rs. 5.00 lakh (In Semi Urban, Urban & Metros)

• 17 April 2012

47

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 48/102

MARGIN: 10% (irrespective of loan amount)

COLLATERAL SECURITY :

(i) For loans upto Rs.2.00 lakh:

• Hypothecation of Primary Security created out of loan

amount etc.

• Third party guarantee acceptable to bank be obtained

(ii) For loans above Rs.2.00 lakh and upto Rs.5.00 lakh.

• In addition to hypothecation of assets as stated above,collateral security which may include LIC Policy, NSCs,

KVPs, IVPs, Banks FDRs etc. or immovable property to

secure the loan be obtained besides suitable guarantee.

• NOTE : If, however, the loan account is eligible for

coverage under Credit Guarantee Fund Trust Scheme(CGTSI), No collateral security and third party guarantee

be obtained.

48

Advances to Micro and Industry Related

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 49/102

Advances to Micro and Industry Related

Service/Business Enterprises.

ELIGIBILITY: Small units having investment upto Rs

10.00 lakh in fixed assets, excluding land & buildingengaged in industry related service/business would be

entitled to the same concessions and incentives as

available to Small Scale Industries and ancillary

industries.

EXTENT OF LOAN: The credit facilities for SSSBEs may

be provided on the principle of need based requirement,

on the basis of simplified procedure.

• Composite Loan (Working Capital Term Loan) upto

Rs.100.00 lakh can be sanctioned to meet therequirement of funds for purchase for fixed assets and

working capital in case of those units, which require

loans upto Rs.100.00 lakh respective of their location.

17 April 2012

49

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 50/102

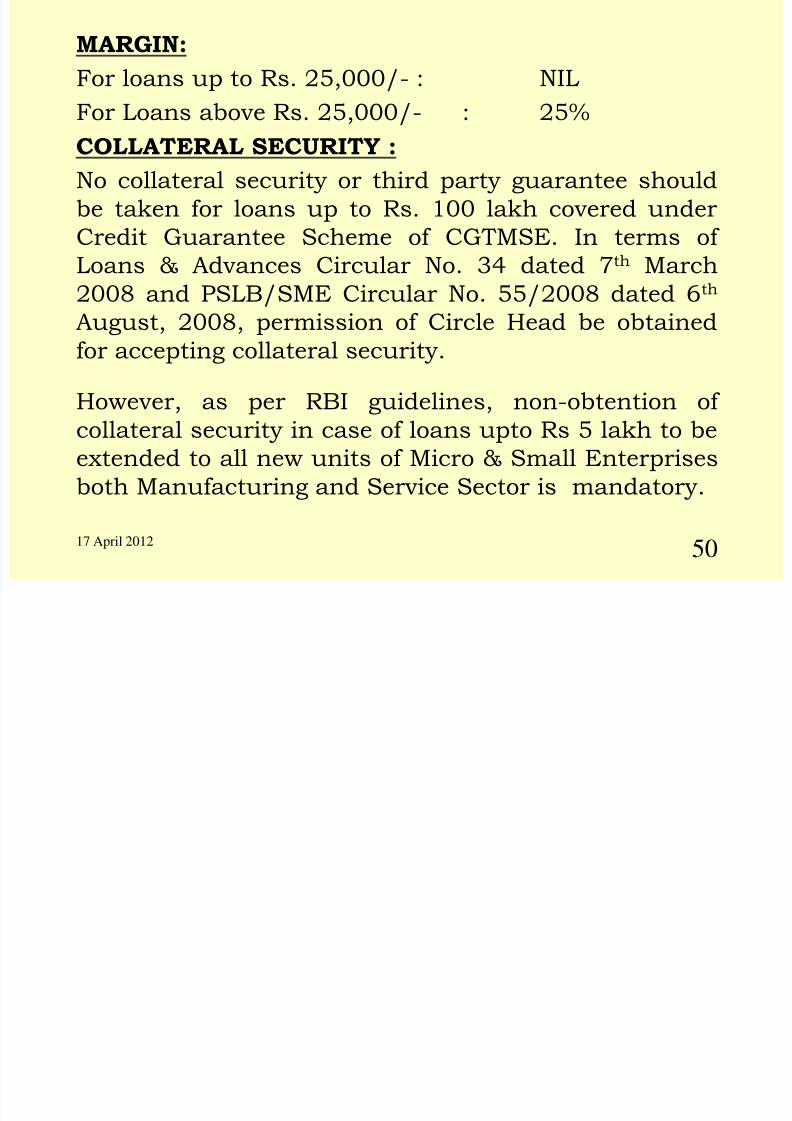

MARGIN:

For loans up to Rs. 25,000/- : NIL

For Loans above Rs. 25,000/- : 25%

COLLATERAL SECURITY :No collateral security or third party guarantee should

be taken for loans up to Rs. 100 lakh covered under

Credit Guarantee Scheme of CGTMSE. In terms of

Loans & Advances Circular No. 34 dated 7th March

2008 and PSLB/SME Circular No. 55/2008 dated 6th

August, 2008, permission of Circle Head be obtained

for accepting collateral security.

However, as per RBI guidelines, non-obtention of

collateral security in case of loans upto Rs 5 lakh to be

extended to all new units of Micro & Small Enterprises

both Manufacturing and Service Sector is mandatory.

17 April 2012

50

SCHEME FOR FINANCING SERVICE ACTIVITIES AS PER

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 51/102

SCHEME FOR FINANCING SERVICE ACTIVITIES AS PER

LOANS & ADVANCES CIRCULAR NO.20/2005 and 93/2008

PURPOSE

• To finance fixed assets required for setting up thebusiness including purchase of shops/offices.

EXTENT OF LOAN

• Working Capital Facility (FB & NFB) & Term Loan –

Need based

i) For purchase of shop- cum- office space – Maximum

Amount Rs.50.00 lakh per unit.

ii)Small service providers those may find difficulty in

making regular transactions from CC account,Working Capital Term Loan (WCTL) upto Rs.25 lakh

shall be granted.

17 April 2012

51

MARGIN

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 52/102

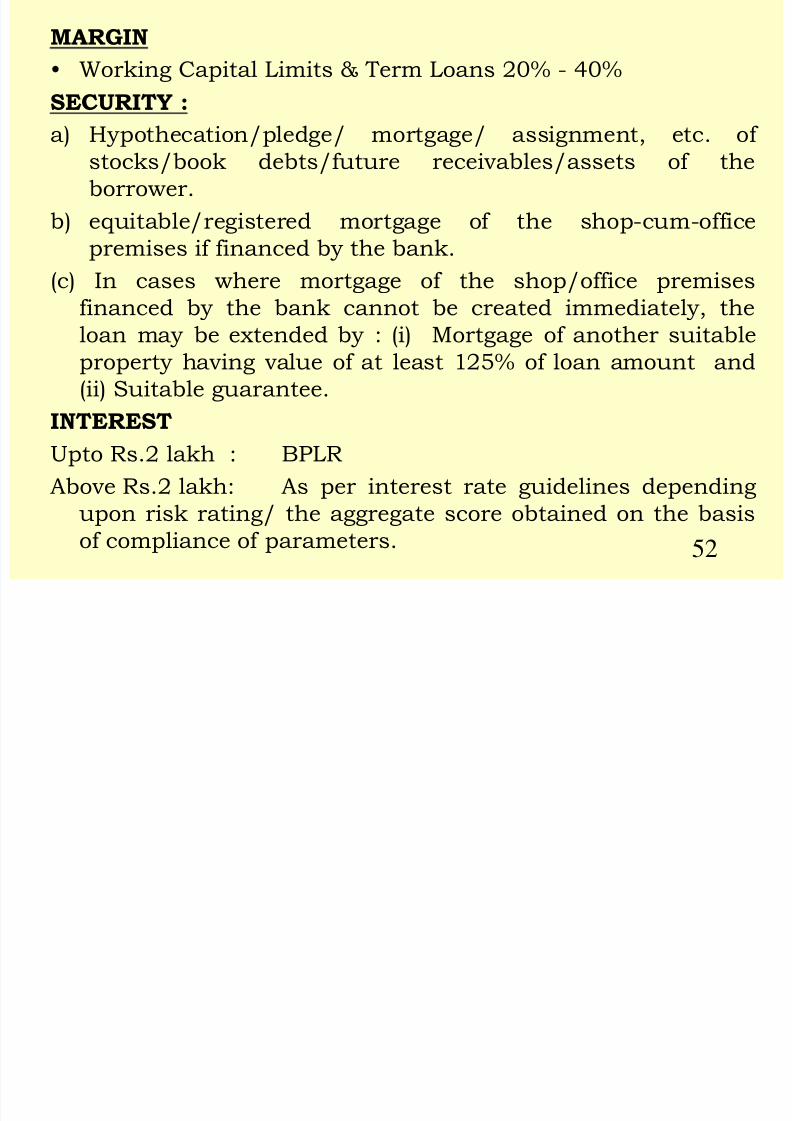

MARGIN

• Working Capital Limits & Term Loans 20% - 40%

SECURITY :

a) Hypothecation/pledge/ mortgage/ assignment, etc. of stocks/book debts/future receivables/assets of the

borrower.

b) equitable/registered mortgage of the shop-cum-office

premises if financed by the bank.

(c) In cases where mortgage of the shop/office premisesfinanced by the bank cannot be created immediately, the

loan may be extended by : (i) Mortgage of another suitable

property having value of at least 125% of loan amount and

(ii) Suitable guarantee.

INTEREST

Upto Rs.2 lakh : BPLR

Above Rs.2 lakh: As per interest rate guidelines depending

upon risk rating/ the aggregate score obtained on the basis

of compliance of parameters. 52

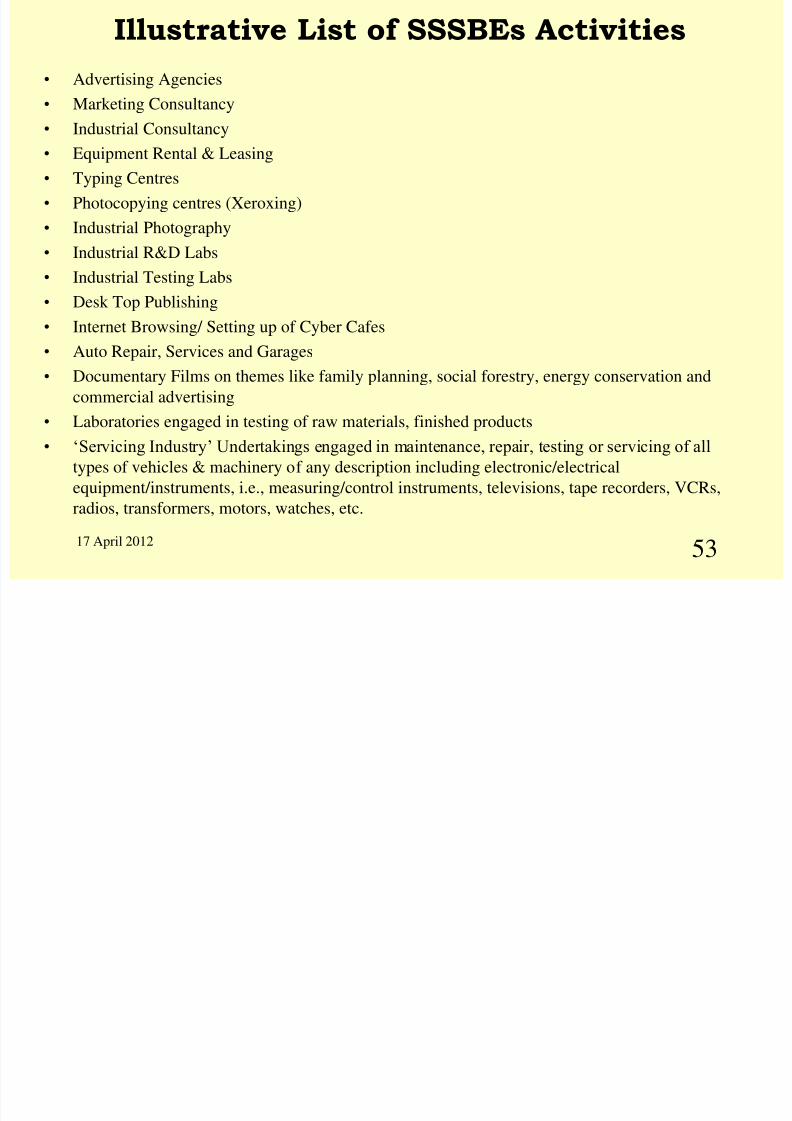

Illustrative List of SSSBEs Activities

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 53/102

Illustrative List of SSSBEs Activities

• Advertising Agencies

• Marketing Consultancy

• Industrial Consultancy

• Equipment Rental & Leasing

• Typing Centres

• Photocopying centres (Xeroxing)

• Industrial Photography

• Industrial R&D Labs

• Industrial Testing Labs• Desk Top Publishing

• Internet Browsing/ Setting up of Cyber Cafes

• Auto Repair, Services and Garages

• Documentary Films on themes like family planning, social forestry, energy conservation and

commercial advertising

• Laboratories engaged in testing of raw materials, finished products

• „Servicing Industry‟ Undertakings engaged in maintenance, repair, testing or servicing of all

types of vehicles & machinery of any description including electronic/electrical

equipment/instruments, i.e., measuring/control instruments, televisions, tape recorders, VCRs,

radios, transformers, motors, watches, etc.

17 April 2012

53

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 54/102

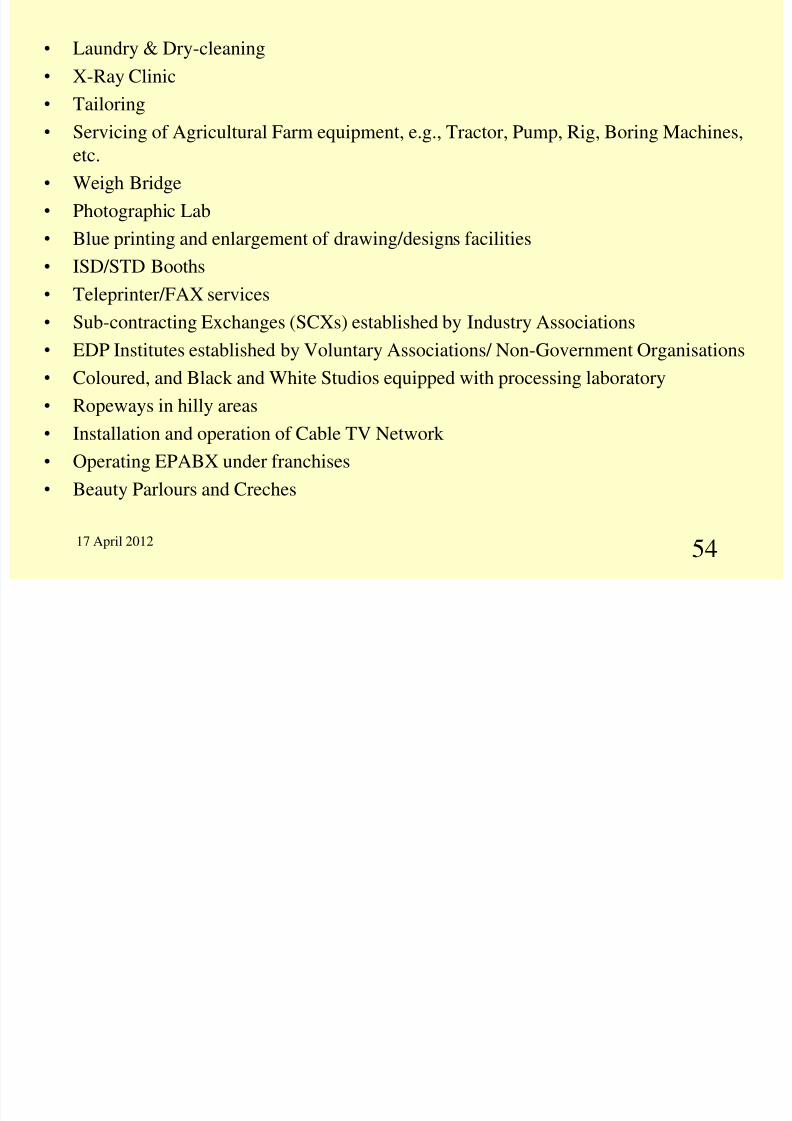

• Laundry & Dry-cleaning

• X-Ray Clinic

• Tailoring

• Servicing of Agricultural Farm equipment, e.g., Tractor, Pump, Rig, Boring Machines,

etc.

