RPBA - Madeira Free Zone - 29.10.2014

63

-

Upload

ricardo-da-palma-borges-associados-sociedade-de-advogados-sp-rl -

Category

Law

-

view

484 -

download

2

Transcript of RPBA - Madeira Free Zone - 29.10.2014

Overview

• Introduction

• The Critical Issues

• Taxation of MFZ Companies

• Madeira’s Practical Structures

2

Introduction

• Main Taxes

• Business Climate in Madeira

• Value Added Tax

• Personal Income Tax

• Corporate Income Tax

3

How to spell Madeira (frequent client answers)

• Madiera - NO

• Maderia - NO

• Madieria - NO

• Maidera - NO

• Maideira - NO

• Maideria - NO

• Madeira - YES

4

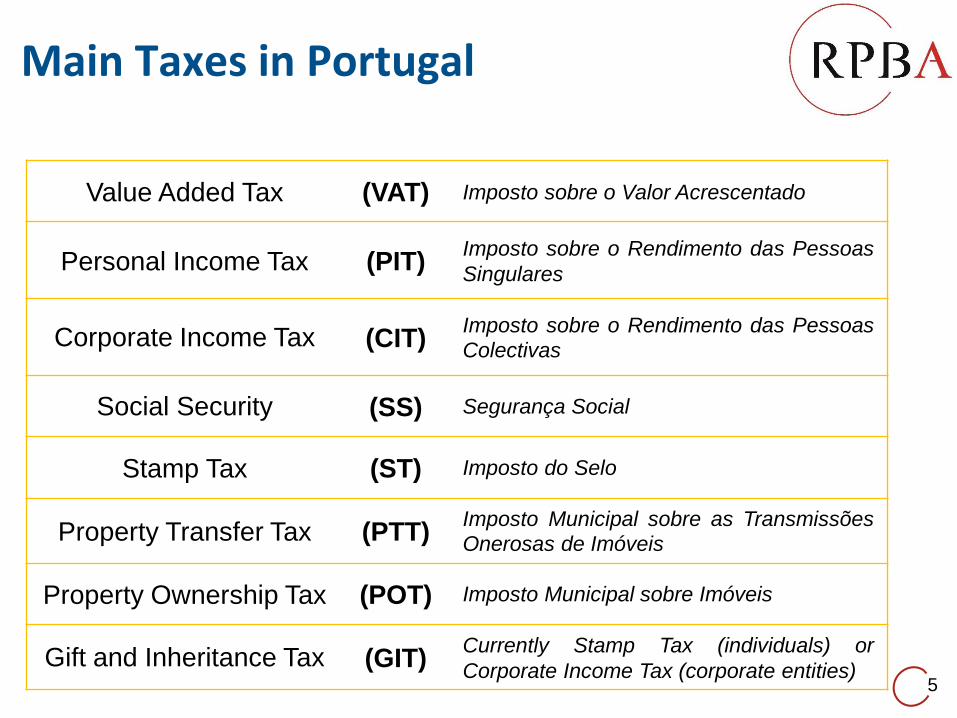

Main Taxes in Portugal

5

Value Added Tax (VAT) Imposto sobre o Valor Acrescentado

Personal Income Tax (PIT)Imposto sobre o Rendimento das Pessoas

Singulares

Corporate Income Tax (CIT)Imposto sobre o Rendimento das Pessoas

Colectivas

Social Security (SS) Segurança Social

Stamp Tax (ST) Imposto do Selo

Property Transfer Tax (PTT)Imposto Municipal sobre as Transmissões

Onerosas de Imóveis

Property Ownership Tax (POT) Imposto Municipal sobre Imóveis

Gift and Inheritance Tax (GIT)Currently Stamp Tax (individuals) or

Corporate Income Tax (corporate entities)

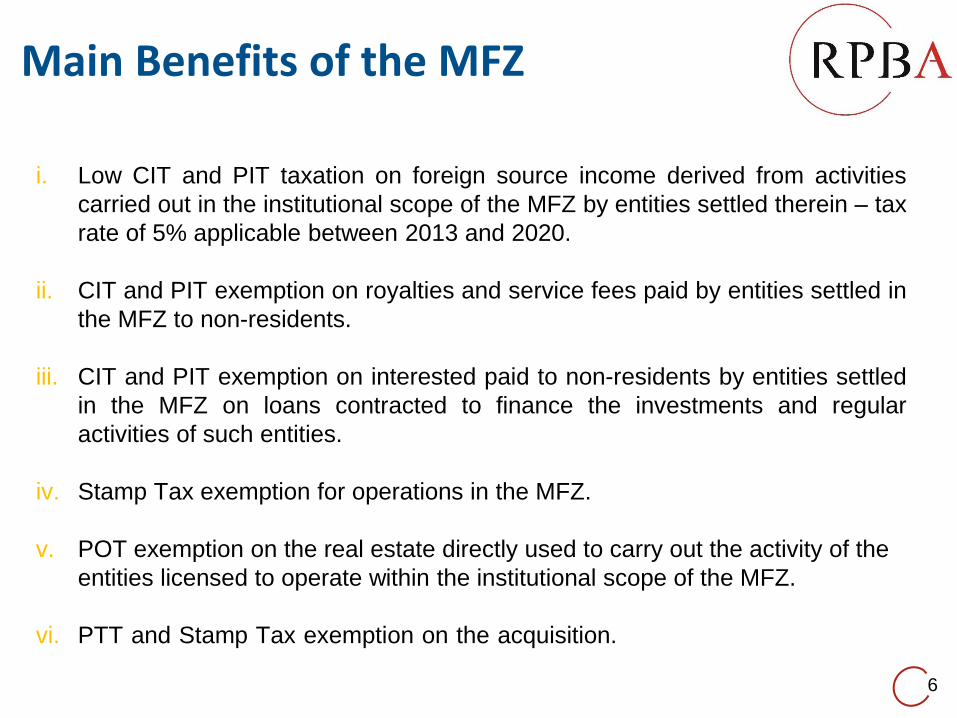

Main Benefits of the MFZ

i. Low CIT and PIT taxation on foreign source income derived from activities

carried out in the institutional scope of the MFZ by entities settled therein – tax

rate of 5% applicable between 2013 and 2020.

ii. CIT and PIT exemption on royalties and service fees paid by entities settled in

the MFZ to non-residents.

iii. CIT and PIT exemption on interested paid to non-residents by entities settled

in the MFZ on loans contracted to finance the investments and regular

activities of such entities.

iv. Stamp Tax exemption for operations in the MFZ.

v. POT exemption on the real estate directly used to carry out the activity of the

entities licensed to operate within the institutional scope of the MFZ.

vi. PTT and Stamp Tax exemption on the acquisition. real estate for their setting

up by entities in the MFZ and of participations in those entities6

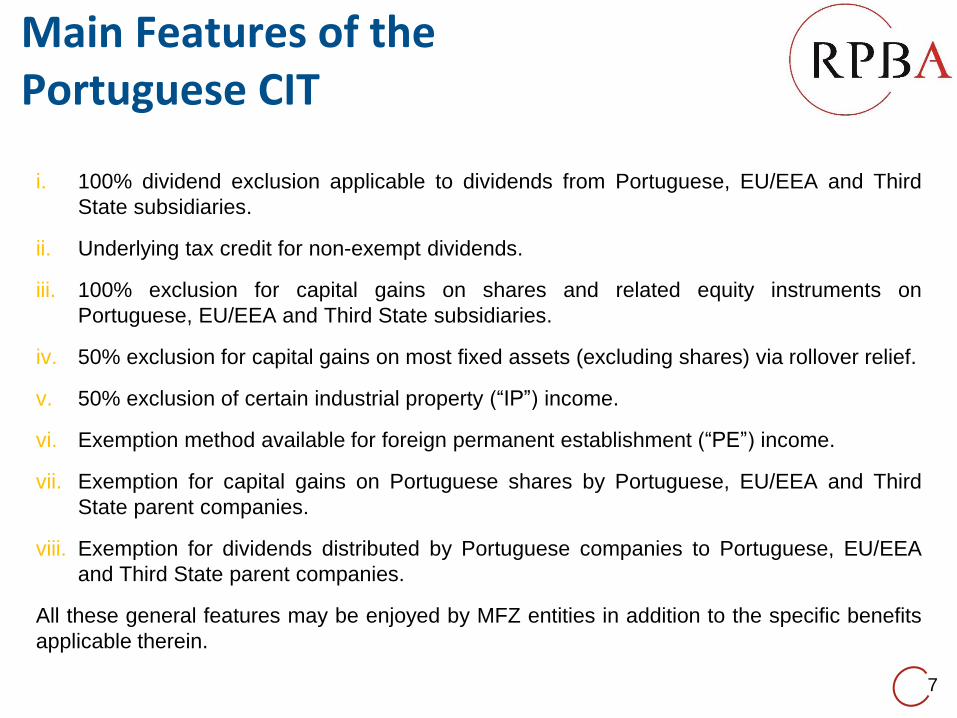

Main Features of the Portuguese CIT

i. 100% dividend exclusion applicable to dividends from Portuguese, EU/EEA and Third

State subsidiaries.

ii. Underlying tax credit for non-exempt dividends.

iii. 100% exclusion for capital gains on shares and related equity instruments on

Portuguese, EU/EEA and Third State subsidiaries.

iv. 50% exclusion for capital gains on most fixed assets (excluding shares) via rollover relief.

v. 50% exclusion of certain industrial property (“IP”) income.

vi. Exemption method available for foreign permanent establishment (“PE”) income.

vii. Exemption for capital gains on Portuguese shares by Portuguese, EU/EEA and Third

State parent companies.

viii. Exemption for dividends distributed by Portuguese companies to Portuguese, EU/EEA

and Third State parent companies.

All these general features may be enjoyed by MFZ entities in addition to the specific benefits

applicable therein.

7

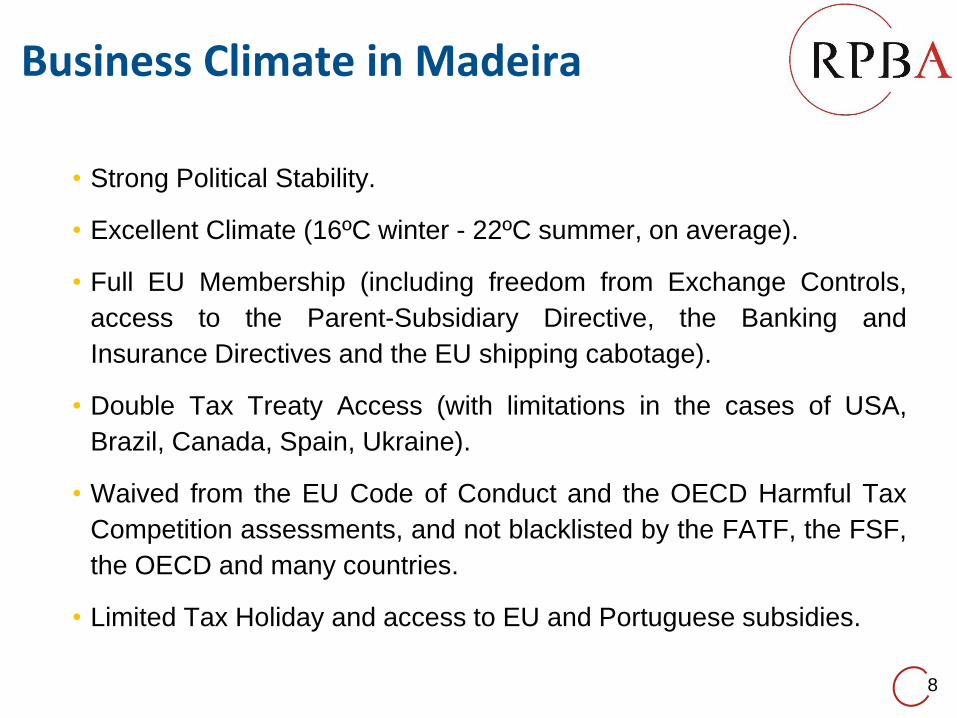

Business Climate in Madeira

• Strong Political Stability.

• Excellent Climate (16ºC winter - 22ºC summer, on average).

• Full EU Membership (including freedom from Exchange Controls,

access to the Parent-Subsidiary Directive, the Banking and

Insurance Directives and the EU shipping cabotage).

• Double Tax Treaty Access (with limitations in the cases of USA,

Brazil, Canada, Spain, Ukraine).

• Waived from the EU Code of Conduct and the OECD Harmful Tax

Competition assessments, and not blacklisted by the FATF, the FSF,

the OECD and many countries.

• Limited Tax Holiday and access to EU and Portuguese subsidies.