• Weigh Bridge

• Photographic Lab

• Blue printing and enlargement of drawing/designs facilities

• ISD/STD Booths

• Teleprinter/FAX services

• Sub-contracting Exchanges (SCXs) established by Industry Associations

• EDP Institutes established by Voluntary Associations/ Non-Government Organisations

• Coloured, and Black and White Studios equipped with processing laboratory

• Ropeways in hilly areas• Installation and operation of Cable TV Network

• Operating EPABX under franchises

• Beauty Parlours and Creches

17 April 2012

54

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 55/102

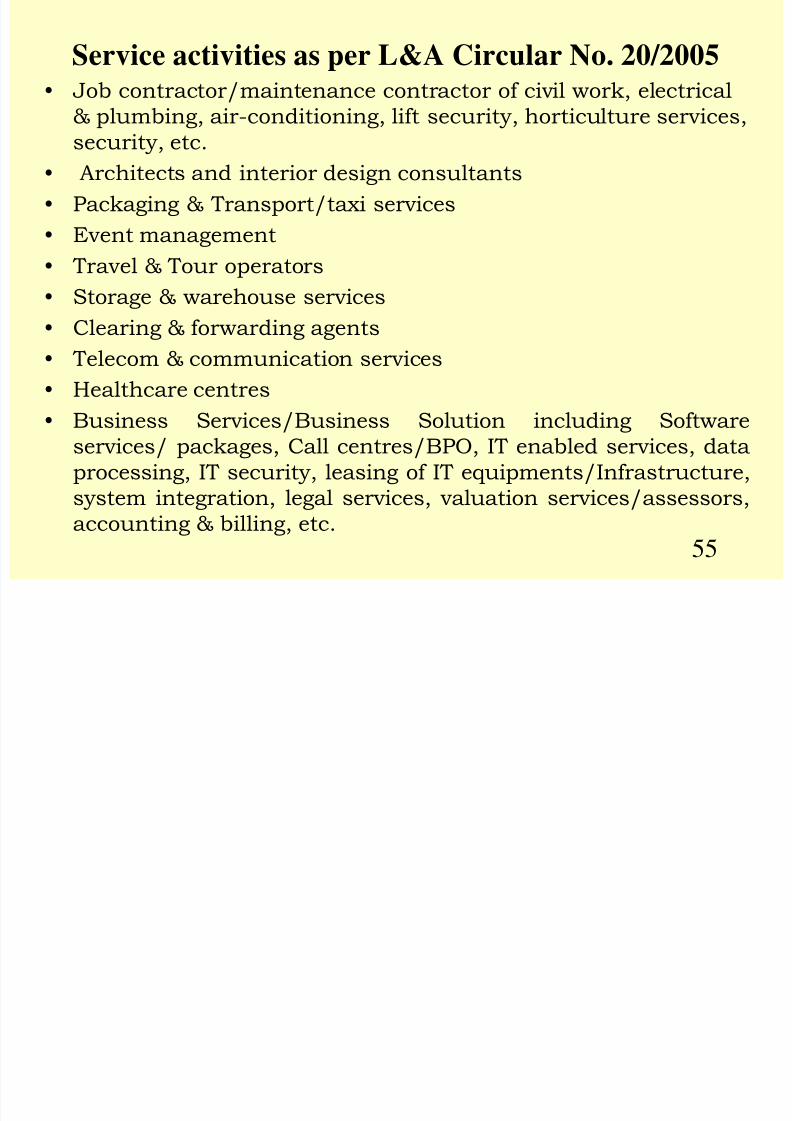

Service activities as per L&A Circular No. 20/2005• Job contractor/maintenance contractor of civil work, electrical

& plumbing, air-conditioning, lift security, horticulture services,

security, etc.• Architects and interior design consultants

• Packaging & Transport/taxi services

• Event management

• Travel & Tour operators

• Storage & warehouse services

• Clearing & forwarding agents

• Telecom & communication services

• Healthcare centres

• Business Services/Business Solution including Softwareservices/ packages, Call centres/BPO, IT enabled services, data

processing, IT security, leasing of IT equipments/Infrastructure,

system integration, legal services, valuation services/assessors,

accounting & billing, etc.

55

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 56/102

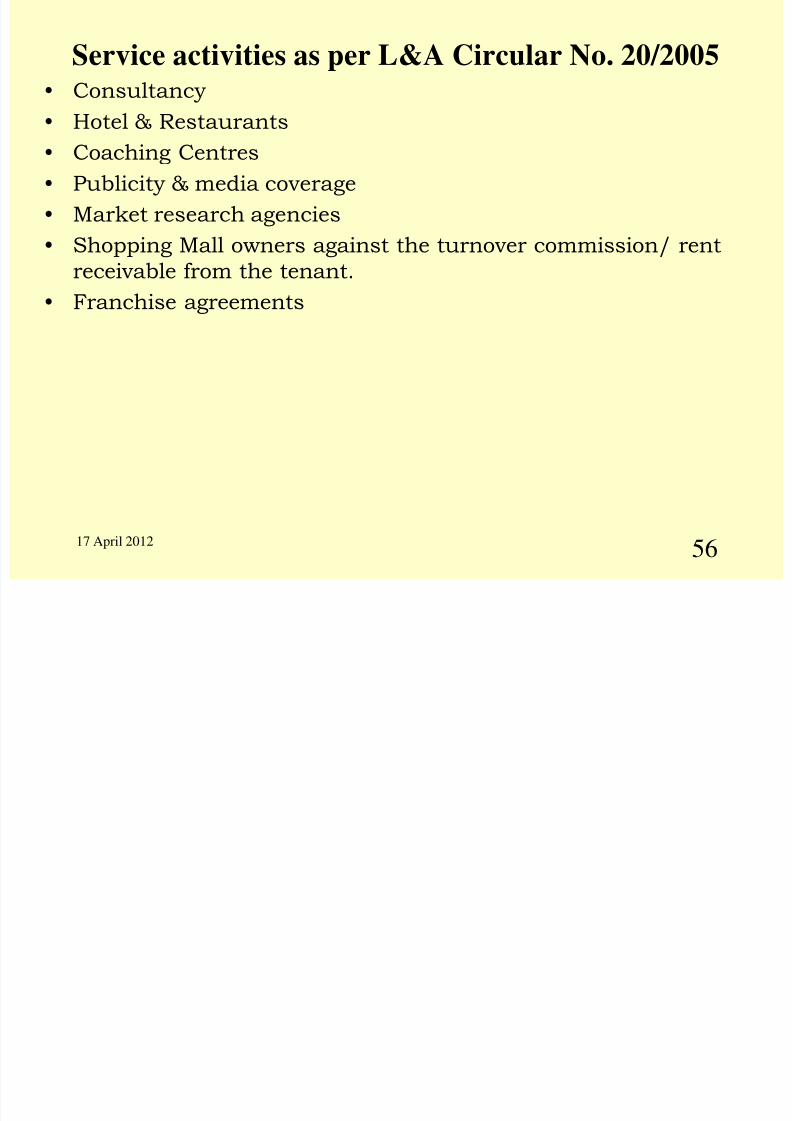

Service activities as per L&A Circular No. 20/2005• Consultancy

• Hotel & Restaurants

• Coaching Centres

• Publicity & media coverage

• Market research agencies

• Shopping Mall owners against the turnover commission/ rent

receivable from the tenant.• Franchise agreements

5617 April 2012

SCHEME FOR FINANCING RETAIL TRADE ACTIVITIES

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 57/102

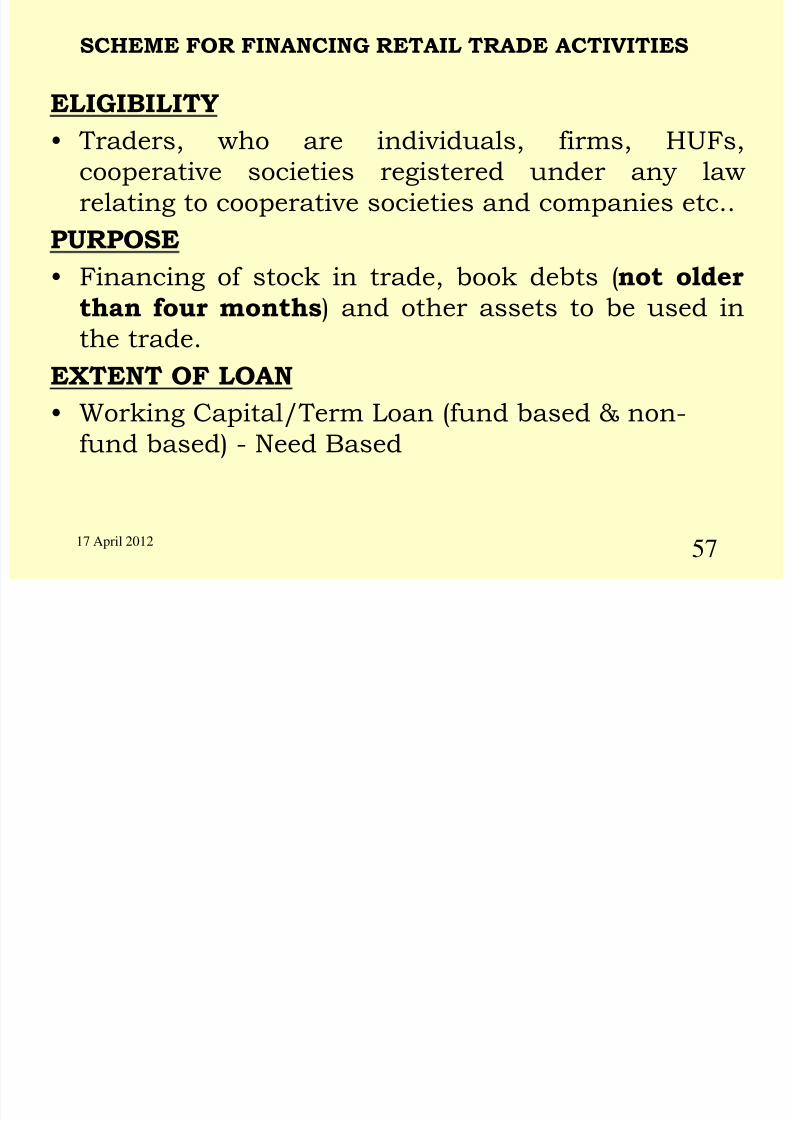

SCHEME FOR FINANCING RETAIL TRADE ACTIVITIES

ELIGIBILITY

• Traders, who are individuals, firms, HUFs,cooperative societies registered under any law

relating to cooperative societies and companies etc..

PURPOSE

• Financing of stock in trade, book debts (not olderthan four months) and other assets to be used in

the trade.

EXTENT OF LOAN

• Working Capital/Term Loan (fund based & non-fund based) - Need Based

17 April 2012

57

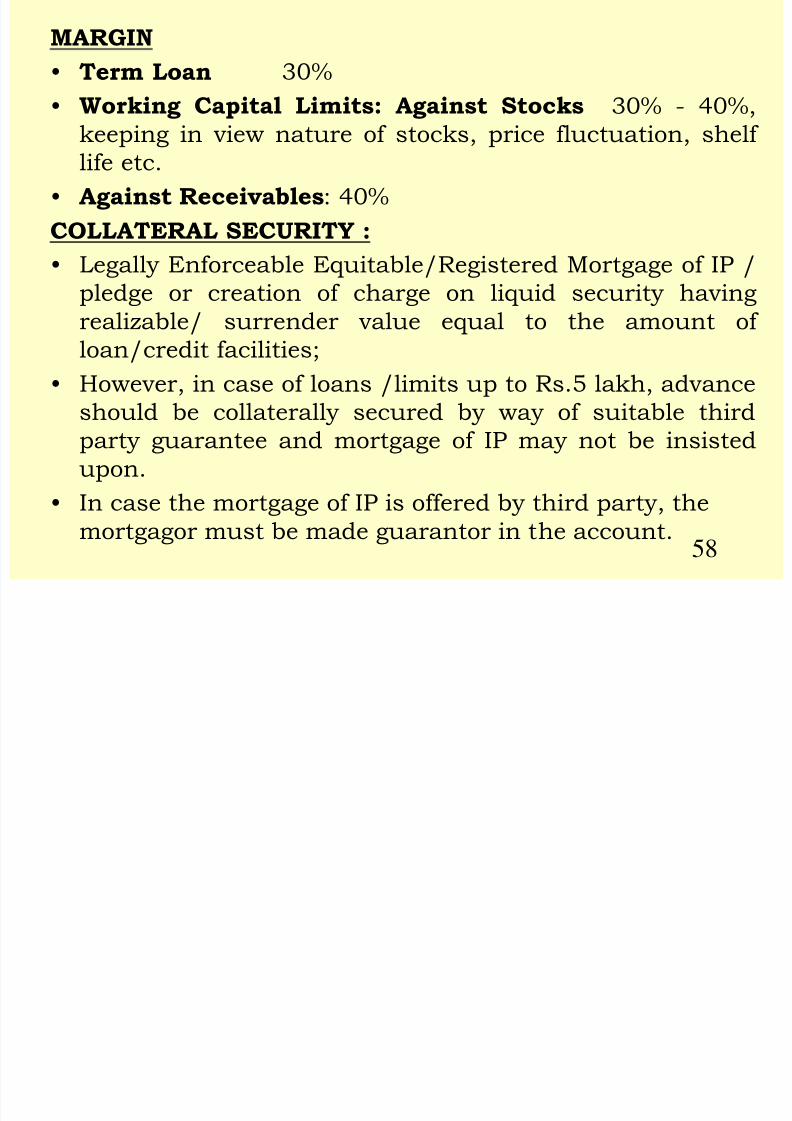

MARGIN

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 58/102

MARGIN

• Term Loan 30%

• Working Capital Limits: Against Stocks 30% - 40%,

keeping in view nature of stocks, price fluctuation, shelf life etc.

• Against Receivables: 40%

COLLATERAL SECURITY :

• Legally Enforceable Equitable/Registered Mortgage of IP /

pledge or creation of charge on liquid security having

realizable/ surrender value equal to the amount of

loan/credit facilities;

• However, in case of loans /limits up to Rs.5 lakh, advance

should be collaterally secured by way of suitable thirdparty guarantee and mortgage of IP may not be insisted

upon.

• In case the mortgage of IP is offered by third party, the

mortgagor must be made guarantor in the account.