8

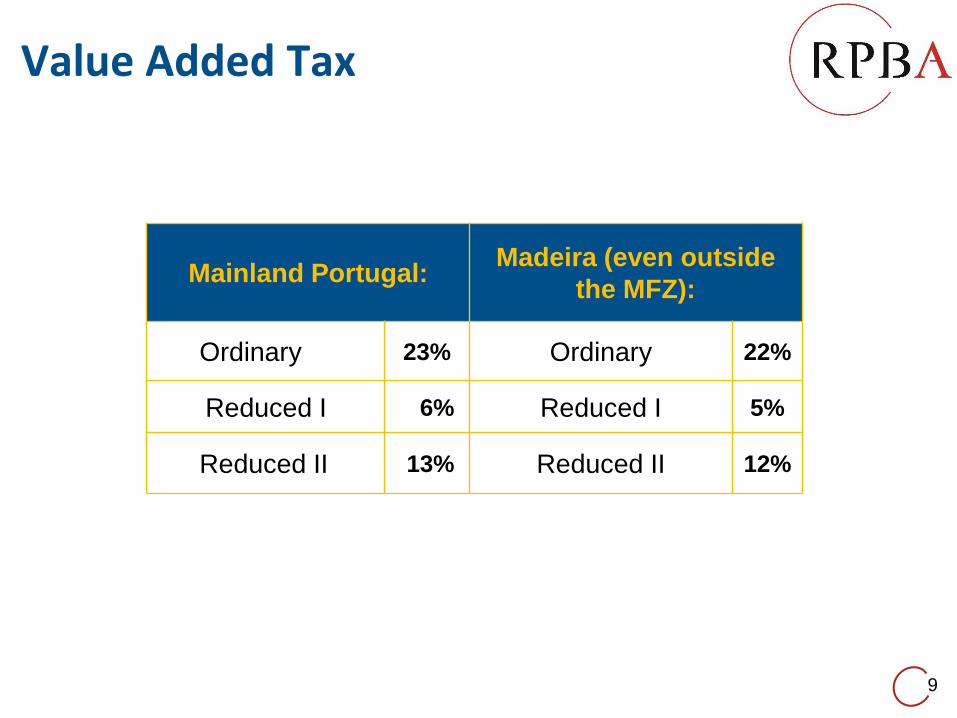

Value Added Tax

9

Mainland Portugal:Madeira (even outside

the MFZ):

Ordinary 23% Ordinary 22%

Reduced I 6% Reduced I 5%

Reduced II 13% Reduced II 12%

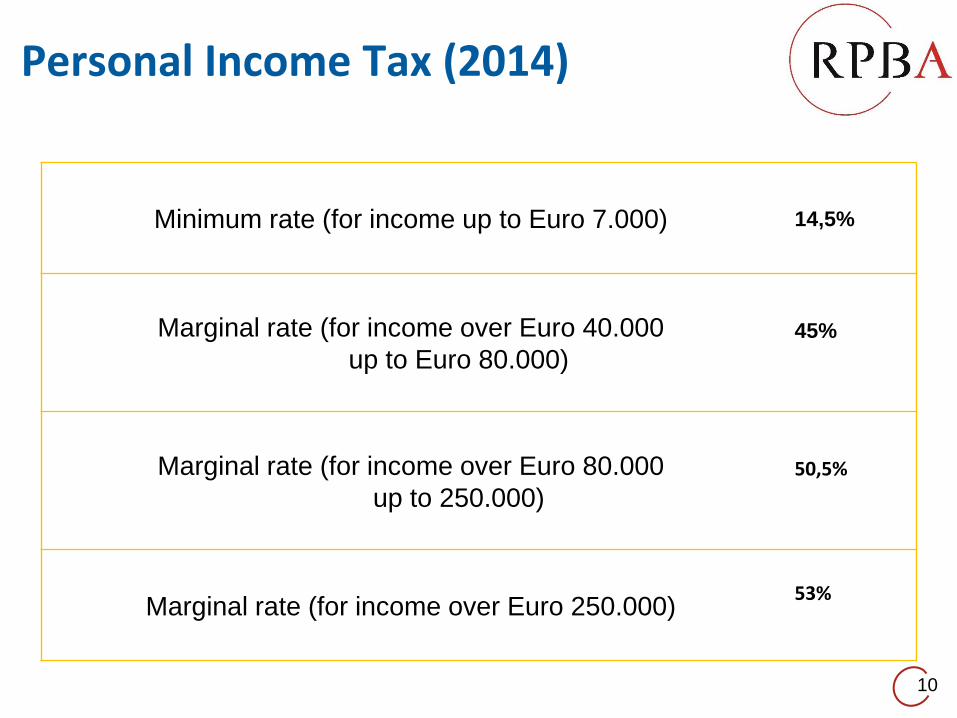

Personal Income Tax (2014)

10

Minimum rate (for income up to Euro 7.000) 14,5%

Marginal rate (for income over Euro 40.000

up to Euro 80.000)45%

Marginal rate (for income over Euro 80.000

up to 250.000)

50,5%

Marginal rate (for income over Euro 250.000)53%

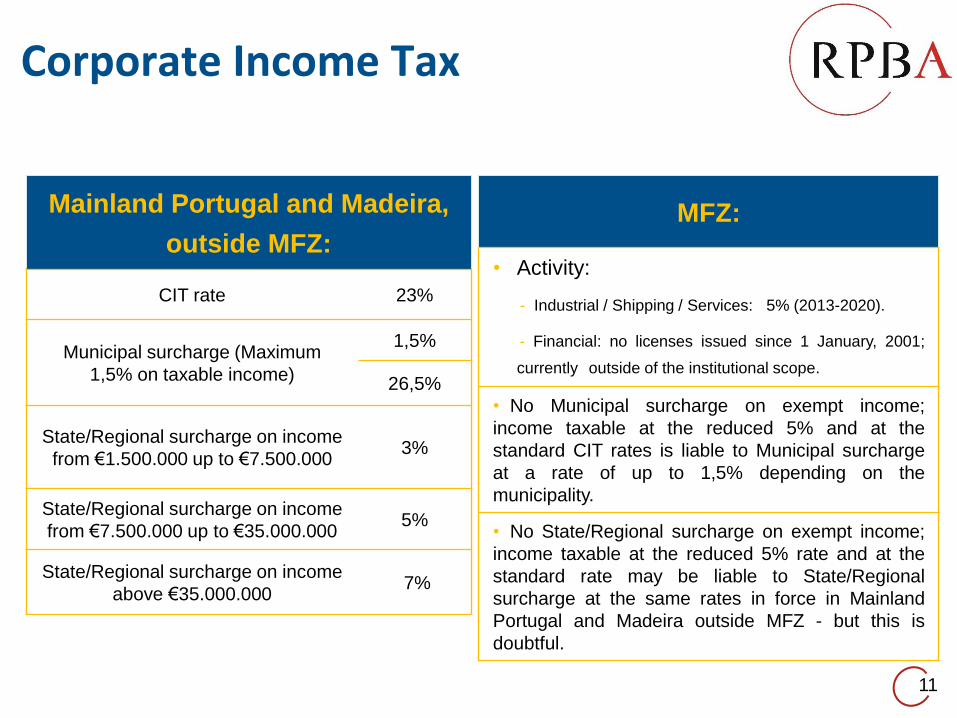

Corporate Income Tax

11

Mainland Portugal and Madeira,

outside MFZ:

CIT rate 23%

Municipal surcharge (Maximum

1,5% on taxable income)

1,5%

26,5%

State/Regional surcharge on income

from €1.500.000 up to €7.500.0003%

State/Regional surcharge on income

from €7.500.000 up to €35.000.000 5%

State/Regional surcharge on income

above €35.000.000 7%

MFZ:

• Activity:

- Industrial / Shipping / Services: 5% (2013-2020).

- Financial: no licenses issued since 1 January, 2001;

currently outside of the institutional scope.

• No Municipal surcharge on exempt income;

income taxable at the reduced 5% and at the

standard CIT rates is liable to Municipal surcharge

at a rate of up to 1,5% depending on the

municipality.

• No State/Regional surcharge on exempt income;

income taxable at the reduced 5% rate and at the

standard rate may be liable to State/Regional

surcharge at the same rates in force in Mainland

Portugal and Madeira outside MFZ - but this is

doubtful.

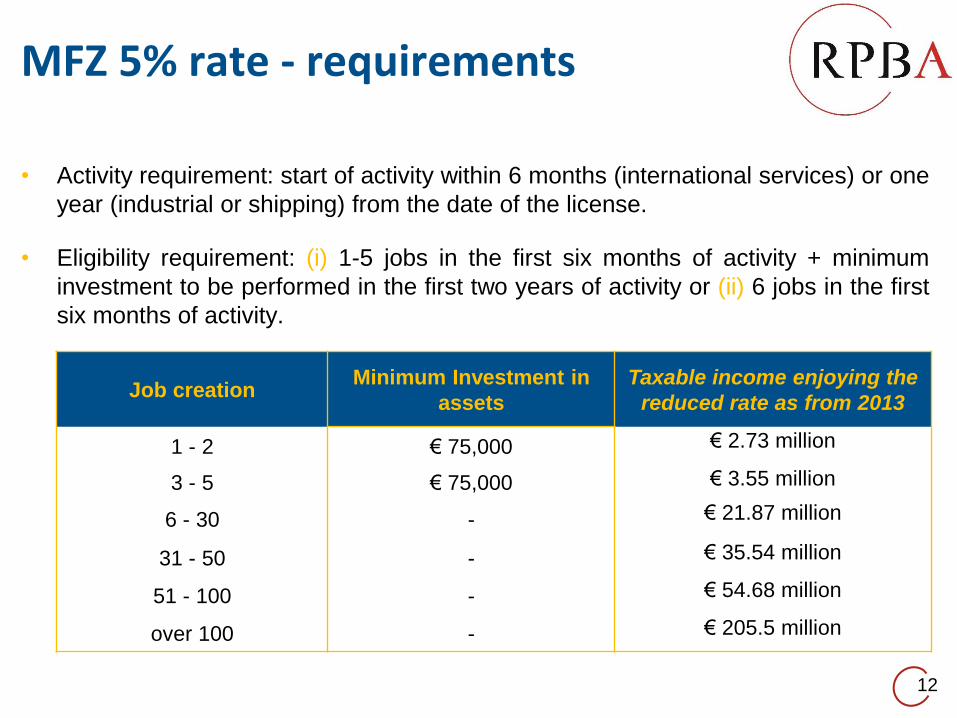

MFZ 5% rate - requirements

• Activity requirement: start of activity within 6 months (international services) or one

year (industrial or shipping) from the date of the license.

• Eligibility requirement: (i) 1-5 jobs in the first six months of activity + minimum

investment to be performed in the first two years of activity or (ii) 6 jobs in the first

six months of activity.

12

Job creationMinimum Investment in

assets

Taxable income enjoying the

reduced rate as from 2013

1 - 2 € 75,000 € 2.73 million

3 - 5 € 75,000 € 3.55 million

6 - 30 - € 21.87 million

31 - 50 - € 35.54 million

51 - 100 - € 54.68 million

over 100 - € 205.5 million

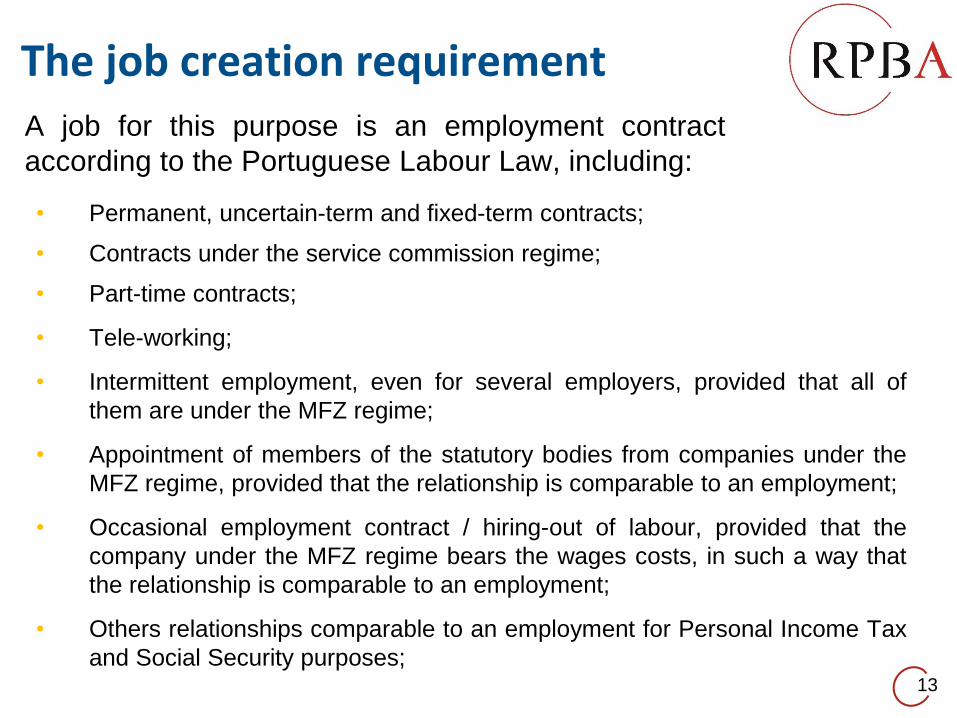

The job creation requirement

• Permanent, uncertain-term and fixed-term contracts;

• Contracts under the service commission regime;

• Part-time contracts;

• Tele-working;

• Intermittent employment, even for several employers, provided that all of

them are under the MFZ regime;

• Appointment of members of the statutory bodies from companies under the

MFZ regime, provided that the relationship is comparable to an employment;

• Occasional employment contract / hiring-out of labour, provided that the

company under the MFZ regime bears the wages costs, in such a way that

the relationship is comparable to an employment;

• Others relationships comparable to an employment for Personal Income Tax

and Social Security purposes;13

A job for this purpose is an employment contract

according to the Portuguese Labour Law, including:

The € 75,000 minimum investment requirement

• Applicable only in the case of creation of less than 6 jobs in the

first six months of activity.