58

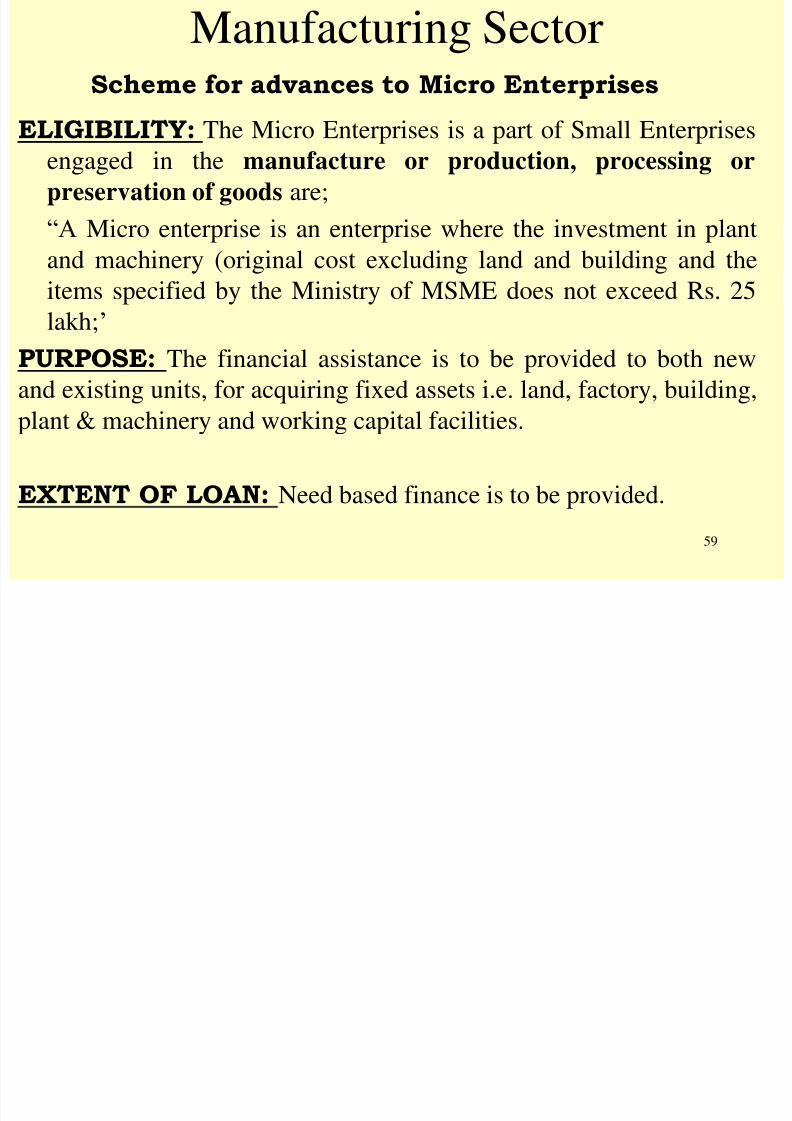

Manufacturing Sector

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 59/102

Manufacturing Sector

59

Scheme for advances to Micro Enterprises

ELIGIBILITY: The Micro Enterprises is a part of Small Enterprises

engaged in the manufacture or production, processing or

preservation of goods are;

“A Micro enterprise is an enterprise where the investment in plant

and machinery (original cost excluding land and building and the

items specified by the Ministry of MSME does not exceed Rs. 25

lakh;‟

PURPOSE: The financial assistance is to be provided to both new

and existing units, for acquiring fixed assets i.e. land, factory, building,

plant & machinery and working capital facilities.

EXTENT OF LOAN: Need based finance is to be provided.

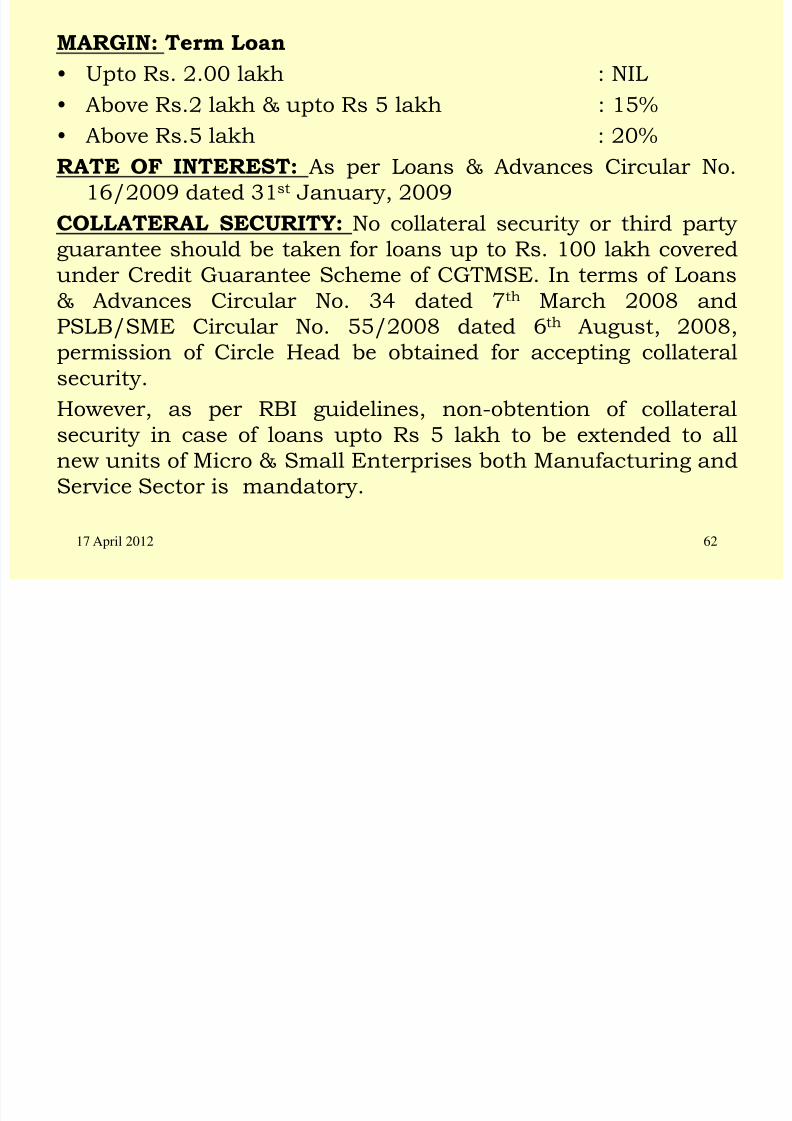

• MARGIN: C h C dit (H ) d T L

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 60/102

17 April 2012 60

• MARGIN: Cash Credit (Hyp.) and Term Loan

• Upto Rs. 2.00 lakh : NIL

• Above Rs.2 lakh & upto Rs 5 lakh : 15%

• Above Rs.5 lakh : 20%

RATE OF INTEREST: As per Loans & Advances

Circular No. 16/2009 dated 31st January, 2009

COLLATERAL SECURITY: No collateral security or third

party guarantee should be taken for loans up to Rs. 100 lakh

covered under Credit Guarantee Scheme of CGTMSE. In terms of

Loans & Advances Circular No. 34 dated 7th March 2008 and

PSLB/SME Circular No. 55/2008 dated 6th August, 2008,

permission of Circle Head be obtained for accepting collateral

security.However, as per RBI guidelines, non-obtention of collateral

security in case of loans upto Rs 5 lakh to be extended to all new

units of Micro & Small Enterprises both Manufacturing and

Service Sector is mandatory.

Scheme for acquisition of ISO 9000 certification

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 61/102

Scheme for acquisition of ISO 9000 certification

17 April 2012

61

OBJECTIVE: To promote quality management system in SSI

units with a view to strengthening their marketing and exportcapabilities.

PURPOSE: Financial assistance is to be provided for acquiring

ISO-9000 certification, e.g. expenses on consultancy,

documentation, audit certification fees, equipment and

calibrating instruments required would be taken into account for

determining the loan requirement.

EXTENT OF LOAN: Assistance under the scheme will be need

based, by way of Term Loan.

MARGIN: Term Loan

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 62/102

17 April 2012 62

MARGIN: Term Loan

• Upto Rs. 2.00 lakh : NIL

• Above Rs.2 lakh & upto Rs 5 lakh : 15%

• Above Rs.5 lakh : 20% RATE OF INTEREST: As per Loans & Advances Circular No.

16/2009 dated 31st January, 2009

COLLATERAL SECURITY: No collateral security or third party

guarantee should be taken for loans up to Rs. 100 lakh covered

under Credit Guarantee Scheme of CGTMSE. In terms of Loans& Advances Circular No. 34 dated 7th March 2008 and

PSLB/SME Circular No. 55/2008 dated 6th August, 2008,

permission of Circle Head be obtained for accepting collateral

security.

However, as per RBI guidelines, non-obtention of collateralsecurity in case of loans upto Rs 5 lakh to be extended to all

new units of Micro & Small Enterprises both Manufacturing and

Service Sector is mandatory.

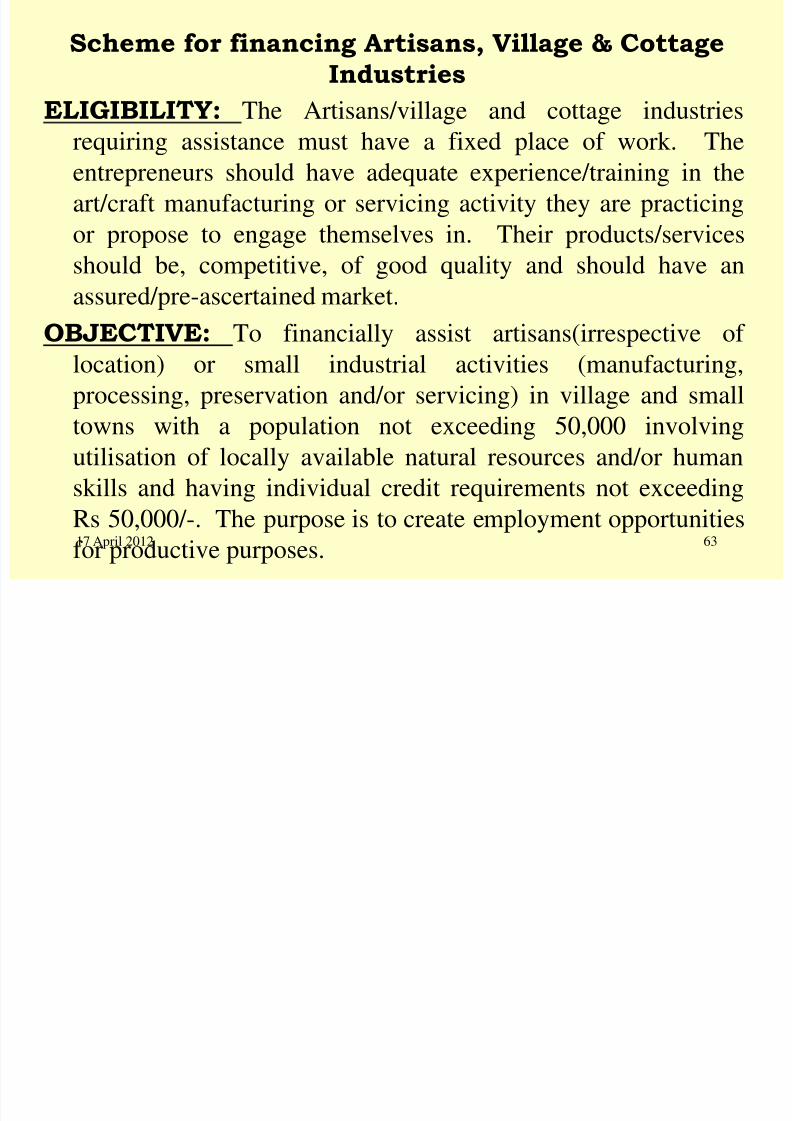

Scheme for financing Artisans Village & Cottage

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 63/102

Scheme for financing Artisans, Village & Cottage

Industries

17 April 2012 63

ELIGIBILITY: The Artisans/village and cottage industries

requiring assistance must have a fixed place of work. Theentrepreneurs should have adequate experience/training in the

art/craft manufacturing or servicing activity they are practicing

or propose to engage themselves in. Their products/services

should be, competitive, of good quality and should have an

assured/pre-ascertained market.

OBJECTIVE: To financially assist artisans(irrespective of

location) or small industrial activities (manufacturing,

processing, preservation and/or servicing) in village and small

towns with a population not exceeding 50,000 involving

utilisation of locally available natural resources and/or human

skills and having individual credit requirements not exceeding

Rs 50,000/-. The purpose is to create employment opportunities

for productive purposes.

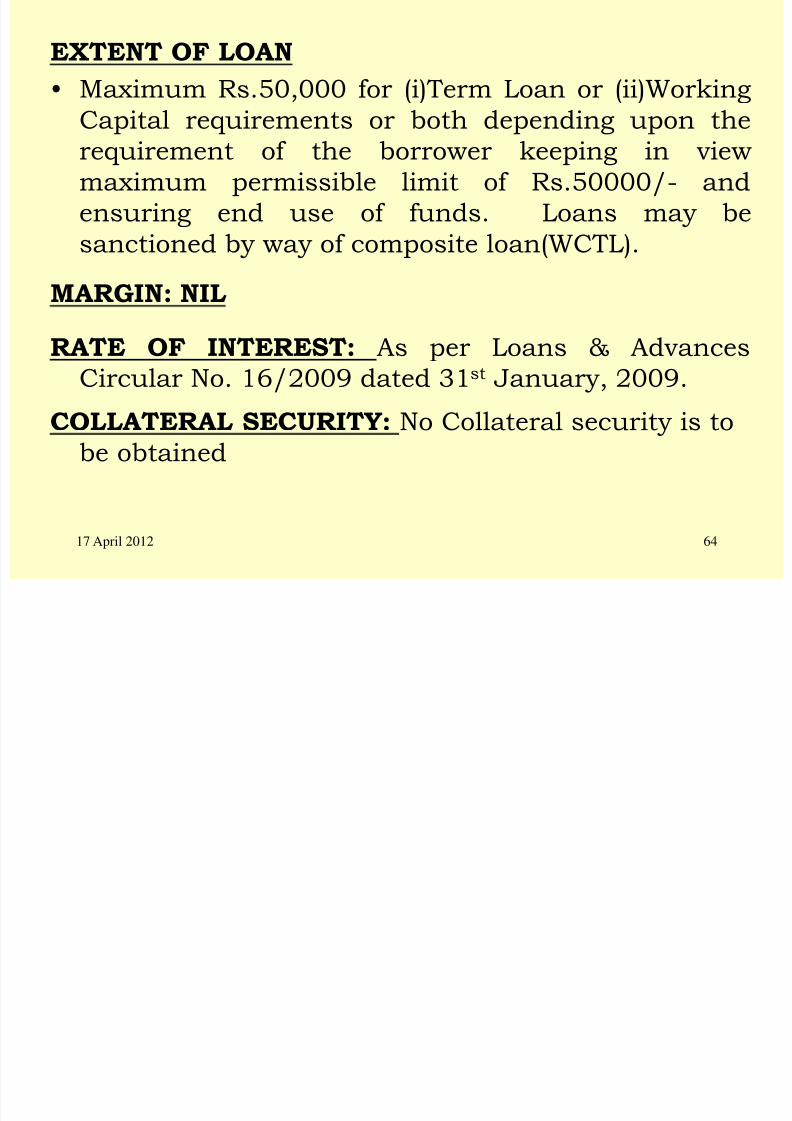

EXTENT OF LOAN

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 64/102

17 April 2012 64

EXTENT OF LOAN

• Maximum Rs.50,000 for (i)Term Loan or (ii)Working

Capital requirements or both depending upon the

requirement of the borrower keeping in viewmaximum permissible limit of Rs.50000/- and

ensuring end use of funds. Loans may be

sanctioned by way of composite loan(WCTL).

MARGIN: NIL

RATE OF INTEREST: As per Loans & Advances

Circular No. 16/2009 dated 31st January, 2009.

COLLATERAL SECURITY: No Collateral security is tobe obtained

Scheme for financing Craftsman & Qualified

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 65/102

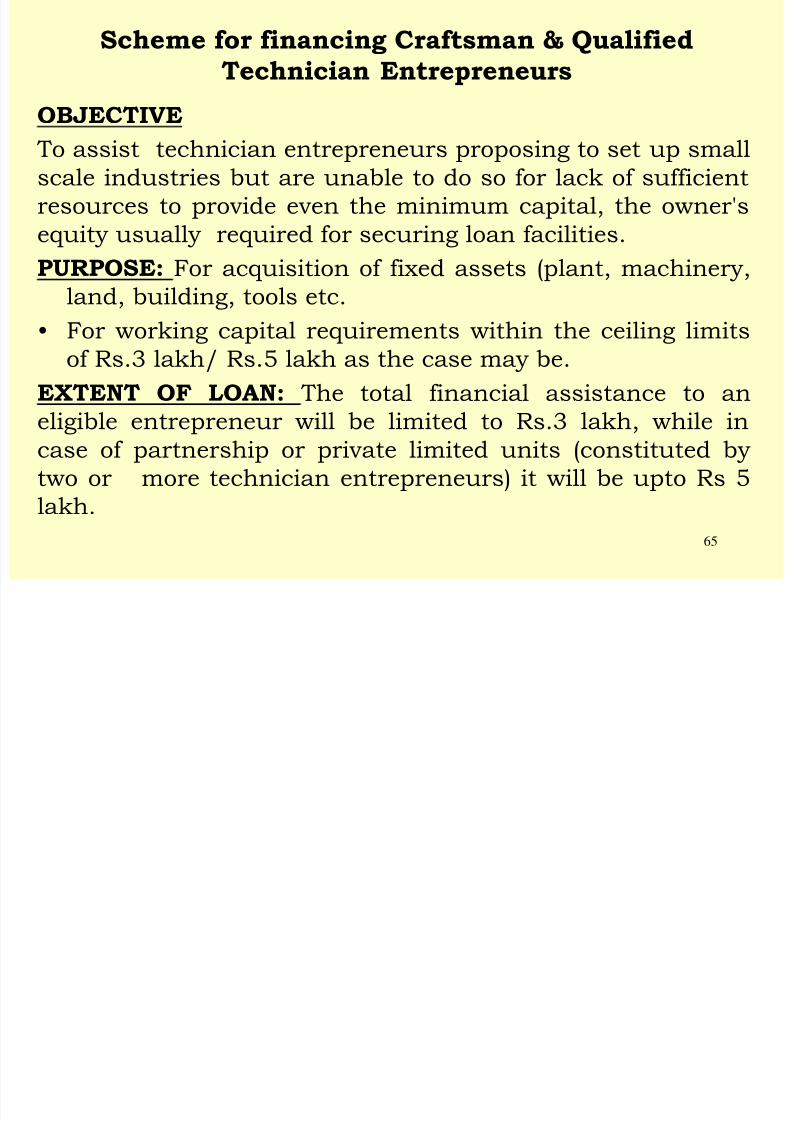

Scheme for financing Craftsman & Qualified

Technician Entrepreneurs

65

OBJECTIVE

To assist technician entrepreneurs proposing to set up smallscale industries but are unable to do so for lack of sufficient

resources to provide even the minimum capital, the owner's

equity usually required for securing loan facilities.

PURPOSE: For acquisition of fixed assets (plant, machinery,

land, building, tools etc.

• For working capital requirements within the ceiling limits

of Rs.3 lakh/ Rs.5 lakh as the case may be.

EXTENT OF LOAN: The total financial assistance to an

eligible entrepreneur will be limited to Rs.3 lakh, while incase of partnership or private limited units (constituted by

two or more technician entrepreneurs) it will be upto Rs 5

lakh.

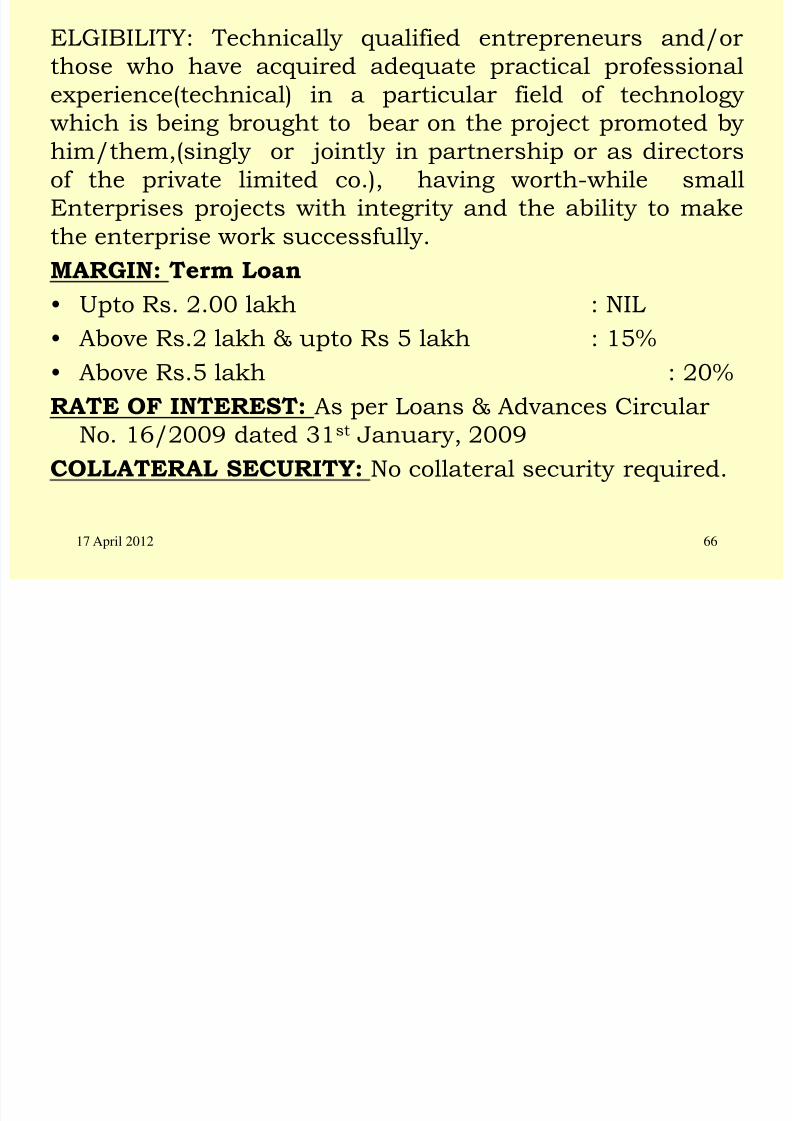

ELGIBILITY: Technically qualified entrepreneurs and/or

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 66/102

17 April 2012 66

y q p /

those who have acquired adequate practical professional

experience(technical) in a particular field of technology

which is being brought to bear on the project promoted by

him/them,(singly or jointly in partnership or as directorsof the private limited co.), having worth-while small

Enterprises projects with integrity and the ability to make

the enterprise work successfully.

MARGIN: Term Loan • Upto Rs. 2.00 lakh : NIL

• Above Rs.2 lakh & upto Rs 5 lakh : 15%

• Above Rs.5 lakh : 20%

RATE OF INTEREST: As per Loans & Advances CircularNo. 16/2009 dated 31st January, 2009

COLLATERAL SECURITY: No collateral security required.

Scheme for financing Handloom Weavers & Artisans

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 67/102

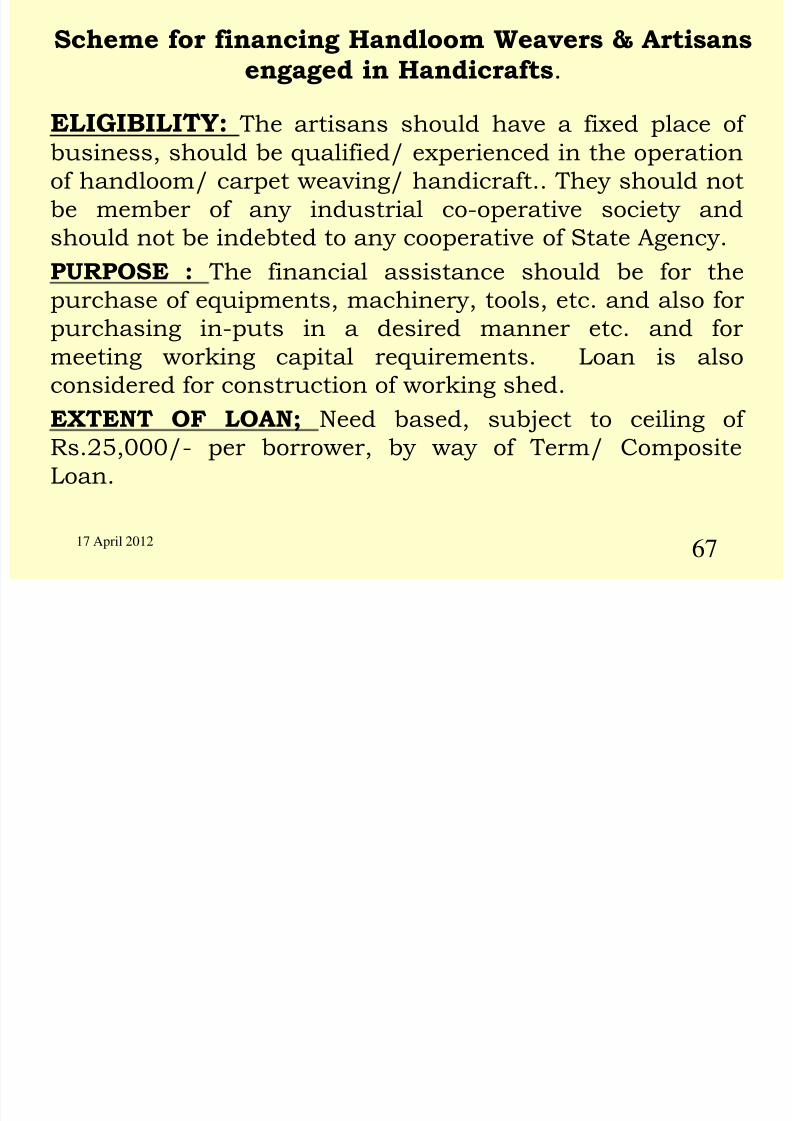

Scheme for financing Handloom Weavers & Artisansengaged in Handicrafts.

17 April 2012

67

ELIGIBILITY: The artisans should have a fixed place of

business, should be qualified/ experienced in the operationof handloom/ carpet weaving/ handicraft.. They should not

be member of any industrial co-operative society and

should not be indebted to any cooperative of State Agency.

PURPOSE : The financial assistance should be for thepurchase of equipments, machinery, tools, etc. and also for

purchasing in-puts in a desired manner etc. and for

meeting working capital requirements. Loan is also

considered for construction of working shed.

EXTENT OF LOAN; Need based, subject to ceiling of Rs.25,000/- per borrower, by way of Term/ Composite

Loan.

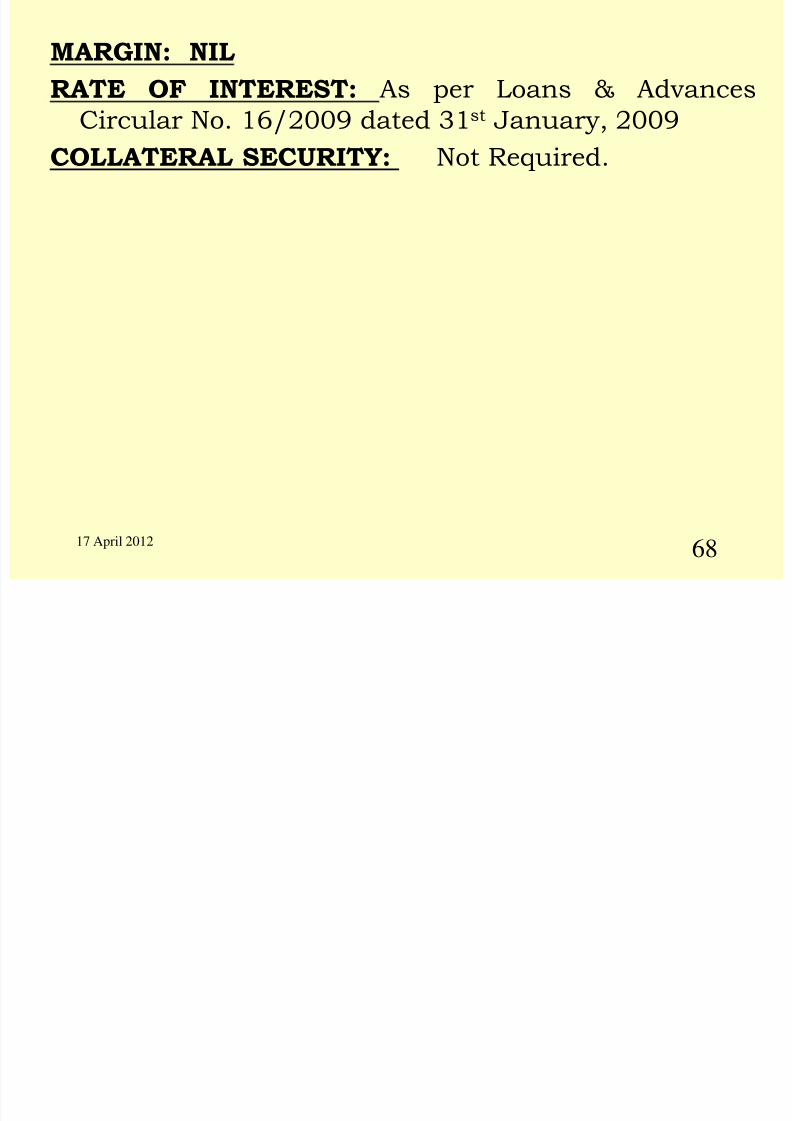

MARGIN NIL

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 68/102

17 April 2012

68

MARGIN: NIL

RATE OF INTEREST: As per Loans & Advances

Circular No. 16/2009 dated 31st January, 2009

COLLATERAL SECURITY: Not Required.

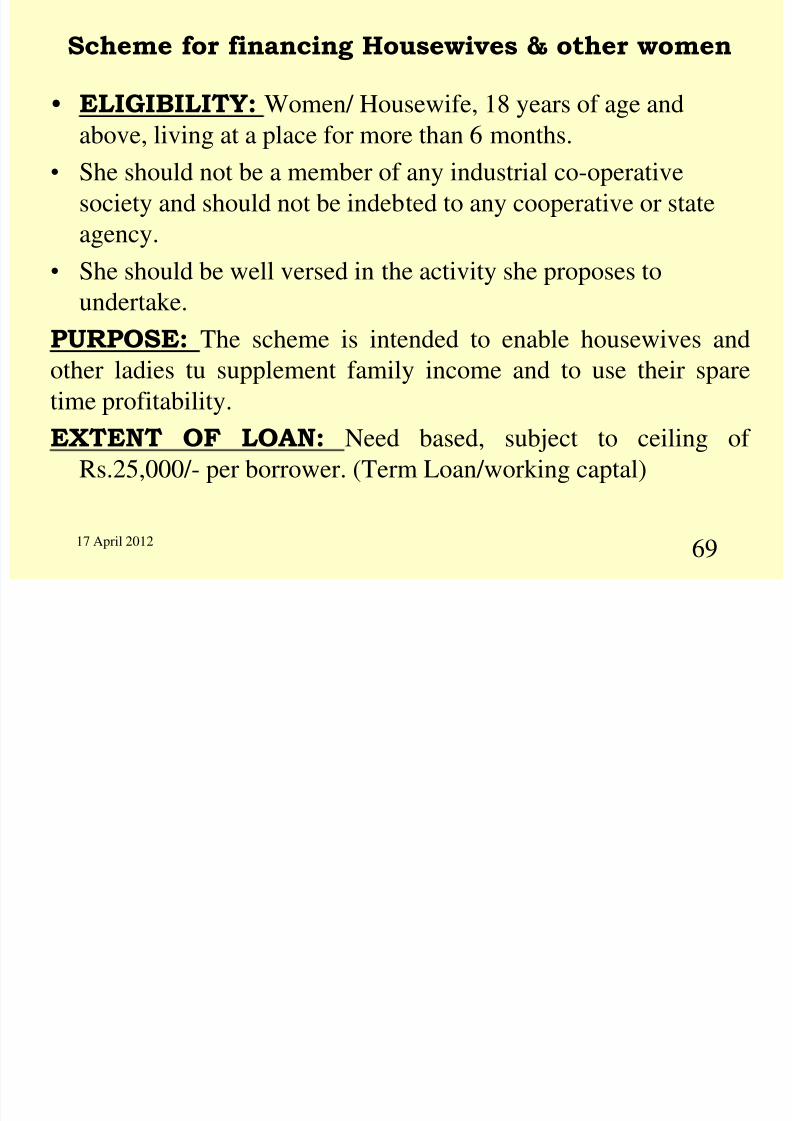

Scheme for financing Housewives & other women

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 69/102

Scheme for financing Housewives & other women

17 April 2012

69

• ELIGIBILITY: Women/ Housewife, 18 years of age and

above, living at a place for more than 6 months.• She should not be a member of any industrial co-operative

society and should not be indebted to any cooperative or state

agency.