• In the acquisition of fixed assets, whether tangible or intangible

(according to an Opinion of the Regional Director of Finance in

Madeira, as per the Portuguese Accounting Normalization System

(SNC), all assets included in the class “Investments”, including

financial investments, qualify as fixed assets, but we prefer a

narrower and safer criterion, excluding the latter).

• To be performed in the first two years of activity.

• Assets do not have to be located in Madeira.

14

General CIT rates

15

• The general CIT rate of 23% is applicable to:

- income derived from Portuguese source (except MFZ); or

- income above the referred limits of taxable income enjoying the reduced

rate.

• A reduced rate of 17% is applicable to entities legally

certified as SMEs, up to € 15.000.

The critical issues• International developments on tax harmonization.

• Substance and effective management requirements for licensed entities.

• Scope of activities of Pure and other Holdings.

• Scope of activities of service companies (non-credit and non-financial).

• Special tax on undocumented / entertainment and motor / tax haven expenses.

• Special payment on account (PEC) of CIT.

• State / Regional surcharge.

• Transfer pricing regulations.

• Restriction on the deductibility of financing costs.

• Due diligence matters.16

• MFZ has been waived from the EU Code of Conduct analysis (which enables the

enforcement of the Netherlands Double Tax Treaty, for instance).

• MFZ has been waived from OECD harmful tax competition analysis.

• The MFZ regime has changed substantially starting from January 1, 2012, but not due to

IMF/ECB/European Commission scrutiny.

• The European Commission, by decision of 2 July 2013, has approved the amendment of

the State Aid regime currently in force (N 421/2006, as approved by Commission

decision of 27 June 2007), allowing for an increase of the taxable income eligible for the

reduced CIT rate.

• The European Commission, by decision of 8 May 2014, has authorized the extension of

the regime for entries taking place until 31 December 2014 (previously new entries into

the regime were barred from 30 June 2014 onwards). This extension has been

transposed into Portuguese domestic law on September 30 and between 1 July 2014

and the latter date new entries into the regime were nevertheless accepted by the entity

managing the Free Zone and by Tax Authorities in Madeira.

• A new State Aid regime (regime IV), applicable to entities registered after 1 January

2015, is already being negotiated with the European Commission.

17

International developments on tax harmonization

• E-business (Internet service and content providers), telecommunications

and holding of participations are mobile activities that may be easily tax

driven to the MFZ but loosing tax revenue countries will try to challenge

these migrations.

• The 2007-2020 EU State Aid regimes for MFZ companies and their

realistic and sensible interpretation by the Regional Administration.

• The branch and the trust as relatively unexplored alternatives to

substance and effective management requirements.

18

Substance and effective management requirements for licensed entities

• A popular myth: holding companies not incorporated as Sociedades

Gestoras de Participações Sociais (SGPS) must be mixed (holding and

operating) companies.

• The legal permission of own portfolio management for commercial

companies vs. the prohibition of exclusive holding activity by non-SGPS

companies.

• Contradiction between social object and factual object is not the same

as double social object / partial exercise of a double social object.

• The mixed, impure and atypical holding companies.

19

Scope of activities of Pure and Other Holdings

• Credit Institutions and the receiving of deposits for their own account,

towards the Public.

• Credit Institutions and Financial Companies and the professional

exercise of listed activities.

• Non-Public (bonds, commercial paper, shareholders loans, labour loans,

payments in advance or outstanding, treasury operations within group

companies, vouchers or cards). The case of the specific and isolated

party to a contract outside the group. The legal permission of own

portfolio management. The Sociedades Gestoras de Património.

• Cash pooling and passive investment. The Sociedades de Simples

Administração de Bens.

20

Scope of activities of service companies (non-credit and non-financial)

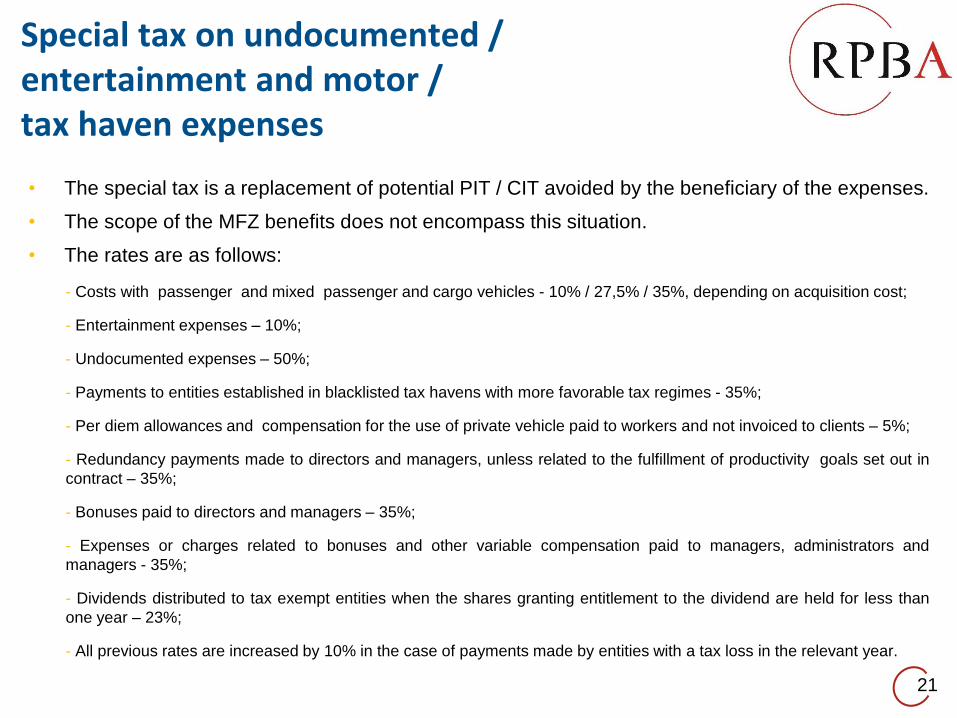

• The special tax is a replacement of potential PIT / CIT avoided by the beneficiary of the expenses.

• The scope of the MFZ benefits does not encompass this situation.

• The rates are as follows:

- Costs with passenger and mixed passenger and cargo vehicles - 10% / 27,5% / 35%, depending on acquisition cost;

- Entertainment expenses – 10%;

- Undocumented expenses – 50%;

- Payments to entities established in blacklisted tax havens with more favorable tax regimes - 35%;

- Per diem allowances and compensation for the use of private vehicle paid to workers and not invoiced to clients – 5%;

- Redundancy payments made to directors and managers, unless related to the fulfillment of productivity goals set out in

contract – 35%;

- Bonuses paid to directors and managers – 35%;

- Expenses or charges related to bonuses and other variable compensation paid to managers, administrators and

managers - 35%;

- Dividends distributed to tax exempt entities when the shares granting entitlement to the dividend are held for less than

one year – 23%;

- All previous rates are increased by 10% in the case of payments made by entities with a tax loss in the relevant year.

21

Special tax on undocumented /entertainment and motor /tax haven expenses

• Under the black letter of the law, entities established in the MFZ were liable to

the PEC even when the tax exemption regime was in force, although it was

never charged to them.

• In 2004 a rule was enacted expressly exempting certain kinds of entities from

the PEC, namely fully CIT exempt entities such as the State, municipalities, etc.

This rule did not include a reference to taxable entities with exempt income, as

was the case of entities established in the MFZ.

• Tax Authorities started assessing the PEC to MFZ entities under the exemption

regime in that year.

• Several court decisions ruled against the assessment, based on the ability to

pay principle (entities with only exempt income had no duty to pay on account of

undue tax).

• Starting from 2006, a new rule was enacted, providing for a PEC limited to

€1.250 (€ 1.000 since 2009) for entities only deriving tax exempt income.

22

Special payment on account (PEC) of CIT

• That rule was declared unconstitutional by a decision of the Constitutional Court

in 2009, also based on the ability to pay principle.

• In 2010 a new rule was enacted, providing for an exemption of PEC for entities

with only exempt income.

• From then on the limitation to €1.000 was abolished and MFZ entities became

liable to PEC according to the general rules, provided that they:

- had non-exempt income (such as Portuguese non-MFZ source income) and were under the

previous exemption regime; or

- were already under the rate reduction regimes.

• The MFZ exemption regime ended in December 31, 2011, which means that all

MFZ entities are now liable to PEC according to the general rules, ranging

between €1.000 and €70.000, levied at the rate of 1% on the previous year

turnover.

• The Tax Authorities have already issued a ruling stating that the effect of the

reduced CIT rates in force in the MFZ is not to be taken into account when

computing this prepayment.

23

Special payment on account of CIT

• The CIT Code currently establishes a surcharge of 3% on income from

€1.500.000 up to €7.500.000, of 5% on income from €7.500.000 up to

€35.000.000 and of 7% on income above €35.000.000.

• This surcharge was enacted in 2010 (with different brackets and rates).

• However, the surcharge was “transposed” into Madeira legislation by a

Regional Legislative Decree, issued by the Parliament of the

Autonomous Region of Madeira, under its powers to legislate in tax

matters.

• Such transposition was apparently devoid of any effects, as:

a) The surcharge established in the CIT Code is applicable to the entire

Portuguese territory, regardless of such “transposition”.

b) The Regional Legislative Decree created a regime which was an exact

copy of the surcharge established in the CIT Code and which has been

updated to remain exactly similar to it whenever changes to the CIT Code

are made. 24

State / Regional surcharge

• There is, however, one significant difference between both regimes.

• In 2011 a rule was enacted by the Parliament of the Autonomous Region of Madeira exempting entities

established in the MFZ from the surcharge, whether they were under the exemption or the reduced rate

regimes (this rule was enacted following an administrative order of the Regional Finance Secretary, issued in

2010 and providing for the same surcharge exemption for MFZ entities. This administrative order was however

of infra-legal status).

• This rule was not included in the CIT Code provisions establishing the CIT surcharge.

• However, it is a fact that the revenue raised by the CIT collected from entities established in Madeira, even in

the MFZ, belongs to the Regional Government.

• Could the Regional Parliament legislate to exempt MFZ entities from the surcharge? Is the exemption legal?

• In our view it is doubtful, as the creation of this exemption was not comprised in the list of legislative powers in

tax matters granted to the Regional Parliament by the Regional Finance Law; moreover, this Law expressly

provides that all matters relating to the MFZ regime must be dealt with by a law of the National Parliament (or

of the National Government, acting under an authorization to legislate granted by the Parliament).

• Regional legislation has been amended in a try to clarify the issue in 2014, but doubts still remain.

• Therefore, although the surcharge was generally not assessed (this has happened in only 2 cases, as far as

we are aware) in regard of MFZ entities since 2010, it is not guaranteed that it will not be so in the future, with

retroactive effects.

• The are rumors according to which Tax Authorities may accept that the State/Regional surcharge is only due

on taxable income liable to the standard CIT rates (thus not encompassing income liable to the reduced 5%

rate). No formal ruling has been issued to reflect such position and its validity is therefore also unclear.

25

State / Regional surcharge

• Transfer pricing rules are specifically set in Article 63 of the Corporate

Income Tax Code and on the Ministerial Order (Portaria) no. 1446-C/2001,

of 21 December – the latter is pending revision following the Reform of the

CIT Code.

• The general rule is that taxpayers are deemed associated with a direct or

indirect participation of 20%.

• Profitability of companies vs. MFZ exemptions.

• Companies whose turnover in the previous year has not exceeded

€ 3.000.000 are waived from documentation compliance requirements.