• She should be well versed in the activity she proposes toundertake.

PURPOSE: The scheme is intended to enable housewives and

other ladies tu supplement family income and to use their spare

time profitability.

EXTENT OF LOAN: Need based, subject to ceiling of

Rs.25,000/- per borrower. (Term Loan/working captal)

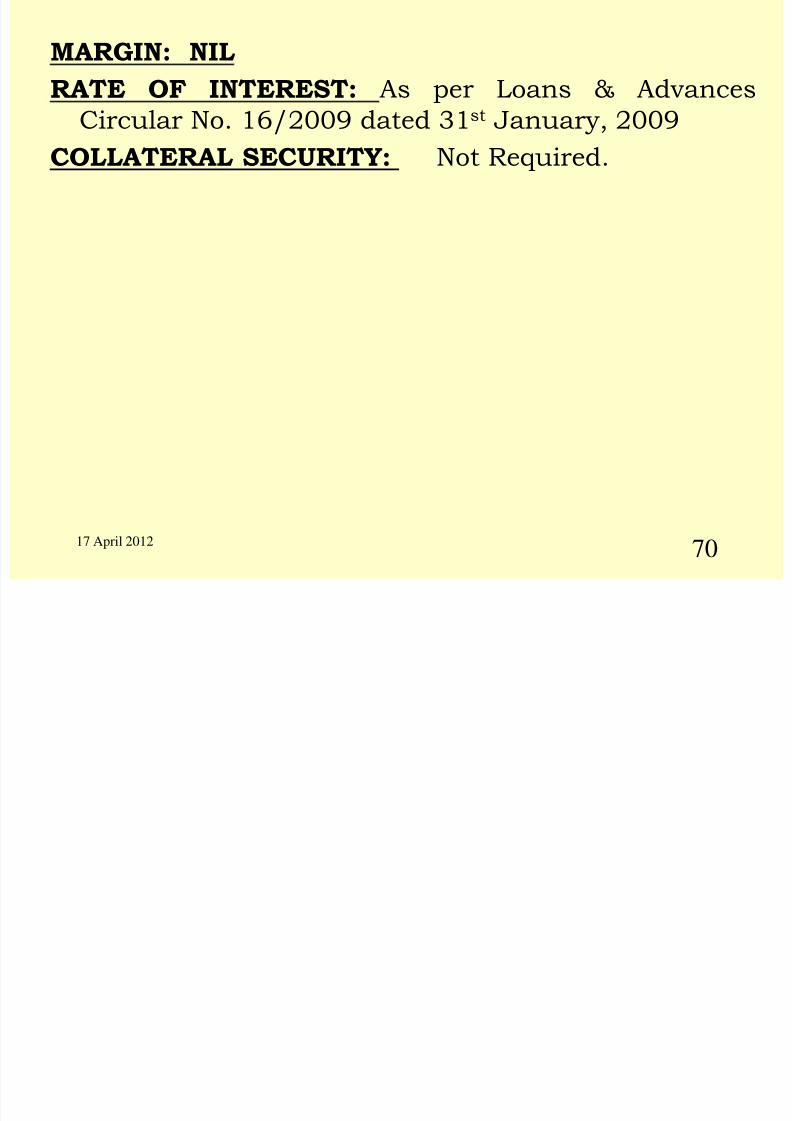

MARGIN: NIL

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 70/102

17 April 2012

70

MARGIN: NIL

RATE OF INTEREST: As per Loans & Advances

Circular No. 16/2009 dated 31st January, 2009

COLLATERAL SECURITY: Not Required.

Scheme for financing Small Enterprise

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 71/102

71

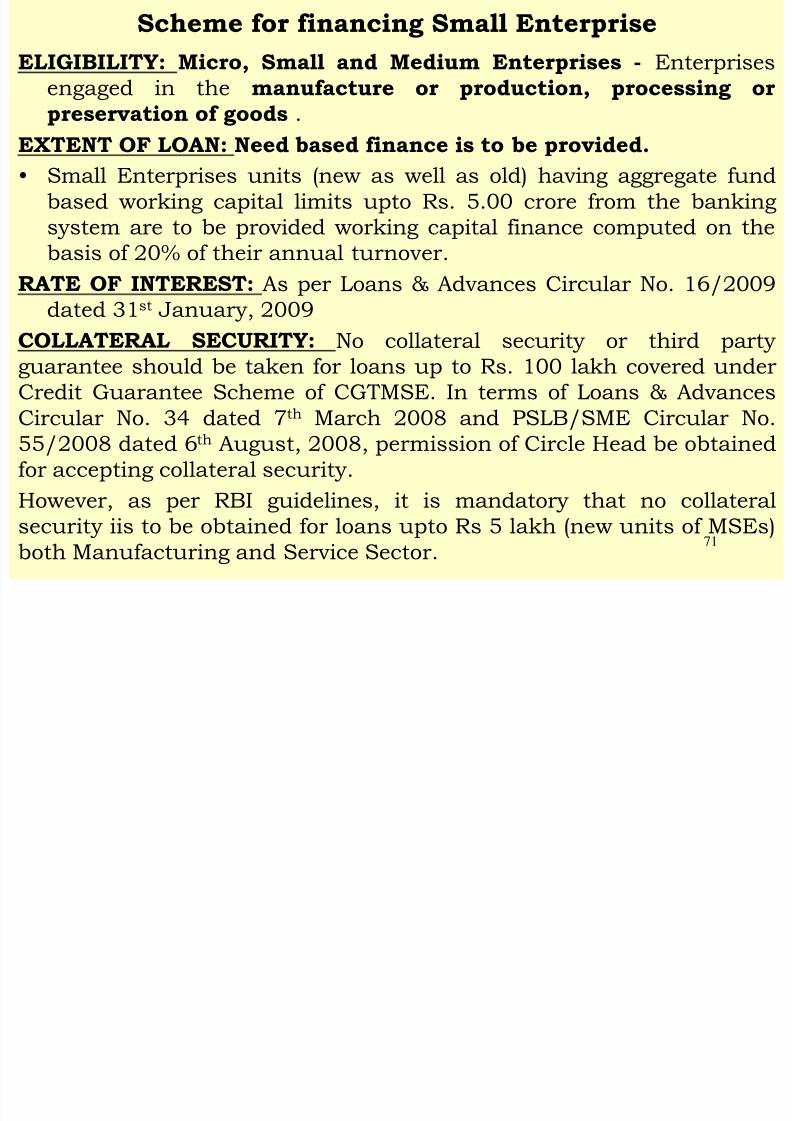

ELIGIBILITY: Micro, Small and Medium Enterprises - Enterprises

engaged in the manufacture or production, processing or

preservation of goods .

EXTENT OF LOAN: Need based finance is to be provided.• Small Enterprises units (new as well as old) having aggregate fund

based working capital limits upto Rs. 5.00 crore from the banking

system are to be provided working capital finance computed on the

basis of 20% of their annual turnover.

RATE OF INTEREST: As per Loans & Advances Circular No. 16/2009dated 31st January, 2009

COLLATERAL SECURITY: No collateral security or third party

guarantee should be taken for loans up to Rs. 100 lakh covered under

Credit Guarantee Scheme of CGTMSE. In terms of Loans & Advances

Circular No. 34 dated 7th March 2008 and PSLB/SME Circular No.55/2008 dated 6th August, 2008, permission of Circle Head be obtained

for accepting collateral security.

However, as per RBI guidelines, it is mandatory that no collateral

security iis to be obtained for loans upto Rs 5 lakh (new units of MSEs)

both Manufacturing and Service Sector.

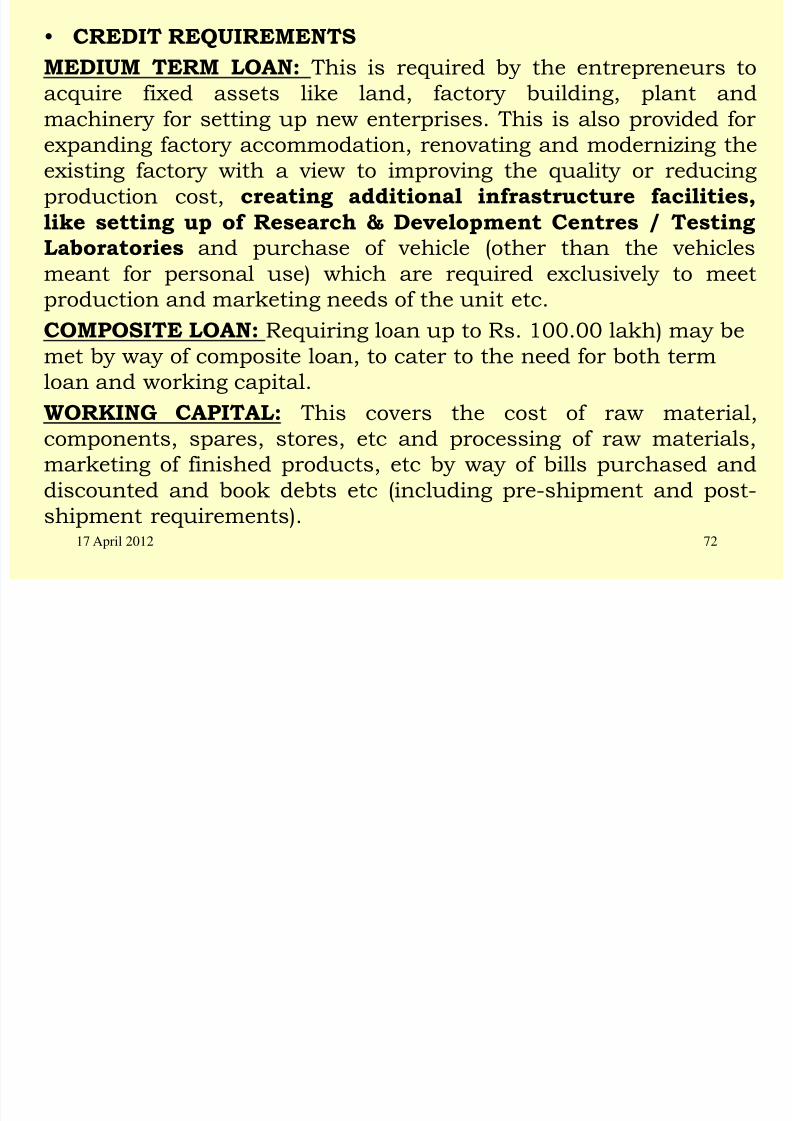

• CREDIT REQUIREMENTS

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 72/102

17 April 2012 72

MEDIUM TERM LOAN: This is required by the entrepreneurs to

acquire fixed assets like land, factory building, plant and

machinery for setting up new enterprises. This is also provided for

expanding factory accommodation, renovating and modernizing theexisting factory with a view to improving the quality or reducing

production cost, creating additional infrastructure facilities,

like setting up of Research & Development Centres / TestingLaboratories and purchase of vehicle (other than the vehicles

meant for personal use) which are required exclusively to meetproduction and marketing needs of the unit etc.

COMPOSITE LOAN: Requiring loan up to Rs. 100.00 lakh) may be

met by way of composite loan, to cater to the need for both term

loan and working capital.

WORKING CAPITAL: This covers the cost of raw material,components, spares, stores, etc and processing of raw materials,

marketing of finished products, etc by way of bills purchased and

discounted and book debts etc (including pre-shipment and post-

shipment requirements).

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 73/102

To provide hassle free financial support to Artisans and to make

credit delivery simple and easy

ELIGIBILITY:

All artisans involved in production/ manufacturing process (andotherwise eligible for credit facilities for carrying out the

proposed activities under any of the existing bank schemes)

would be eligible. Preference would be given to artisans

registered with Development Commissioner (Handicrafts) and Thrust in financing would be on clusters of artisans and

artisans who have joined to form Self Help Groups (SHGs).

NATURE OF LIMIT : Term Loan & Cash Credit Limit up to Rs.

2 lakh

• The Development Commissioner (Handicrafts) will pay/re-

imburse one time Guarantee money and Annual service fee

to bank for obtention of guarantee cover under creditguarantee scheme of CGTSI to facilitate flow of credit to the

Handicraft Artisans.

17 April 2012

73

PNB ARTISANS CREDIT CARD SCHEME

PNB LAGHU UDYAMI CREDIT CARD SCHEME

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 74/102

To provide hassle free financial support to Small businessunits, Retail Traders, Artisans, Village Industries, Small Scale

Industrial Units, Small Scale Services & Business Enterprises(SSSBEs) and Tiny Units, Professionals and Self EmployedPersons, etc.

• ELIGIBILITY: Borrowers belonging to aforesaid categoriesenjoying Cash Credit limits upto Rs 10 lakh and whose dealingswith the bank have been satisfactory for the last three years are

eligible for issuance of Laghu Udyami Credit Card.• EXTENT OF LIMIT: CC limit Max.upto Rs 10 lakh

• ASSESSMENT OF CREDIT CARD LIMIT

• (i) For small business, retail traders, etc. 20% of the annualturnover,

• (ii) For professionals and self-employed persons, 50% of their

gross annual income as per Income Tax return.• (iii) For Small Scale Industrial Units, Small Scale Services &

Business Enterprises (SSSBEs) including tiny sector units theassessment norms in vogue as per the Nayak Committeerecommendations.

17 April 2012

74

PNB LAGHU UDYAMI CREDIT CARD SCHEME

PNB SME Sahayog Scheme: is a new product , designed to

meet the unforeseen expenditure of the small enterprises with

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 75/102

meet the unforeseen expenditure of the small-enterprises with

excellent track record.

75

ELIGIBILITY: The scheme is applicable to existing borrowers

whose accounts have been classified as standard assets as on 31

March for the last 3 consecutive years.

(ii)To begin with, this facility may be extended to the existing rated

borrowers enjoying credit limits above Rs.20 lakh.

(iii)For sanctioned limits (Term loan & working capital) of above

Rs.20 lakh, the threshold credit rating should be „BB' as on the

closing of previous financial year. However, credit risk rating for

any of the earlier years should not be below 'B'.

EXTENT OF LOAN: The eligible borrowers will be sanctioned aspecial credit limit for an amount equal to 20% of the aggregate

working capital limits (i.e. fund based and non fund based

separately) sanctioned to the unit, subject to a maximum of Rs.25

lakh.

PORPUSE: The limit can be utilized for contingencies

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 76/102

17 April 2012 76

PORPUSE: The limit can be utilized for contingencies

like additional purchase of raw materials including

packing materials/handling charges for the

execution of bulk orders, taking part innational/international trade exhibitions for creating

market base, payment of consultancy charges,repairs to machinery, labour payments, etc.

RATE OF INTEREST: As per Loans & AdvancesCircular No. 16/2009 dated 31st January, 2009

COLLATERAL SECURITY: Collateral security be obtained as

per bank's extant guidelines. The charge on available security by

way of primary/collateral to the existing sanctioned limits will be

extended to cover the clean cash credit limit.

PNB Green Scheme : CREDIT FACILITY TO SSIUNITS - Five per cent Green Credit Facility for

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 77/102

p y

clearance of statutory dues.

77

ELIGIBILITY: All Micro & Small Enterprises units

PURPOSE: In order to meet payment of statutory duesexclusively like income tax, sales tax, excise duty and

other expenses like electricity charges, custom duties,

telephone expenses by SSI units in emergent

circumstances, bank will provide/ sanction 5% GreenCash Credit facility maximum upto Rs.1.00 lakh of

the fund based sanction limit/assessed permissible

bank finance, over & above adhoc facility or Credit

Facility availed by unit under PNB SME Sahayog. This

facility would be available to the MSEs of Standard

Category, who are banking with us for at least one

year. The facility will be allowed by the Incumbents Incharge

without referring the matter to higher authorities

Concessions Available to Micro & Small Enterprises

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 78/102

Concessions Available to Micro & Small Enterprises

• No Collateral Security for Loans up to Rs. 100 lakh. As per RBI

guidelines- Non-obtention of collateral security in case of loans

upto Rs 5 lakh to be extended to all new units of Micro & Small

Enterprises both Manufacturing and Service Sector is

mandatory.

• Composite Loan Limit up to Rs. 100 lakh.

• Simplified Loan Application Forms for Loans up to Rs. 50 lakh.

• No Processing/Upfront fee for loans up to Rs. 2 lakh.• Interest concessions in the range of 0.25% to 0.50% for SMERA

& CRISIL rated borrowers.

• Financing of Pre-operative expenses, where no tangible primary

security is being created, be considered to Small Enterprises

not exceeding 10% of the project cost, within the total financingof the project. Further, it should be ensured that security

created out of loan amount and other collateral securities etc

are adequate to cover such pre-operative expenses.

17 April 2012

78

NEF SCHEME- Soft Loan Assistance

OBJECTIVE : The objective of NEF Scheme is to provide

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 79/102

OBJECTIVE : The objective of NEF Scheme is to provide

equity type support to entrepreneurs for setting up new

projects in tiny/small scale sector, for undertaking

expansion, modernisation, technology upgradation anddiversification by existing tiny, SSI and service

enterprises and for rehabilitation of viable sick units in

the SSI Sector which fulfill the specified eligibility criteria,

irrespective of location.

ELIGIBILITY CRITERIA: All new and existingManufacturing & service enterprises excluding SRTO.

Assistance to Service Enterprises liked with acquisition

for fixed assets only.

AMOUNT OF ASSISTANCE: Amount as may be required tomeet the gap in equity as per prescribed debt equity

norm, after taking into account promoters’ contribution,

subject to a maximum of 25% of project cost or Rs.10.00

lakh per project, whichever is lower.

79

PROJECT COST

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 80/102

PROJECT COST

• Project cost (including margin money for working

capital) should not exceed Rs.50 lakh in the case of

new projects. In the case of existing units andservice enterprises, the total outlay, including the

proposed outlay on expansion/

modernisation/technology upgradation/

diversification of rehabilitation should not exceedRs.50 lakh.

• PROMOTER’S CONTRIBUTION : Minimum 10% of

the project cost.

• DEBT EQUITY RATIO: 65:35 or 1.857:1 (excludingState Investment Subsidy). However, a flexible

approach may be followed in the case of

rehabilitation proposals.

80

Mahila Udyam Nidhi Yojana

OBJECTIVE T id ft l (Q i it ) i t

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 81/102

OBJECTIVE: To provide soft loan (Quasi equity) assistance

to women entrepreneurs besides usual term loans for

setting up industrial units in the small scale and tiny sector

and undertaking service activities eligible for assistanceunder refinance scheme.

ELIGIBILITY : a) New projects in tiny and small scale

sectors for manufacture, preservation or processing of

goods [Tiny enterprises would include all industrial units

and service industries (except Road Transport Operators)

satisfying the investment ceiling prescribed for micro

enterprises].

b) Existing tiny and small scale industrial units and

service enterprises as mentioned above [including thosewhich have availed of MUN assistance earlier], undertaking

expansion, modernisation, technology upgradation and

diversification.

81

NATURE AND EXTENT OF ASSISTANCE: Soft

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 82/102

NATURE AND EXTENT OF ASSISTANCE: Soft

loan upto 25% of the project cost with a ceiling of Rs

2.50 lakh per project to meet the gap in equity as per

prescribed Debt Equity Ratio(DER) of 1.857:1(excluding State subsidy which may be retained for

meeting working capital) after taking into account the

promotors’ own contribution equivalent to 10% of the

project cost.PROJECT OUTLAY: Project cost(including margin

money for working capital) should not exceed Rs 10.00

lakh in case of new projects. In the case of existing

units and service enterprises, the outlay on expansion

/ modernisation / technology upgradation, or

diversification or rehabilitation should not exceed Rs

10.00 lakh per project.

82

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 83/102

17 April 2012

83

CREDIT

GUARANTEE

FUND T RUST SCHEME

FORMICRO & SMALL

ENTERPRISES

SALIENT FEATURES - CGTMSE

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 84/102

84

• Facilitates availment of credit by ALL NEW AND

EXISTING MICRO AND SMALL ENTERPRISES(BOTH IN THE MANUFACTURING SECTOR AS

WELL AS IN THE SERVICE SECTOR) except

advances to Retail Trade & EducationalInstitutions) from formal banking channel purely on

the viability of the projects.

• Maximum loan guaranteed by CGTMSE is Rs.100

lakh per Micro & Small Enterprises unit for fund

based & Non Fund Based facilities. However, the

loan amount may be more than Rs 100 lakh

• Amount in default of a borrowing unit is shared

between CGTMSE and the Lender in the ratio of 3:1

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 85/102

17 April 2012

85

ADDITIONAL CREDIT FACILITIES –

Eligible for Credit Guarantee Cover

• The additional credit facilities sanctioned upto

Rs. 100 lakh per borrower, subsequently,

without collateral security and / or third party

guarantee to such Micro & Small Enterprises

units, can be covered under the GuaranteeScheme.

• The decision to release the collateral security

and / or third party guarantee in respect of the

existing credit facilities extended to the eligibleSSI units have been left to the discretion of the

respective bank / lending institution (MLI).

d C d

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 86/102

17 April 2012

86

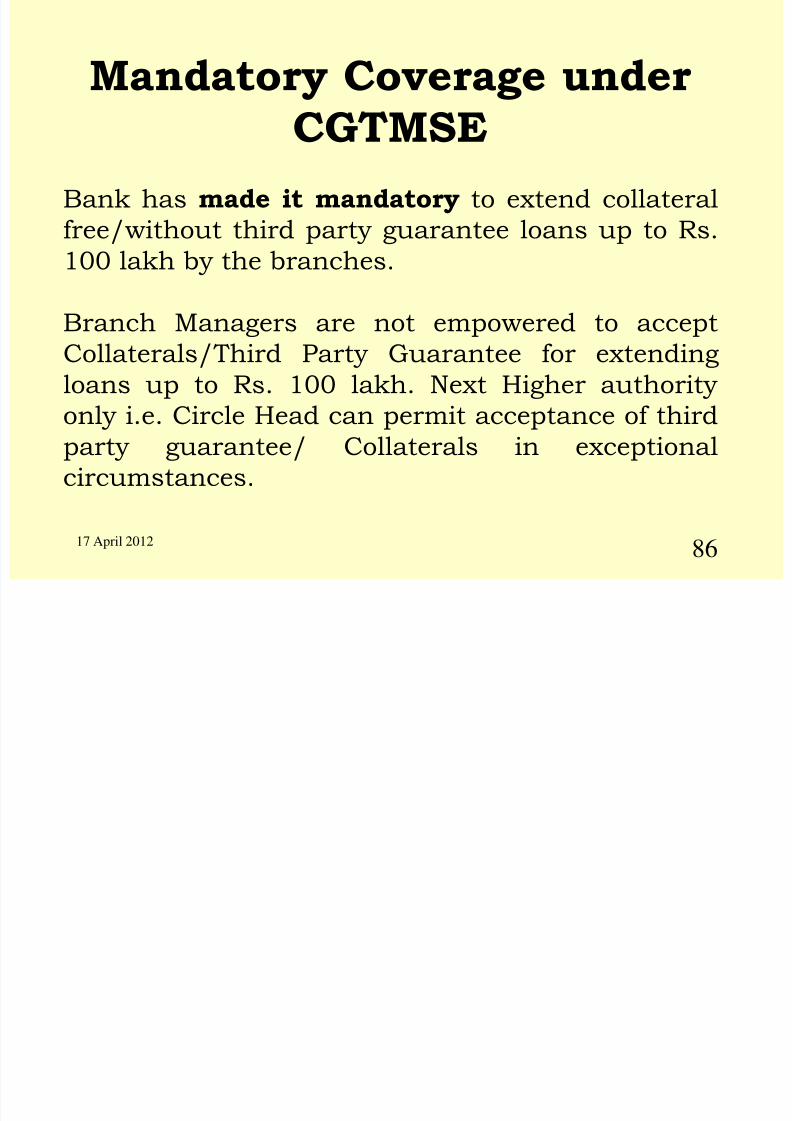

Mandatory Coverage under

CGTMSEBank has made it mandatory to extend collateral

free/without third party guarantee loans up to Rs.

100 lakh by the branches.

Branch Managers are not empowered to accept

Collaterals/Third Party Guarantee for extending

loans up to Rs. 100 lakh. Next Higher authority

only i.e. Circle Head can permit acceptance of thirdparty guarantee/ Collaterals in exceptional

circumstances.

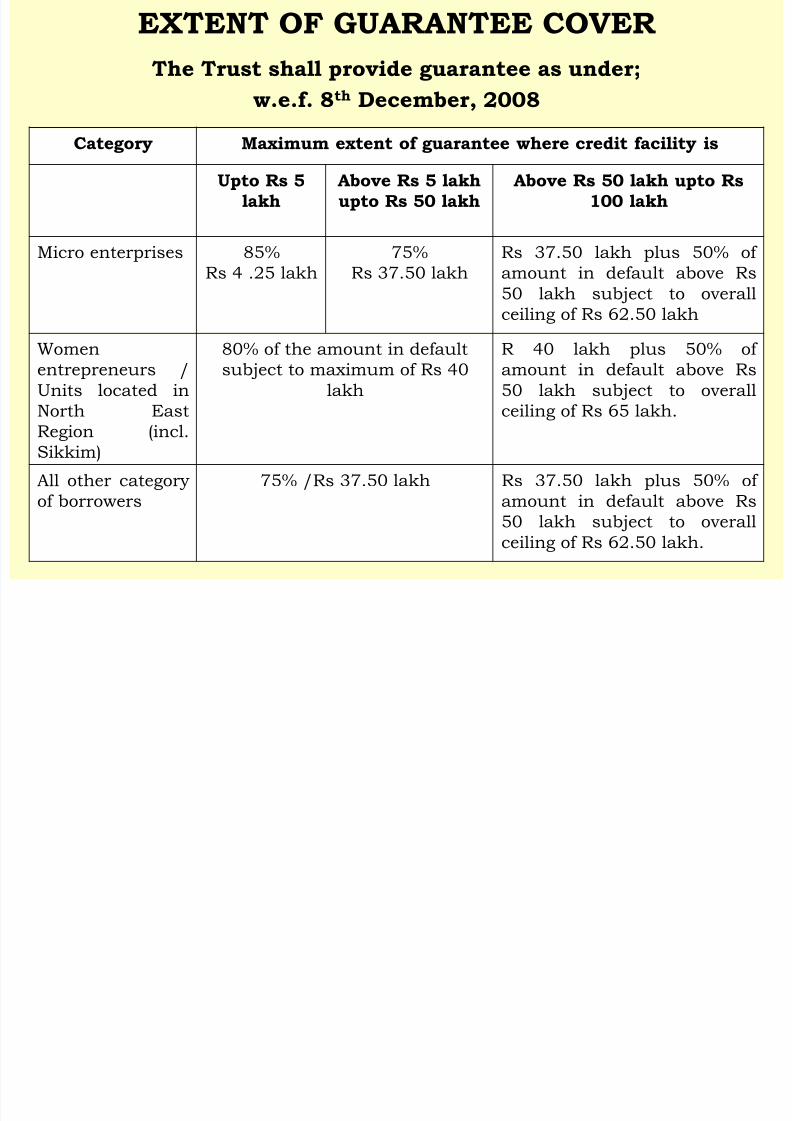

EXTENT OF GUARANTEE COVER

Th T h ll id d

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 87/102

The Trust shall provide guarantee as under;

w.e.f. 8th December, 2008

17 April 2012 87

Category Maximum extent of guarantee where credit facility is

Upto Rs 5

lakh

Above Rs 5 lakh

upto Rs 50 lakh

Above Rs 50 lakh upto Rs

100 lakh

Micro enterprises 85%

Rs 4 .25 lakh

75%

Rs 37.50 lakh

Rs 37.50 lakh plus 50% of

amount in default above Rs

50 lakh subject to overall

ceiling of Rs 62.50 lakh

Women

entrepreneurs /

Units located in

North East

Region (incl.

Sikkim)

80% of the amount in default

subject to maximum of Rs 40

lakh

R 40 lakh plus 50% of

amount in default above Rs

50 lakh subject to overall

ceiling of Rs 65 lakh.

All other category

of borrowers

75% /Rs 37.50 lakh Rs 37.50 lakh plus 50% of

amount in default above Rs

50 lakh subject to overall

ceiling of Rs 62.50 lakh.

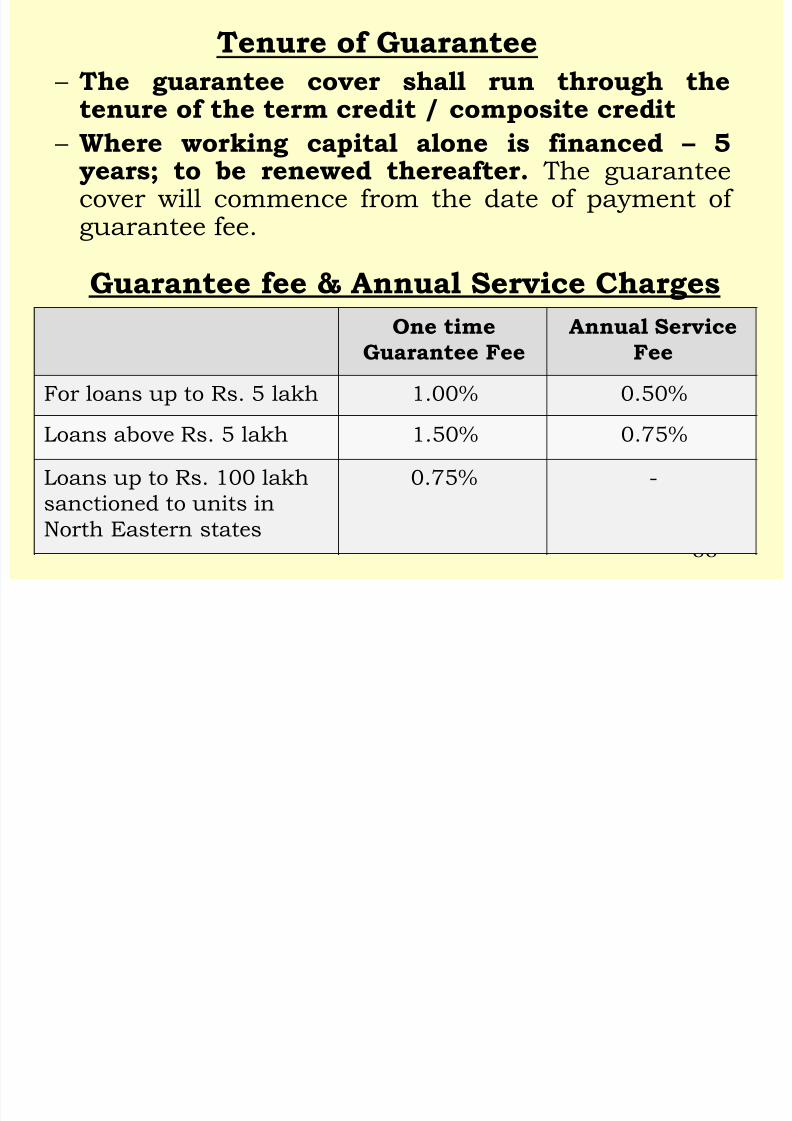

Tenure of Guarantee

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 88/102

17 April 2012

88

– The guarantee cover shall run through thetenure of the term credit / composite credit

– Where working capital alone is financed – 5years; to be renewed thereafter. The guaranteecover will commence from the date of payment of guarantee fee.