• Although is not likely that the Portuguese Tax Authorities will focus their

efforts and audits on CIT low-taxed MFZ companies, the fact is that some

have been inspected due to their high turnover.26

Transfer pricing regulations

• New rules were introduced by the Law approving the Reform of the CIT Code in this regard

• Financing costs are now only deductible up to:

(i) € 1.000.000 (previously €3.000.000); or

(ii) A percentage of earnings before net financial costs, depreciation and taxes - EBITDA

(70% for 2014, decreasing 10% each year until reaching 30% in 2018);

whichever is higher

• Amounts exceeding these limits may be carried forward and deducted in the subsequent 5

years, provided that the deduction relating to those years is below them. Amounts not used

under the percentage of EBITDA limit (but not under the €1.000.000 limit) may also be

carried forward for the same period and used to absorb excesses verified in regard of it in

subsequent years.

• The regime applies to permanent establishments of non-resident entities.

• The regime applies proportionally in the case of taxable periods shorter than one year (such

as on the starting-up or winding-down of business).

• Tax groups may opt to apply the regime on a consolidated basis for a minimum period of 3

years, subject to certain restrictions, although the option does not increase any of the

above limits (previously the option was not available and the regime applied on an

individual basis even to the members of a tax group). 27

Restriction on the deductibility of financing costs

• Are you getting consulting services invoices from mainland Portugal at the 23%

VAT rate?

– You shouldn’t. VAT should be self-assed under the reverse charge mechanism and

the correct rate is 22%. See Articles 2 (1) (e) and (g), and (5), and 6 (6) (a) of the

VAT Code and Article 1 (2) and (3) of Decree-Law no. 347/85, of 23 August.

• Are you notifying Portuguese Foreign Trade Institute (ICEP) on the

incorporation of MFZ companies / foreign investment operations?

– You no longer need to do it. Decree-Law no. 321/95, of 28 November, was revoked

by Decree-Law no. 203/2003, of 10 September.

• Are you notifying the Bank of Portugal on foreign accounts held by MFZ

companies / branches, of financial operations with non-resident entities and of

assets and liabilities vis-à-vis non-residents?

– You should. See Decree-Law no. 295/2003, of 21 November, Law no. 22/2008, of

13 May, Instructions 34/2009 and 27/2012 of the Bank of Portugal, EC Directive no.

88/361, of 24 July, and EC Regulation no. 184/2005, of 12 January.

28

Due diligence matters (I)

• Are you submitting monthly statistic reports to the Bank of Portugal?

– You should, as this report is mandatory to all entities established in Portugal under

Instruction 27/2012 of the Bank of Portugal. The report should be filed electronically

by the 15th working day following the month to which it refers.

– Entities with less than € 100 000 of economic and financial operations per year with

non-resident entities are exempt from reporting.

• Are you notifying Portuguese Securities and Exchange Commission (CMVM) on

the issuing of shares in Sociedade Anónima companies?

– You shouldn’t, unless the company has a “Sociedade Aberta” status or the company

is listed in a stock exchange. See Article 110 (2), of the Securities Code.

• Are you notifying the Portuguese Tax Administration on the transfer for a

consideration of shares in Sociedade Anónima companies?

– In principle you should. See Articles 138 of the Personal Income Tax Code and 129

of the CIT Code.

29

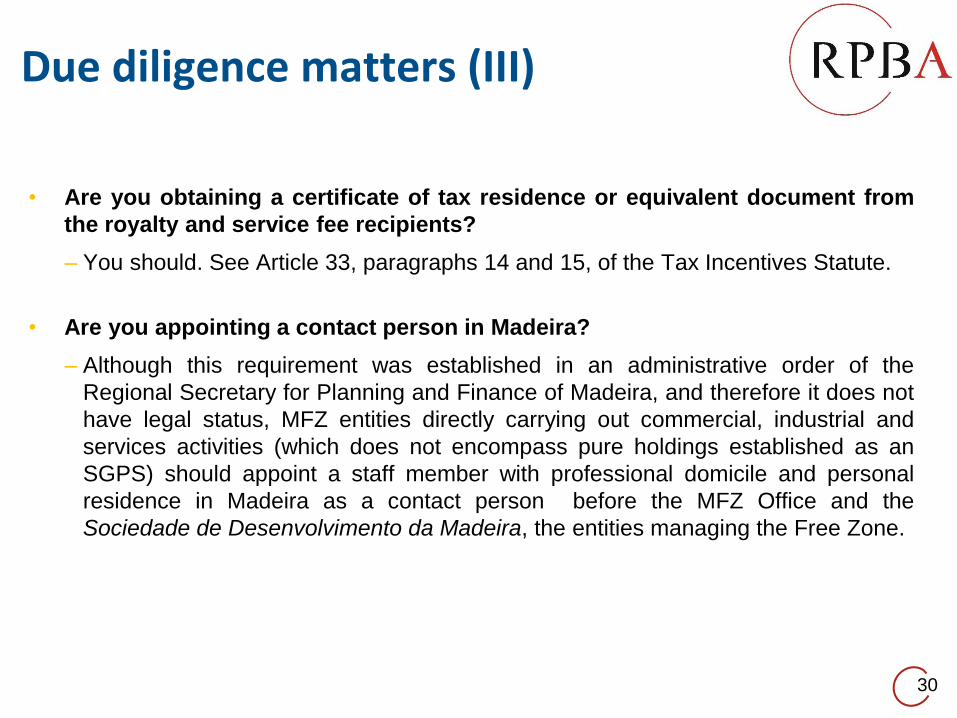

Due diligence matters (II)

• Are you obtaining a certificate of tax residence or equivalent document from

the royalty and service fee recipients?

– You should. See Article 33, paragraphs 14 and 15, of the Tax Incentives Statute.

• Are you appointing a contact person in Madeira?

– Although this requirement was established in an administrative order of the

Regional Secretary for Planning and Finance of Madeira, and therefore it does not

have legal status, MFZ entities directly carrying out commercial, industrial and

services activities (which does not encompass pure holdings established as an

SGPS) should appoint a staff member with professional domicile and personal

residence in Madeira as a contact person before the MFZ Office and the

Sociedade de Desenvolvimento da Madeira, the entities managing the Free Zone.

30

Due diligence matters (III)

31

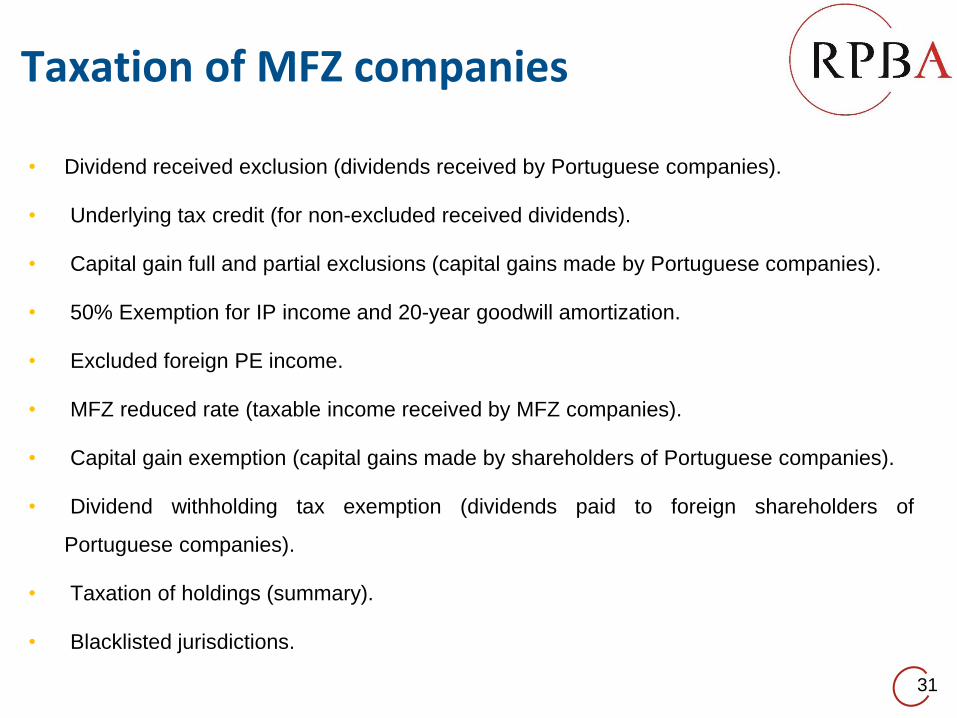

Taxation of MFZ companies

• Dividend received exclusion (dividends received by Portuguese companies).

• Underlying tax credit (for non-excluded received dividends).

• Capital gain full and partial exclusions (capital gains made by Portuguese companies).

• 50% Exemption for IP income and 20-year goodwill amortization.

• Excluded foreign PE income.

• MFZ reduced rate (taxable income received by MFZ companies).

• Capital gain exemption (capital gains made by shareholders of Portuguese companies).

• Dividend withholding tax exemption (dividends paid to foreign shareholders of

Portuguese companies).

• Taxation of holdings (summary).

• Blacklisted jurisdictions.

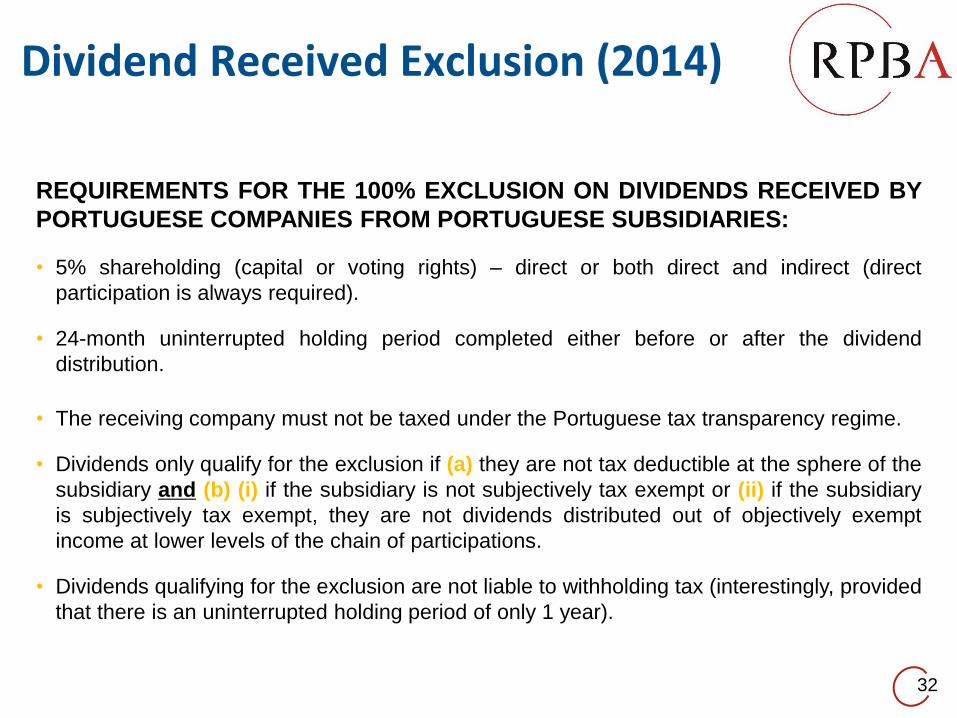

Dividend Received Exclusion (2014)

32

REQUIREMENTS FOR THE 100% EXCLUSION ON DIVIDENDS RECEIVED BY

PORTUGUESE COMPANIES FROM PORTUGUESE SUBSIDIARIES:

• 5% shareholding (capital or voting rights) – direct or both direct and indirect (direct

participation is always required).

• 24-month uninterrupted holding period completed either before or after the dividend

distribution.

• The receiving company must not be taxed under the Portuguese tax transparency regime.

• Dividends only qualify for the exclusion if (a) they are not tax deductible at the sphere of the

subsidiary and (b) (i) if the subsidiary is not subjectively tax exempt or (ii) if the subsidiary

is subjectively tax exempt, they are not dividends distributed out of objectively exempt

income at lower levels of the chain of participations.

• Dividends qualifying for the exclusion are not liable to withholding tax (interestingly, provided

that there is an uninterrupted holding period of only 1 year).