Guarantee fee & Annual Service ChargesOne time

Guarantee Fee

Annual Service

Fee

For loans up to Rs. 5 lakh 1.00% 0.50%

Loans above Rs. 5 lakh 1.50% 0.75%

Loans up to Rs. 100 lakh

sanctioned to units in

North Eastern states

0.75% -

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 89/102

17 April 2012

89

Incentives to banks

CGTMSE guaranteed loans carry

– Zero per cent risk weight – Zero per cent provisions

RBI Circular DBOD BP.BC.128/2.04.048/00-01 dated June 7,2001

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 90/102

TECHNOLOGYUPGRADATION SCHEME

FORSMALL ENTERPRISES

SECTOR

17 April 2012

90

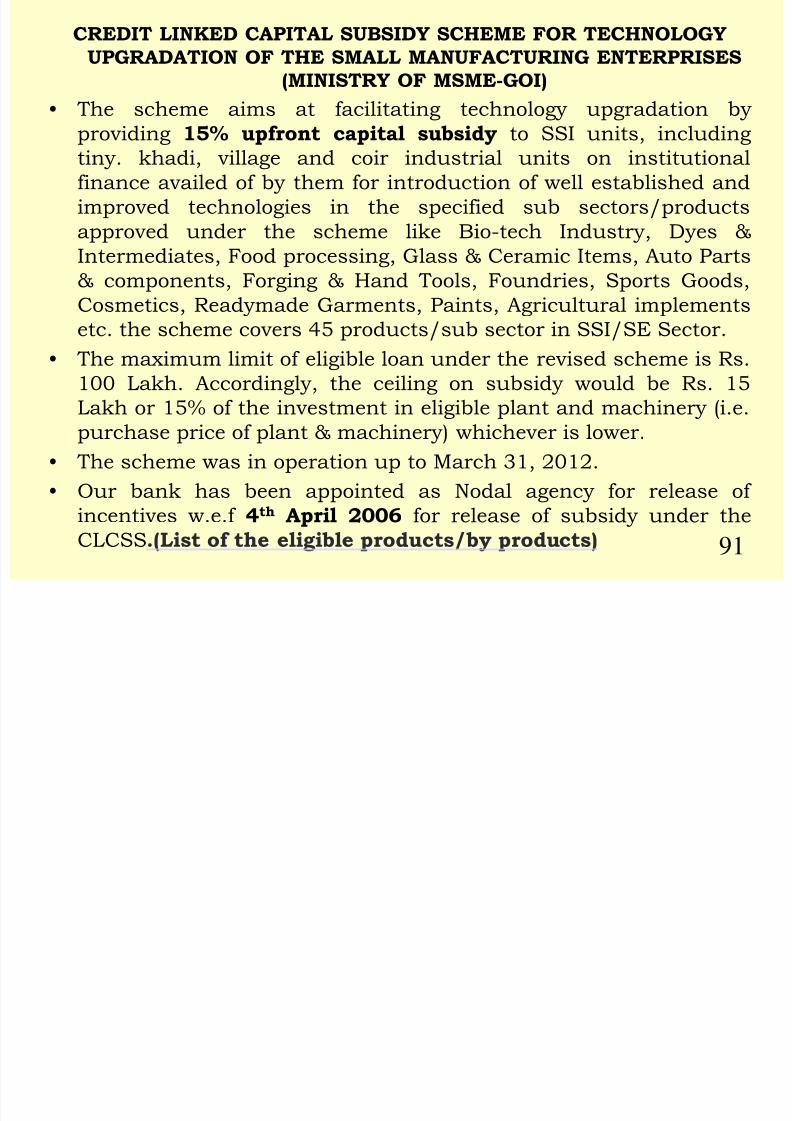

CREDIT LINKED CAPITAL SUBSIDY SCHEME FOR TECHNOLOGY

UPGRADATION OF THE SMALL MANUFACTURING ENTERPRISES

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 91/102

(MINISTRY OF MSME-GOI)

• The scheme aims at facilitating technology upgradation by

providing 15% upfront capital subsidy to SSI units, including

tiny. khadi, village and coir industrial units on institutionalfinance availed of by them for introduction of well established and

improved technologies in the specified sub sectors/products

approved under the scheme like Bio-tech Industry, Dyes &

Intermediates, Food processing, Glass & Ceramic Items, Auto Parts

& components, Forging & Hand Tools, Foundries, Sports Goods,Cosmetics, Readymade Garments, Paints, Agricultural implements

etc. the scheme covers 45 products/sub sector in SSI/SE Sector.

• The maximum limit of eligible loan under the revised scheme is Rs.

100 Lakh. Accordingly, the ceiling on subsidy would be Rs. 15

Lakh or 15% of the investment in eligible plant and machinery (i.e.

purchase price of plant & machinery) whichever is lower.

• The scheme was in operation up to March 31, 2012.

• Our bank has been appointed as Nodal agency for release of

incentives w.e.f 4th April 2006 for release of subsidy under the

CLCSS.(List of the eligible products/by products)

91

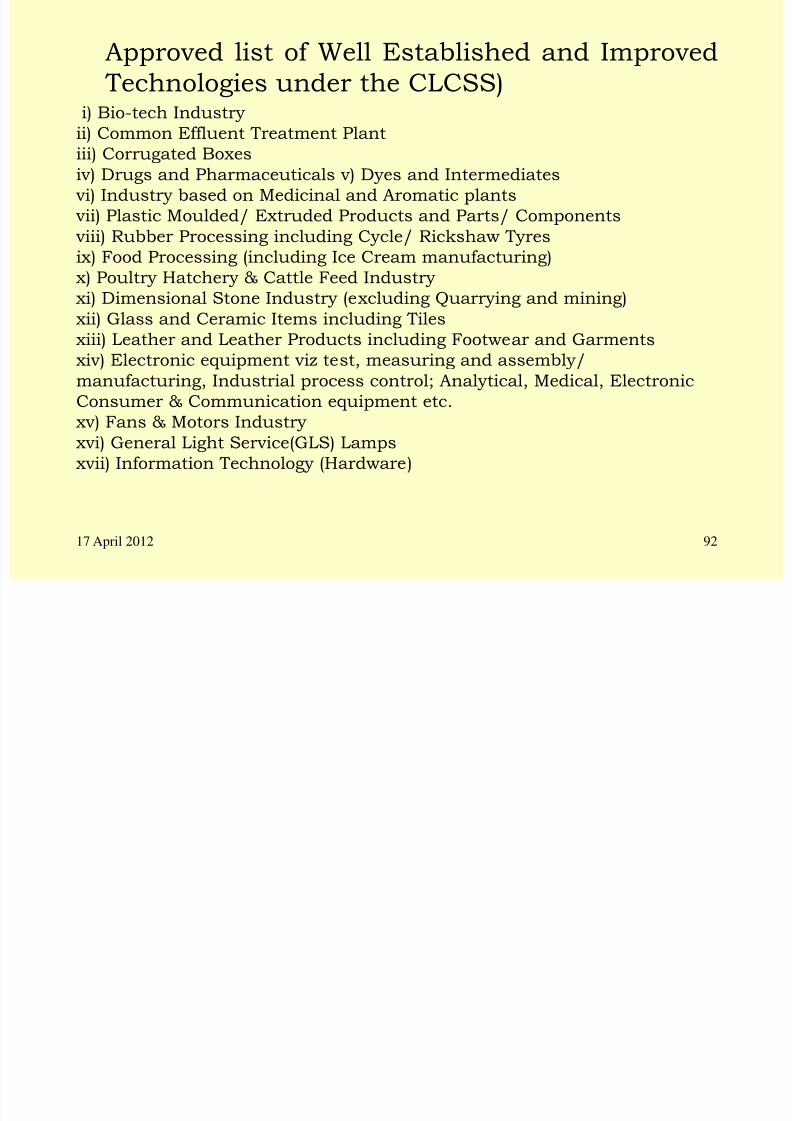

Approved list of Well Established and Improved

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 92/102

pp p

Technologies under the CLCSS)i) Bio-tech Industry

ii) Common Effluent Treatment Plant

iii) Corrugated Boxesiv) Drugs and Pharmaceuticals v) Dyes and Intermediates

vi) Industry based on Medicinal and Aromatic plants

vii) Plastic Moulded/ Extruded Products and Parts/ Components

viii) Rubber Processing including Cycle/ Rickshaw Tyres

ix) Food Processing (including Ice Cream manufacturing)

x) Poultry Hatchery & Cattle Feed Industry xi) Dimensional Stone Industry (excluding Quarrying and mining)

xii) Glass and Ceramic Items including Tiles

xiii) Leather and Leather Products including Footwear and Garments

xiv) Electronic equipment viz test, measuring and assembly/

manufacturing, Industrial process control; Analytical, Medical, Electronic

Consumer & Communication equipment etc.

xv) Fans & Motors Industry xvi) General Light Service(GLS) Lamps

xvii) Information Technology (Hardware)

17 April 2012 92

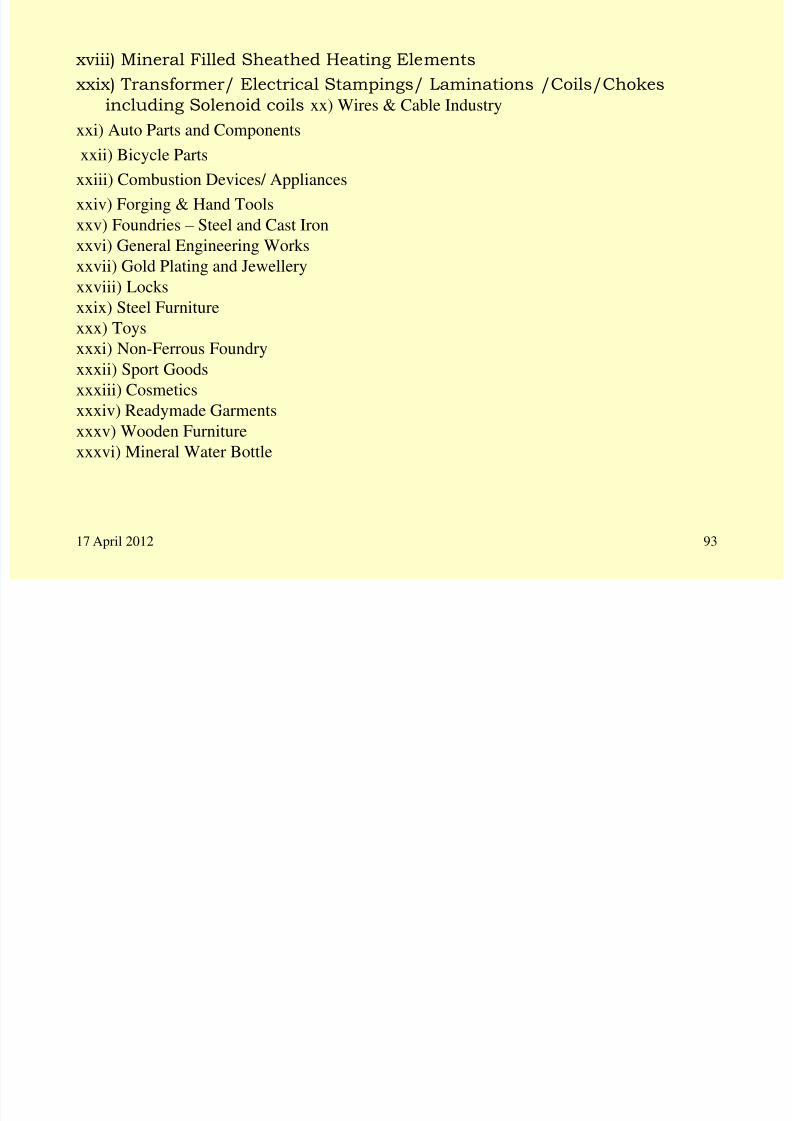

xviii) Mineral Filled Sheathed Heating Elements

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 93/102

) g

xxix) Transformer/ Electrical Stampings/ Laminations /Coils/Chokes

including Solenoid coils xx) Wires & Cable Industry

xxi) Auto Parts and Components

xxii) Bicycle Parts

xxiii) Combustion Devices/ Appliances

xxiv) Forging & Hand Tools

xxv) Foundries – Steel and Cast Iron

xxvi) General Engineering Works

xxvii) Gold Plating and Jewellery

xxviii) Locksxxix) Steel Furniture

xxx) Toys

xxxi) Non-Ferrous Foundry

xxxii) Sport Goods

xxxiii) Cosmetics

xxxiv) Readymade Garments

xxxv) Wooden Furniture

xxxvi) Mineral Water Bottle

17 April 2012 93

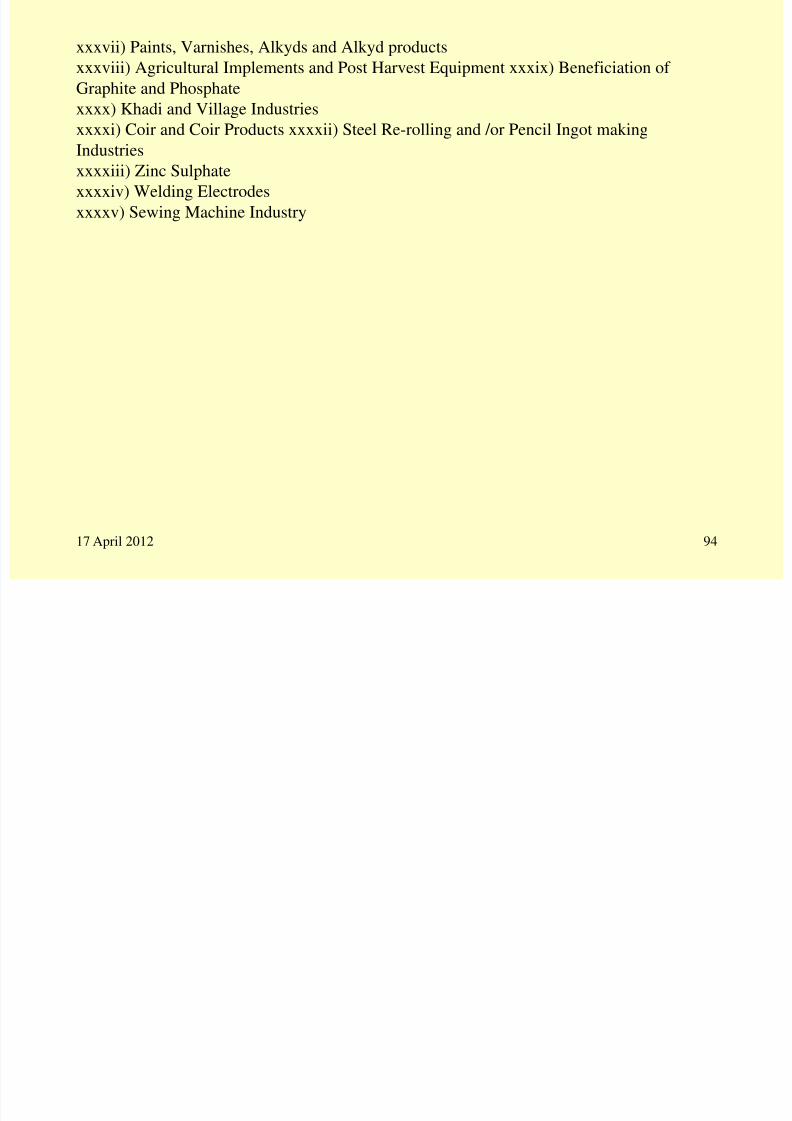

xxxvii) Paints, Varnishes, Alkyds and Alkyd products

xxxviii) Agricultural Implements and Post Harvest Equipment xxxix) Beneficiation of

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 94/102

xxxviii) Agricultural Implements and Post Harvest Equipment xxxix) Beneficiation of

Graphite and Phosphate

xxxx) Khadi and Village Industries

xxxxi) Coir and Coir Products xxxxii) Steel Re-rolling and /or Pencil Ingot making

Industriesxxxxiii) Zinc Sulphate

xxxxiv) Welding Electrodes

xxxxv) Sewing Machine Industry

17 April 2012 94

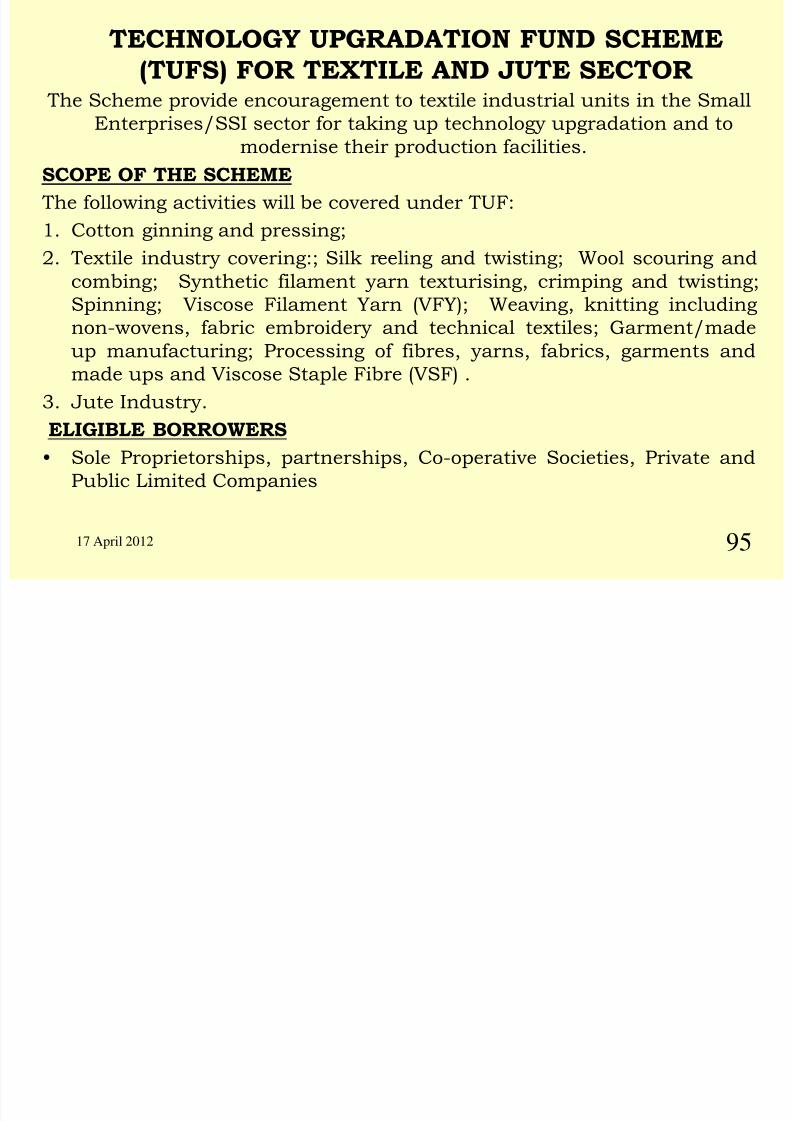

TECHNOLOGY UPGRADATION FUND SCHEME

(TUFS) FOR TEXTILE AND JUTE SECTOR

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 95/102

(TUFS) FOR TEXTILE AND JUTE SECTOR The Scheme provide encouragement to textile industrial units in the Small

Enterprises/SSI sector for taking up technology upgradation and to

modernise their production facilities. SCOPE OF THE SCHEME

The following activities will be covered under TUF:

1. Cotton ginning and pressing;

2. Textile industry covering:; Silk reeling and twisting; Wool scouring and

combing; Synthetic filament yarn texturising, crimping and twisting;Spinning; Viscose Filament Yarn (VFY); Weaving, knitting including

non-wovens, fabric embroidery and technical textiles; Garment/made

up manufacturing; Processing of fibres, yarns, fabrics, garments and

made ups and Viscose Staple Fibre (VSF) .

3. Jute Industry.

ELIGIBLE BORROWERS

• Sole Proprietorships, partnerships, Co-operative Societies, Private and

Public Limited Companies

9517 April 2012

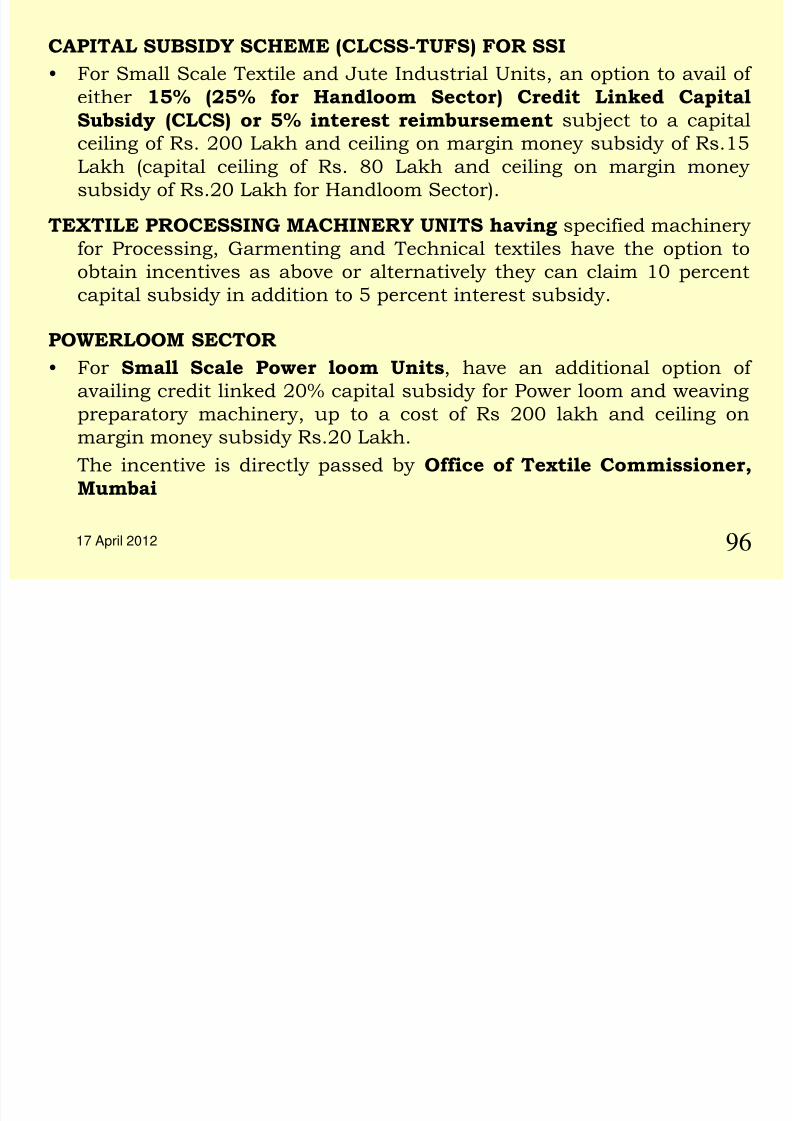

CAPITAL SUBSIDY SCHEME (CLCSS-TUFS) FOR SSI

F S ll S l T til d J t I d t i l U it ti t il f

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 96/102

• For Small Scale Textile and Jute Industrial Units, an option to avail of

either 15% (25% for Handloom Sector) Credit Linked Capital

Subsidy (CLCS) or 5% interest reimbursement subject to a capital

ceiling of Rs. 200 Lakh and ceiling on margin money subsidy of Rs.15Lakh (capital ceiling of Rs. 80 Lakh and ceiling on margin money

subsidy of Rs.20 Lakh for Handloom Sector).

TEXTILE PROCESSING MACHINERY UNITS having specified machinery

for Processing, Garmenting and Technical textiles have the option to

obtain incentives as above or alternatively they can claim 10 percent

capital subsidy in addition to 5 percent interest subsidy.

POWERLOOM SECTOR

• For Small Scale Power loom Units, have an additional option of

availing credit linked 20% capital subsidy for Power loom and weaving

preparatory machinery, up to a cost of Rs 200 lakh and ceiling onmargin money subsidy Rs.20 Lakh.

The incentive is directly passed by Office of Textile Commissioner,

Mumbai

17 April 2012 96

cont…..

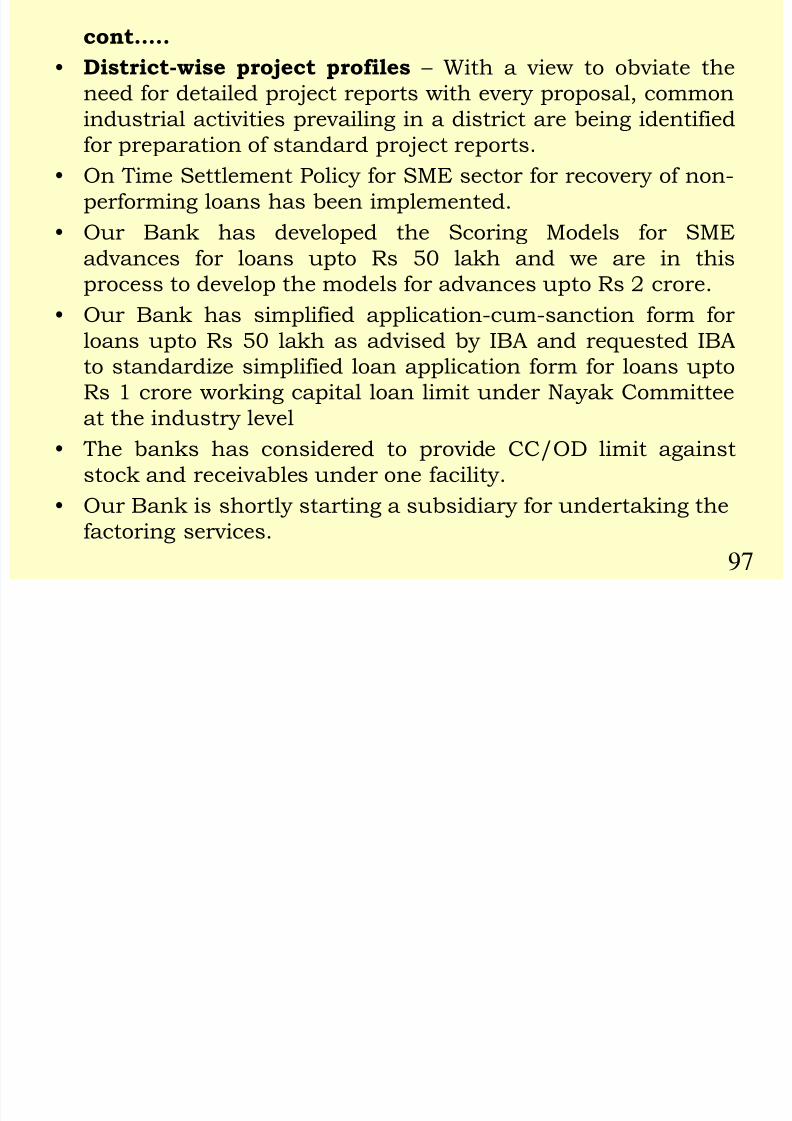

• District-wise project profiles – With a view to obviate the

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 97/102

• District-wise project profiles – With a view to obviate the

need for detailed project reports with every proposal, common

industrial activities prevailing in a district are being identified

for preparation of standard project reports.• On Time Settlement Policy for SME sector for recovery of non-

performing loans has been implemented.

• Our Bank has developed the Scoring Models for SME

advances for loans upto Rs 50 lakh and we are in this

process to develop the models for advances upto Rs 2 crore.• Our Bank has simplified application-cum-sanction form for

loans upto Rs 50 lakh as advised by IBA and requested IBA

to standardize simplified loan application form for loans upto

Rs 1 crore working capital loan limit under Nayak Committee

at the industry level• The banks has considered to provide CC/OD limit against

stock and receivables under one facility.

• Our Bank is shortly starting a subsidiary for undertaking the

factoring services.

97

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 98/102

Thanks……………

17 April 2012 98

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 99/102

OTHER SME

SCHEMES

17 April 2012 99

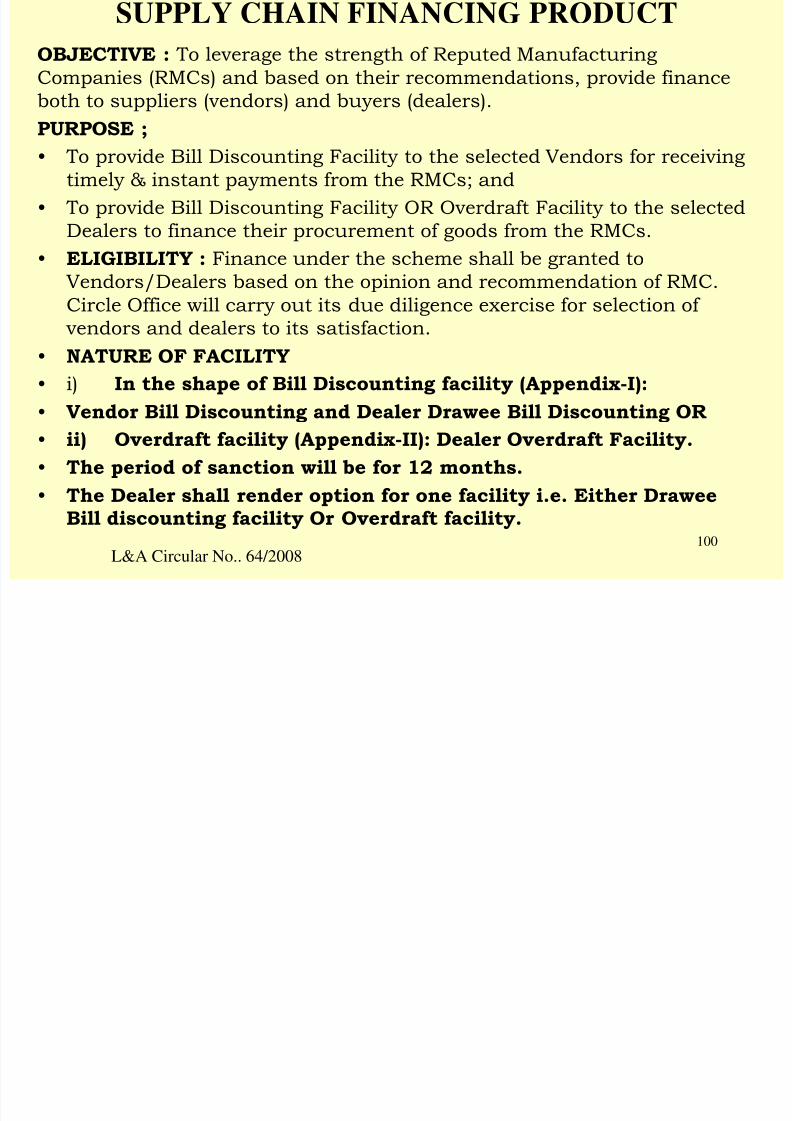

SUPPLY CHAIN FINANCING PRODUCT OBJECTIVE : To leverage the strength of Reputed Manufacturing

C i (RMC ) d b d h i d i id fi

8/4/2019 8-SME 30092009

http://slidepdf.com/reader/full/8-sme-30092009 100/102

Companies (RMCs) and based on their recommendations, provide finance

both to suppliers (vendors) and buyers (dealers).

PURPOSE ;

• To provide Bill Discounting Facility to the selected Vendors for receivingtimely & instant payments from the RMCs; and

• To provide Bill Discounting Facility OR Overdraft Facility to the selected