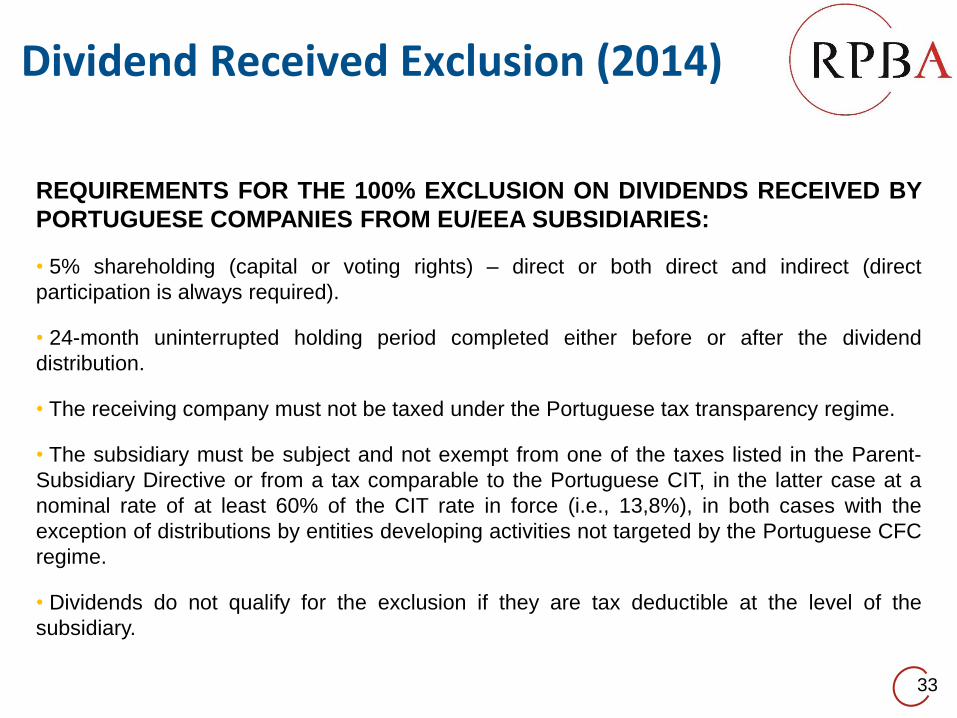

Dividend Received Exclusion (2014)

33

REQUIREMENTS FOR THE 100% EXCLUSION ON DIVIDENDS RECEIVED BY

PORTUGUESE COMPANIES FROM EU/EEA SUBSIDIARIES:

• 5% shareholding (capital or voting rights) – direct or both direct and indirect (direct

participation is always required).

• 24-month uninterrupted holding period completed either before or after the dividend

distribution.

• The receiving company must not be taxed under the Portuguese tax transparency regime.

• The subsidiary must be subject and not exempt from one of the taxes listed in the Parent-

Subsidiary Directive or from a tax comparable to the Portuguese CIT, in the latter case at a

nominal rate of at least 60% of the CIT rate in force (i.e., 13,8%), in both cases with the

exception of distributions by entities developing activities not targeted by the Portuguese CFC

regime.

• Dividends do not qualify for the exclusion if they are tax deductible at the level of the

subsidiary.

Dividend Received Exclusion (2014)

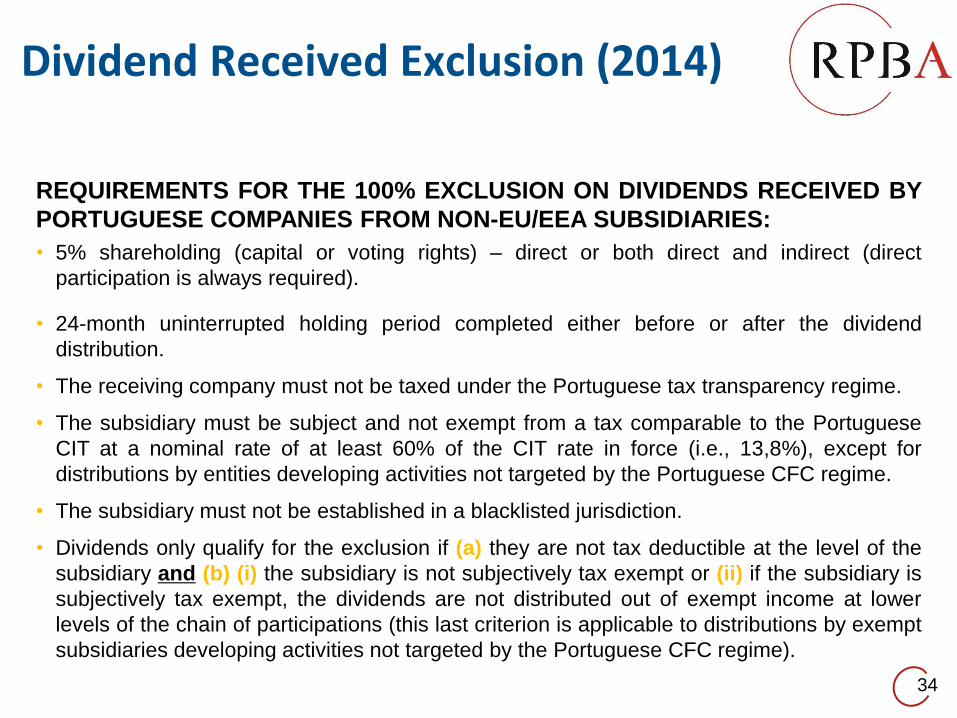

34

REQUIREMENTS FOR THE 100% EXCLUSION ON DIVIDENDS RECEIVED BY

PORTUGUESE COMPANIES FROM NON-EU/EEA SUBSIDIARIES:

• 5% shareholding (capital or voting rights) – direct or both direct and indirect (direct

participation is always required).

• 24-month uninterrupted holding period completed either before or after the dividend

distribution.

• The receiving company must not be taxed under the Portuguese tax transparency regime.

• The subsidiary must be subject and not exempt from a tax comparable to the Portuguese

CIT at a nominal rate of at least 60% of the CIT rate in force (i.e., 13,8%), except for

distributions by entities developing activities not targeted by the Portuguese CFC regime.

• The subsidiary must not be established in a blacklisted jurisdiction.

• Dividends only qualify for the exclusion if (a) they are not tax deductible at the level of the

subsidiary and (b) (i) the subsidiary is not subjectively tax exempt or (ii) if the subsidiary is

subjectively tax exempt, the dividends are not distributed out of exempt income at lower

levels of the chain of participations (this last criterion is applicable to distributions by exempt

subsidiaries developing activities not targeted by the Portuguese CFC regime).

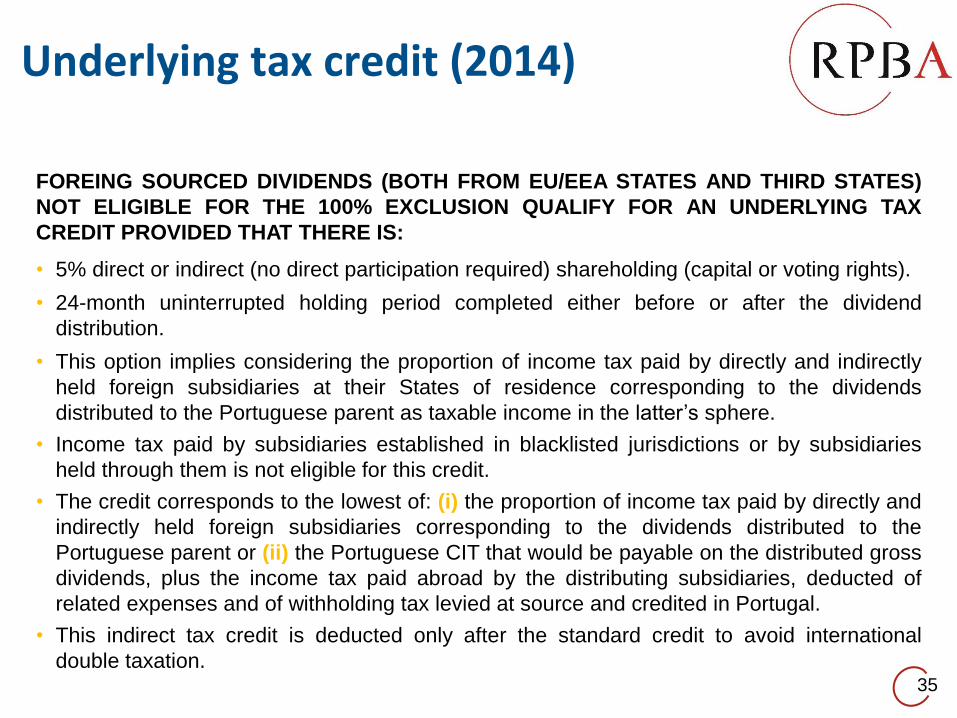

Underlying tax credit (2014)

35

FOREING SOURCED DIVIDENDS (BOTH FROM EU/EEA STATES AND THIRD STATES)

NOT ELIGIBLE FOR THE 100% EXCLUSION QUALIFY FOR AN UNDERLYING TAX

CREDIT PROVIDED THAT THERE IS:

• 5% direct or indirect (no direct participation required) shareholding (capital or voting rights).

• 24-month uninterrupted holding period completed either before or after the dividend

distribution.

• This option implies considering the proportion of income tax paid by directly and indirectly

held foreign subsidiaries at their States of residence corresponding to the dividends

distributed to the Portuguese parent as taxable income in the latter’s sphere.

• Income tax paid by subsidiaries established in blacklisted jurisdictions or by subsidiaries

held through them is not eligible for this credit.

• The credit corresponds to the lowest of: (i) the proportion of income tax paid by directly and

indirectly held foreign subsidiaries corresponding to the dividends distributed to the

Portuguese parent or (ii) the Portuguese CIT that would be payable on the distributed gross

dividends, plus the income tax paid abroad by the distributing subsidiaries, deducted of

related expenses and of withholding tax levied at source and credited in Portugal.

• This indirect tax credit is deducted only after the standard credit to avoid international

double taxation.

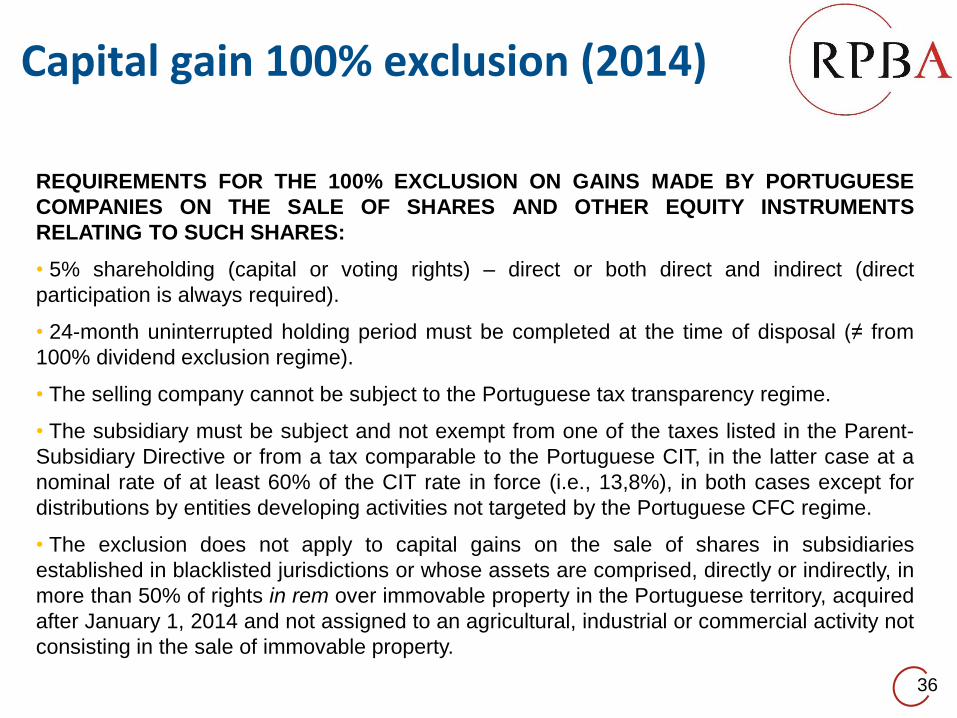

Capital gain 100% exclusion (2014)

36

REQUIREMENTS FOR THE 100% EXCLUSION ON GAINS MADE BY PORTUGUESE

COMPANIES ON THE SALE OF SHARES AND OTHER EQUITY INSTRUMENTS

RELATING TO SUCH SHARES:

• 5% shareholding (capital or voting rights) – direct or both direct and indirect (direct

participation is always required).

• 24-month uninterrupted holding period must be completed at the time of disposal (≠ from

100% dividend exclusion regime).

• The selling company cannot be subject to the Portuguese tax transparency regime.

• The subsidiary must be subject and not exempt from one of the taxes listed in the Parent-

Subsidiary Directive or from a tax comparable to the Portuguese CIT, in the latter case at a

nominal rate of at least 60% of the CIT rate in force (i.e., 13,8%), in both cases except for

distributions by entities developing activities not targeted by the Portuguese CFC regime.

• The exclusion does not apply to capital gains on the sale of shares in subsidiaries

established in blacklisted jurisdictions or whose assets are comprised, directly or indirectly, in

more than 50% of rights in rem over immovable property in the Portuguese territory, acquired

after January 1, 2014 and not assigned to an agricultural, industrial or commercial activity not

consisting in the sale of immovable property.

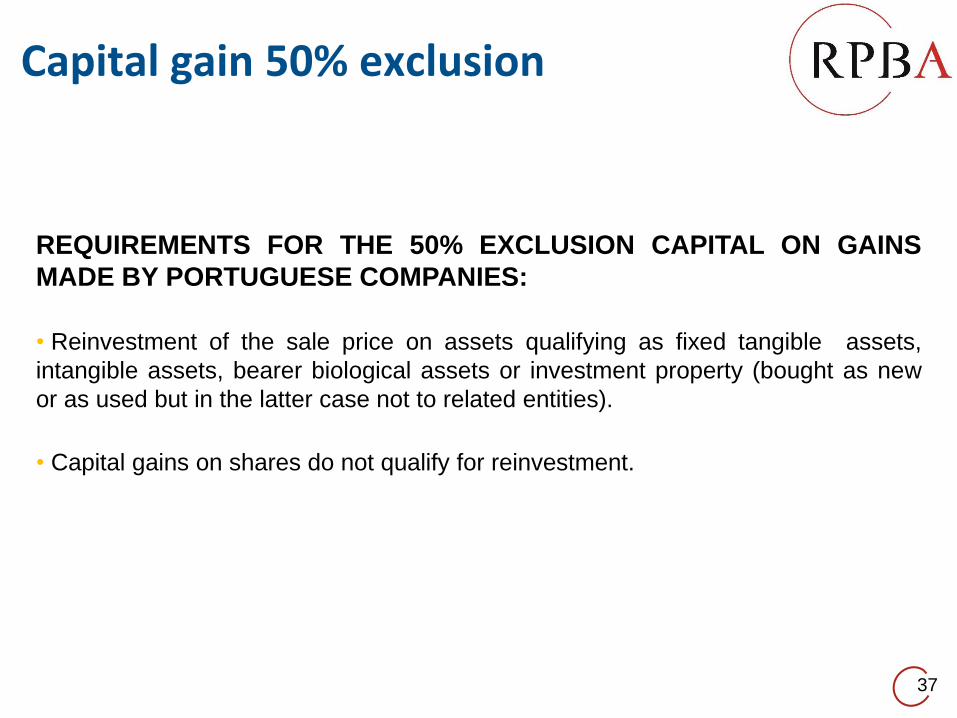

Capital gain 50% exclusion

37

REQUIREMENTS FOR THE 50% EXCLUSION CAPITAL ON GAINS

MADE BY PORTUGUESE COMPANIES:

• Reinvestment of the sale price on assets qualifying as fixed tangible assets,

intangible assets, bearer biological assets or investment property (bought as new

or as used but in the latter case not to related entities).

• Capital gains on shares do not qualify for reinvestment.

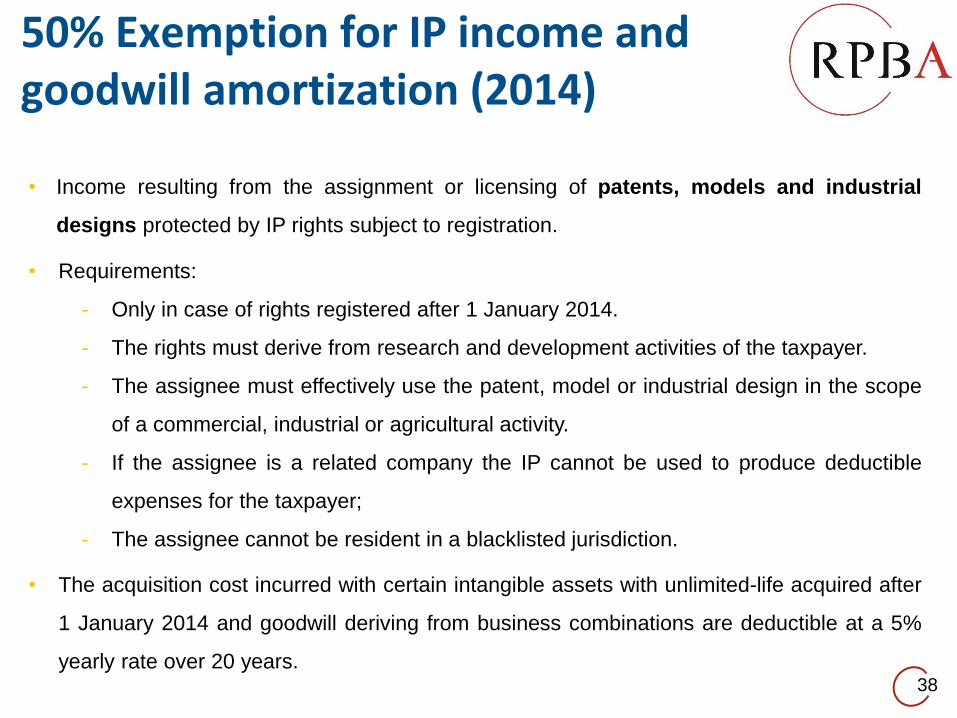

50% Exemption for IP income and goodwill amortization (2014)

38

• Income resulting from the assignment or licensing of patents, models and industrial

designs protected by IP rights subject to registration.

• Requirements:

- Only in case of rights registered after 1 January 2014.

- The rights must derive from research and development activities of the taxpayer.

- The assignee must effectively use the patent, model or industrial design in the scope

of a commercial, industrial or agricultural activity.

- If the assignee is a related company the IP cannot be used to produce deductible

expenses for the taxpayer;

- The assignee cannot be resident in a blacklisted jurisdiction.

• The acquisition cost incurred with certain intangible assets with unlimited-life acquired after

1 January 2014 and goodwill deriving from business combinations are deductible at a 5%

yearly rate over 20 years.

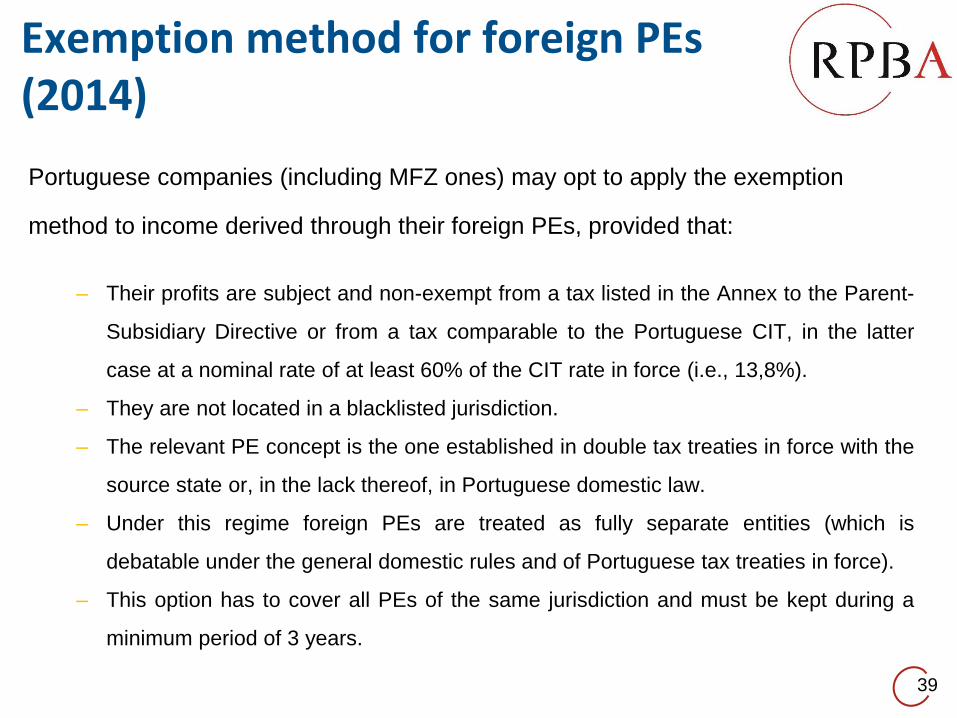

Portuguese companies (including MFZ ones) may opt to apply the exemption

method to income derived through their foreign PEs, provided that:

– Their profits are subject and non-exempt from a tax listed in the Annex to the Parent-

Subsidiary Directive or from a tax comparable to the Portuguese CIT, in the latter

case at a nominal rate of at least 60% of the CIT rate in force (i.e., 13,8%).

– They are not located in a blacklisted jurisdiction.

– The relevant PE concept is the one established in double tax treaties in force with the

source state or, in the lack thereof, in Portuguese domestic law.

– Under this regime foreign PEs are treated as fully separate entities (which is

debatable under the general domestic rules and of Portuguese tax treaties in force).

– This option has to cover all PEs of the same jurisdiction and must be kept during a

minimum period of 3 years.

39

Exemption method for foreign PEs (2014)

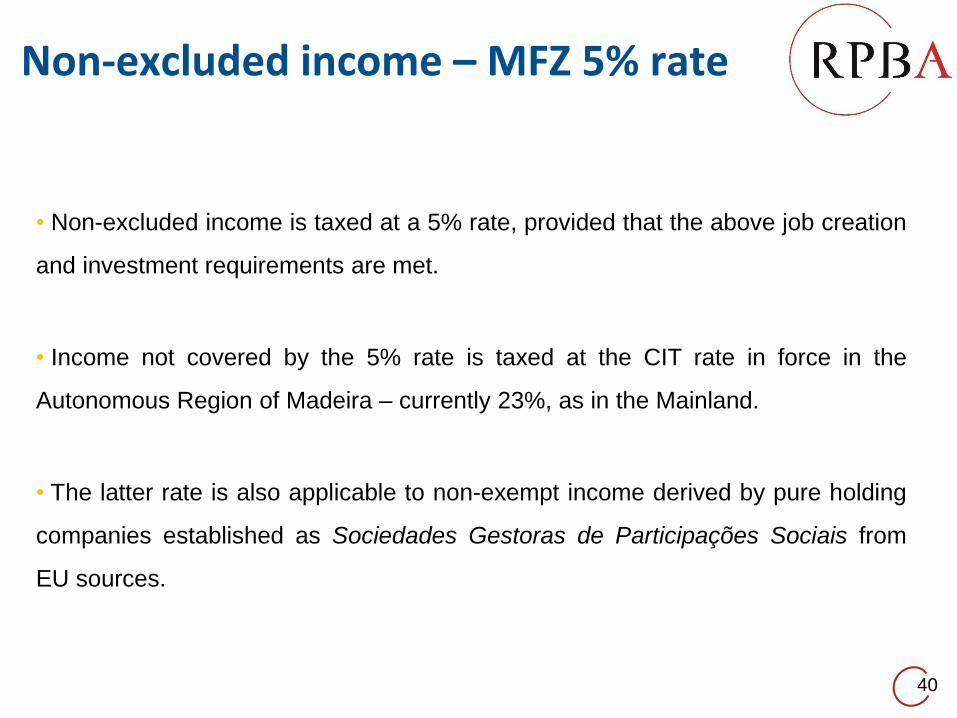

Non-excluded income – MFZ 5% rate

40

• Non-excluded income is taxed at a 5% rate, provided that the above job creation

and investment requirements are met.

• Income not covered by the 5% rate is taxed at the CIT rate in force in the

Autonomous Region of Madeira – currently 23%, as in the Mainland.

• The latter rate is also applicable to non-exempt income derived by pure holding

companies established as Sociedades Gestoras de Participações Sociais from

EU sources.

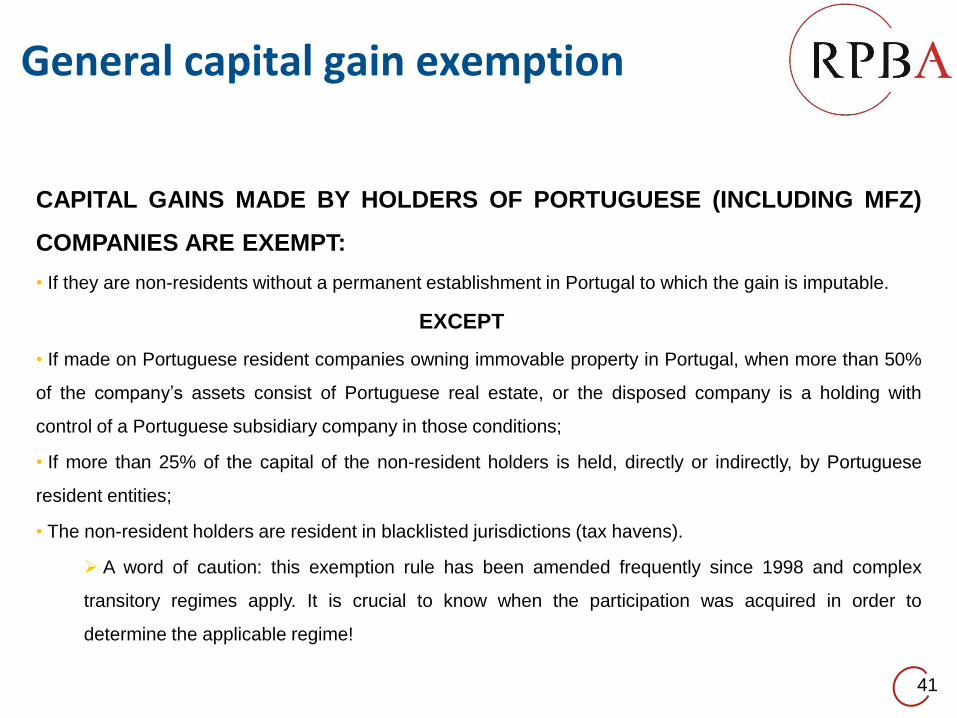

General capital gain exemption

41

CAPITAL GAINS MADE BY HOLDERS OF PORTUGUESE (INCLUDING MFZ)

COMPANIES ARE EXEMPT:

• If they are non-residents without a permanent establishment in Portugal to which the gain is imputable.

EXCEPT

• If made on Portuguese resident companies owning immovable property in Portugal, when more than 50%

of the company’s assets consist of Portuguese real estate, or the disposed company is a holding with

control of a Portuguese subsidiary company in those conditions;

• If more than 25% of the capital of the non-resident holders is held, directly or indirectly, by Portuguese

resident entities;

• The non-resident holders are resident in blacklisted jurisdictions (tax havens).

A word of caution: this exemption rule has been amended frequently since 1998 and complex

transitory regimes apply. It is crucial to know when the participation was acquired in order to

determine the applicable regime!

General dividend WHT exemption

42

DIVIDENDS PAID BY PORTUGUESE (INCLUDING MFZ) COMPANIES TO FOREIGN

CORPORATE SHAREHOLDERS ARE EXEMPT FROM CIT WITHOLDINGS PROVIDED

THAT THERE IS:

• 5% shareholding (capital or voting rights) – direct or both direct and indirect (direct participation is

always required).

• 24-month uninterrupted holding period completed before the dividend distribution (if holding period is

only subsequently completed WHT applies but a refund may be requested upon completion).

• The distributing company is not taxed under the Portuguese tax transparency regime and is liable

and not exempt from CIT (MFZ entities fulfil this condition).

• The shareholder is resident in an EU Member-State, in an EEA State provided that administrative

cooperation measures equivalent to those existing in the EU are in place with that State (in general

terms exchange of information not limited by bank secrecy and assistance in the collection of taxes)

or in a Third State which has entered into a double tax treaty with Portugal providing for the same

measures.

• The shareholder must be subject and not exempt from one of the taxes listed in the Parent-

Subsidiary Directive or from a tax comparable to the Portuguese CIT, in the latter case at a nominal

rate of at least 60% of the CIT rate in force (i.e., 13,8%).

• Distributions to shareholders not fulfilling one of these two requirements but developing activities not

targeted by the Portuguese CFC regime do not qualify for the exemption, contrarily to what happens

in the case of the CIT exclusions for dividends received and capital gains made by Portuguese

companies.

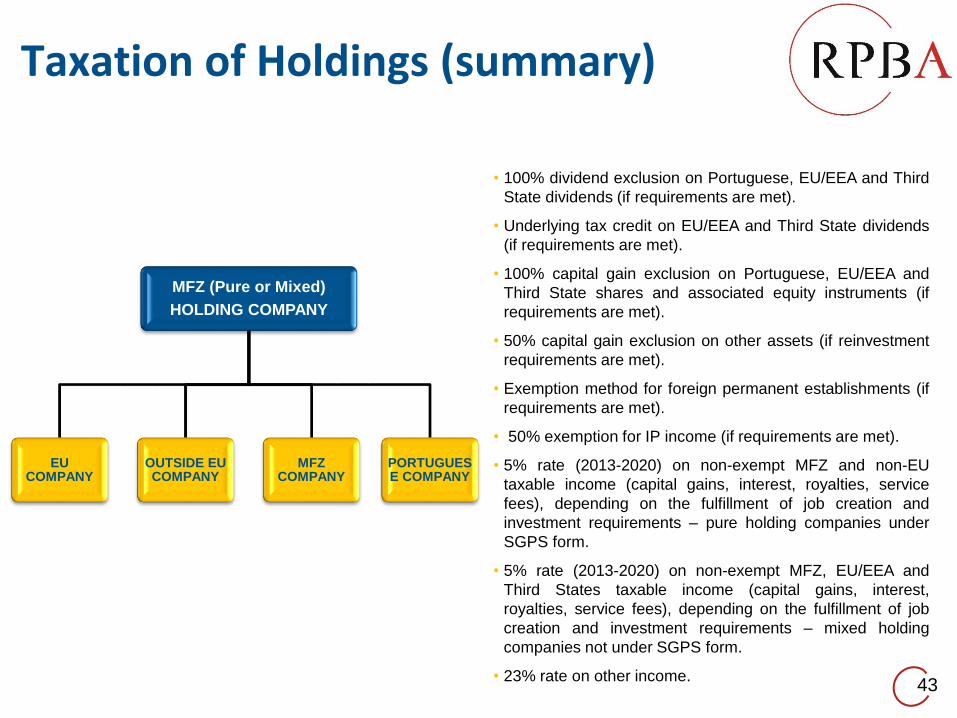

Taxation of Holdings (summary)

43

• 100% dividend exclusion on Portuguese, EU/EEA and Third

State dividends (if requirements are met).

• Underlying tax credit on EU/EEA and Third State dividends

(if requirements are met).

• 100% capital gain exclusion on Portuguese, EU/EEA and

Third State shares and associated equity instruments (if

requirements are met).

• 50% capital gain exclusion on other assets (if reinvestment

requirements are met).

• Exemption method for foreign permanent establishments (if

requirements are met).

• 50% exemption for IP income (if requirements are met).

• 5% rate (2013-2020) on non-exempt MFZ and non-EU

taxable income (capital gains, interest, royalties, service

fees), depending on the fulfillment of job creation and

investment requirements – pure holding companies under

SGPS form.

• 5% rate (2013-2020) on non-exempt MFZ, EU/EEA and

Third States taxable income (capital gains, interest,

royalties, service fees), depending on the fulfillment of job

creation and investment requirements – mixed holding

companies not under SGPS form.

• 23% rate on other income.

MFZ (Pure or Mixed)

HOLDING COMPANY

EU COMPANY

OUTSIDE EU COMPANY

MFZ COMPANY

PORTUGUESE COMPANY

• Andorra, Anguilla, Antigua and Barbuda, the Netherlands Antilles, Aruba,

Ascension, the Bahamas, Bahrain, Barbados, Belize, Bermuda, Bolivia,

Brunei, the Channel Islands (Alderney, Guernsey, Jersey, Great Sark, Herm,

Little Sark, Brechou, Jethou, and Lihou), the Cayman Islands, the Cocos o

Keeling Islands, the Cook Islands, Costa Rica, Djibouti, Dominica, United Arab

Emirates, the Falkland Islands, Fiji, Gambia, Grenada, Gibraltar, Guam,

Guyana, Honduras, Hong Kong, Jamaica, Jordan, the Queshm Island, Kiribati,

Kuwait, Labuan, Lebanon, Liberia, Liechtenstein, the Maldives, the Isle of

Man, the Northern Marianas Islands, the Marshall Islands, Mauritius, Monaco,

Montserrat, Nauru, Natal, Niue, Norfolk Island, Oman, Palau, Panama,

Pitcairn Island, French Polynesia, Puerto Rico, Qatar, the Solomon Islands,

American Samoa, Samoa, St. Helena, St. Lucia, St. Kitts-Nevis, San Marino,

St. Pierre and Miguelon, St. Vincent and the Grenadines, the Seychelles,

Swaziland, Svalbard Islands (Spitsbergen archipelago and the Bjornoya

island), Tokelau, Tonga, Trinidad and Tobago, Tristão da Cunha Island, Turks

and Caicos Islands, Tuvalu, Uruguay, Vanuatu, the British Virgin Islands, the

U.S. Virgin Islands, and Yemen. And also “Other Pacific Islands not

specifically mentioned”.44

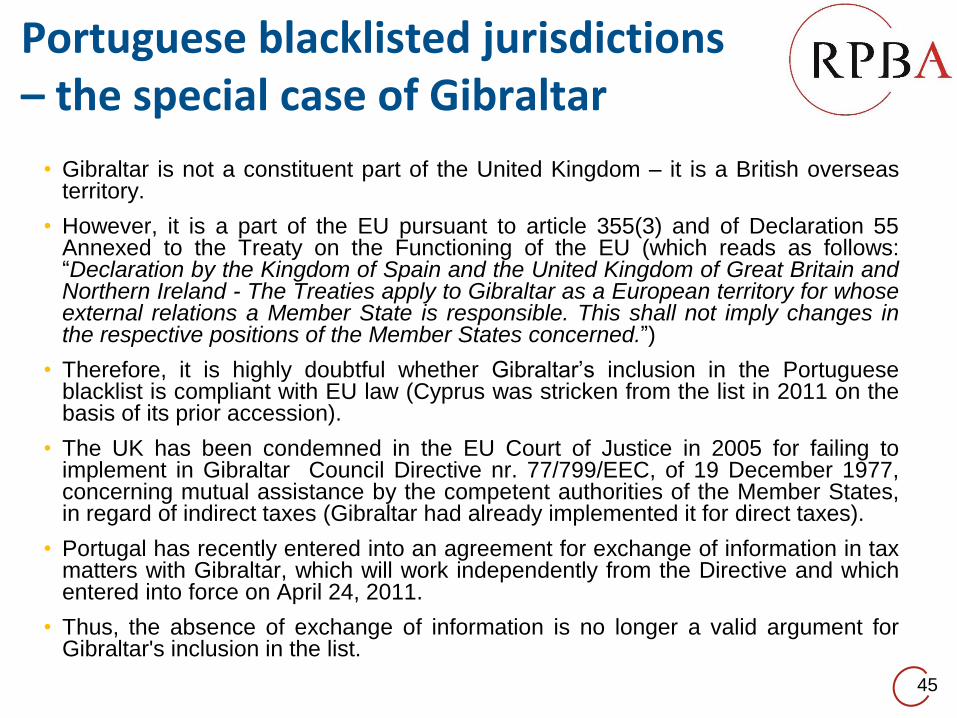

Portuguese blacklisted jurisdictions

• Gibraltar is not a constituent part of the United Kingdom – it is a British overseasterritory.

• However, it is a part of the EU pursuant to article 355(3) and of Declaration 55Annexed to the Treaty on the Functioning of the EU (which reads as follows:“Declaration by the Kingdom of Spain and the United Kingdom of Great Britain andNorthern Ireland - The Treaties apply to Gibraltar as a European territory for whoseexternal relations a Member State is responsible. This shall not imply changes inthe respective positions of the Member States concerned.”)

• Therefore, it is highly doubtful whether Gibraltar’s inclusion in the Portugueseblacklist is compliant with EU law (Cyprus was stricken from the list in 2011 on thebasis of its prior accession).

• The UK has been condemned in the EU Court of Justice in 2005 for failing toimplement in Gibraltar Council Directive nr. 77/799/EEC, of 19 December 1977,concerning mutual assistance by the competent authorities of the Member States,in regard of indirect taxes (Gibraltar had already implemented it for direct taxes).

• Portugal has recently entered into an agreement for exchange of information in taxmatters with Gibraltar, which will work independently from the Directive and whichentered into force on April 24, 2011.

• Thus, the absence of exchange of information is no longer a valid argument forGibraltar's inclusion in the list.

45

Portuguese blacklisted jurisdictions – the special case of Gibraltar

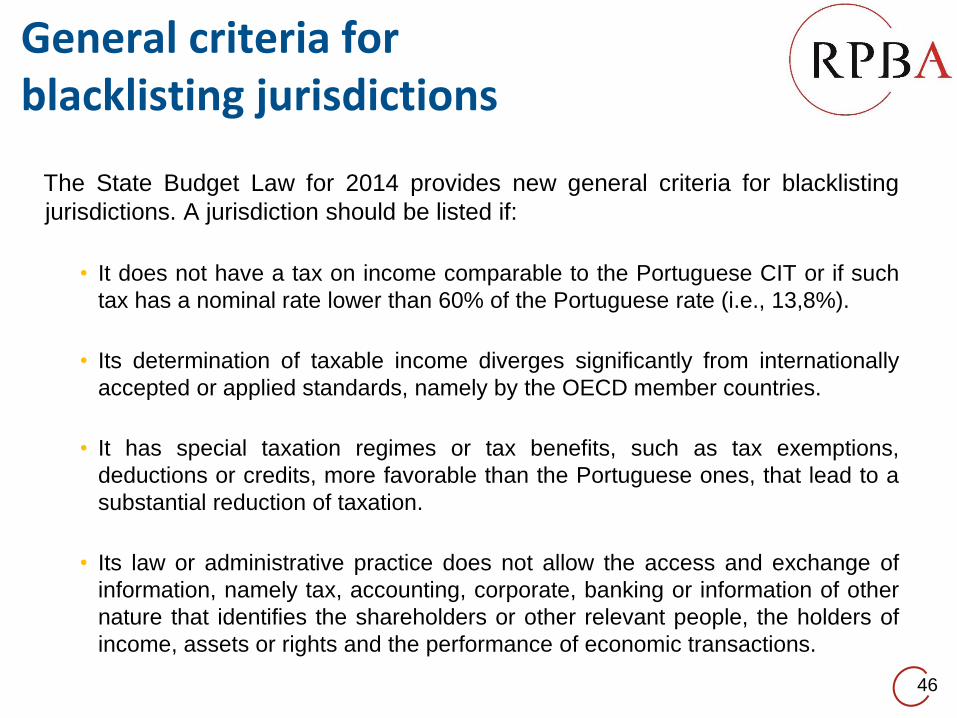

The State Budget Law for 2014 provides new general criteria for blacklisting

jurisdictions. A jurisdiction should be listed if:

• It does not have a tax on income comparable to the Portuguese CIT or if such

tax has a nominal rate lower than 60% of the Portuguese rate (i.e., 13,8%).

• Its determination of taxable income diverges significantly from internationally

accepted or applied standards, namely by the OECD member countries.

• It has special taxation regimes or tax benefits, such as tax exemptions,

deductions or credits, more favorable than the Portuguese ones, that lead to a

substantial reduction of taxation.

• Its law or administrative practice does not allow the access and exchange of

information, namely tax, accounting, corporate, banking or information of other

nature that identifies the shareholders or other relevant people, the holders of

income, assets or rights and the performance of economic transactions.

46

General criteria for blacklisting jurisdictions

• Any listed jurisdiction may request to the Portuguese government a

revision and removal from the blacklist grounded on the non-fulfilment of

the general criteria mentioned above.

• Any delisting will only have effects for the future and the list currently in

force remains applicable until the publication of a new one.

47

General criteria for blacklisting jurisdictions

• Commissionaire or Trading Structure

• Patent Royalty and Service Structure

• Capital Duty Structure

• Tax Sparing Structure (Loan)

• Controlled Foreign Company Blocking Structure

• Dividend Reduction Structure

48

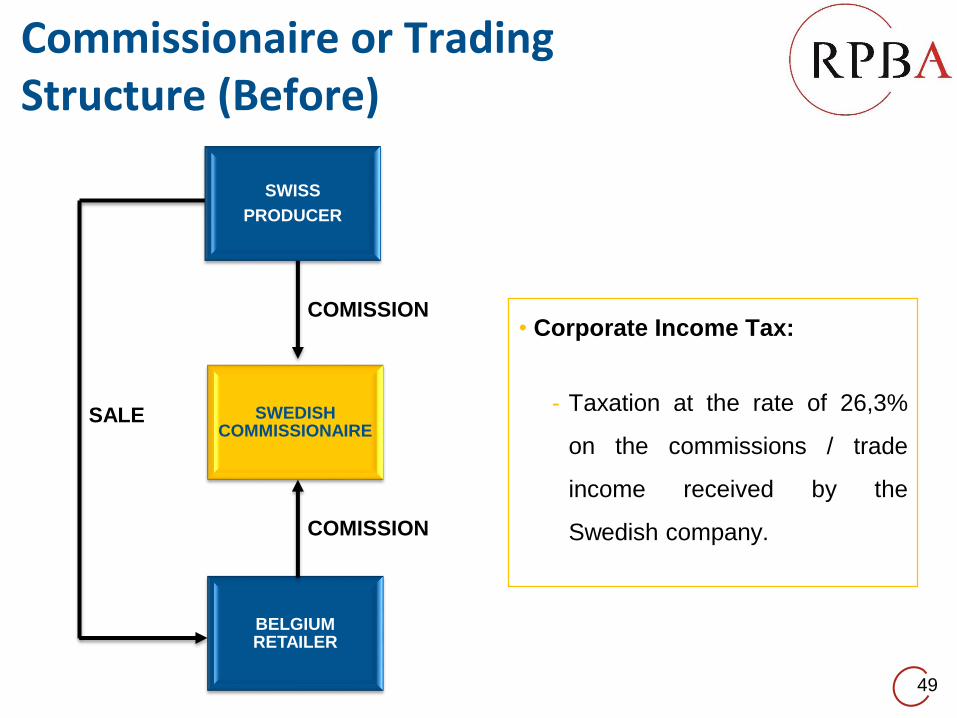

Madeira’s Practical Structures

SWISS

PRODUCER

SWEDISH COMMISSIONAIRE

BELGIUM RETAILER

49

Commissionaire or TradingStructure (Before)

• Corporate Income Tax:

- Taxation at the rate of 26,3%

on the commissions / trade

income received by the

Swedish company.

SALE

COMISSION

COMISSION

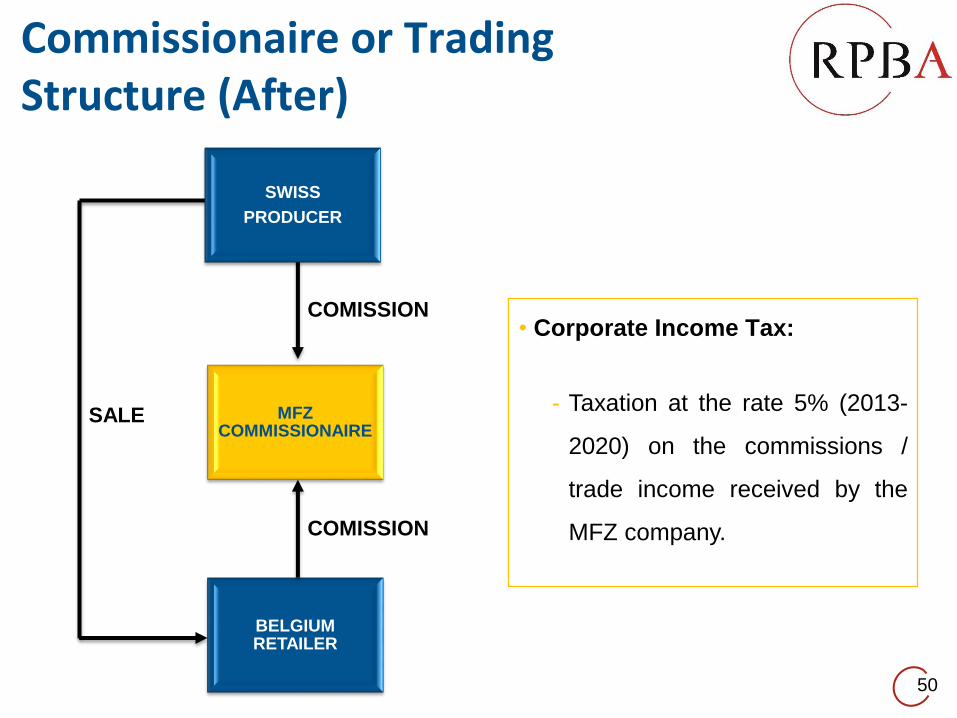

SWISS

PRODUCER

MFZ COMMISSIONAIRE

BELGIUM RETAILER

SALE

COMISSION

COMISSION

50

Commissionaire or Trading Structure (After)

• Corporate Income Tax:

- Taxation at the rate 5% (2013-

2020) on the commissions /

trade income received by the

MFZ company.

51

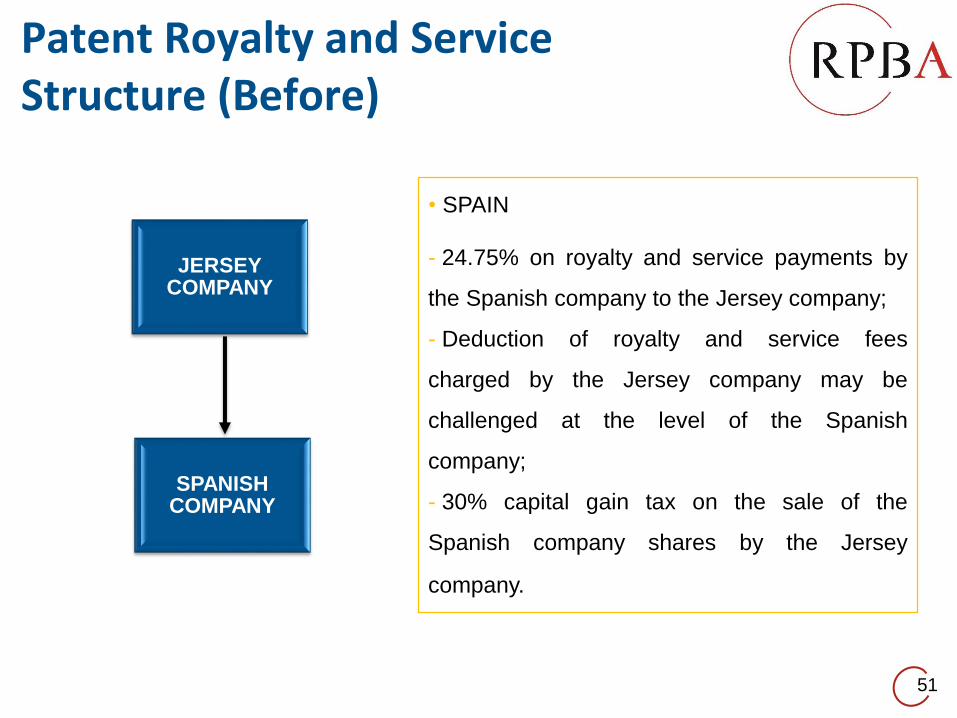

Patent Royalty and Service Structure (Before)

• SPAIN

- 24.75% on royalty and service payments by

the Spanish company to the Jersey company;

- Deduction of royalty and service fees

charged by the Jersey company may be

challenged at the level of the Spanish

company;

- 30% capital gain tax on the sale of the

Spanish company shares by the Jersey

company.

JERSEY COMPANY

SPANISH COMPANY

52

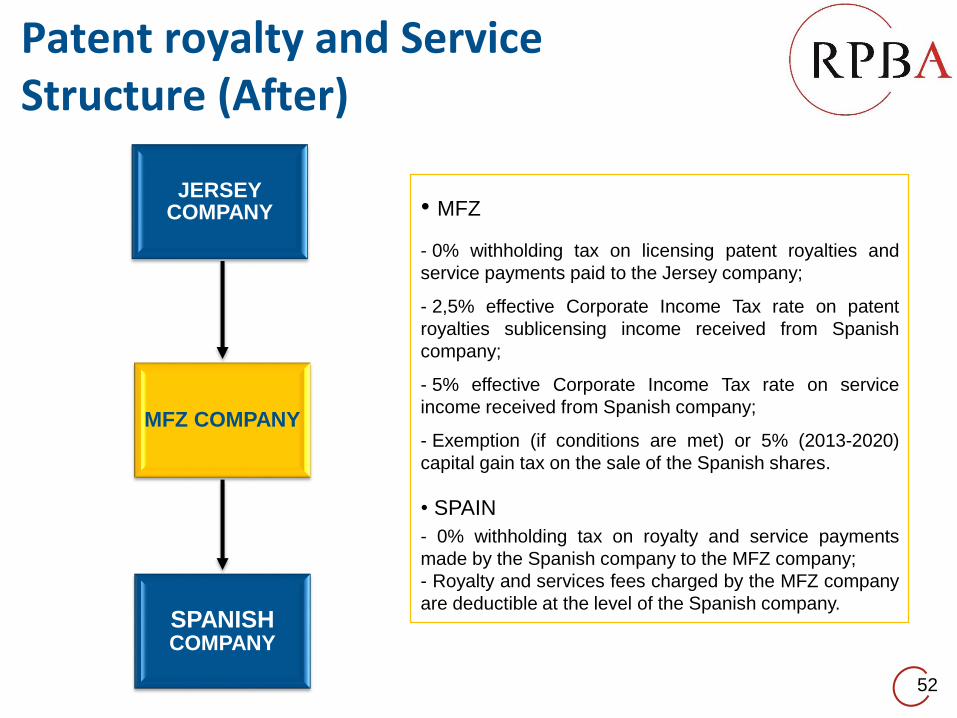

Patent royalty and ServiceStructure (After)

• MFZ

- 0% withholding tax on licensing patent royalties and

service payments paid to the Jersey company;

- 2,5% effective Corporate Income Tax rate on patent

royalties sublicensing income received from Spanish

company;

- 5% effective Corporate Income Tax rate on service

income received from Spanish company;

- Exemption (if conditions are met) or 5% (2013-2020)

capital gain tax on the sale of the Spanish shares.

• SPAIN

- 0% withholding tax on royalty and service payments

made by the Spanish company to the MFZ company;

- Royalty and services fees charged by the MFZ company

are deductible at the level of the Spanish company.

JERSEY COMPANY

MFZ COMPANY

SPANISH COMPANY

53

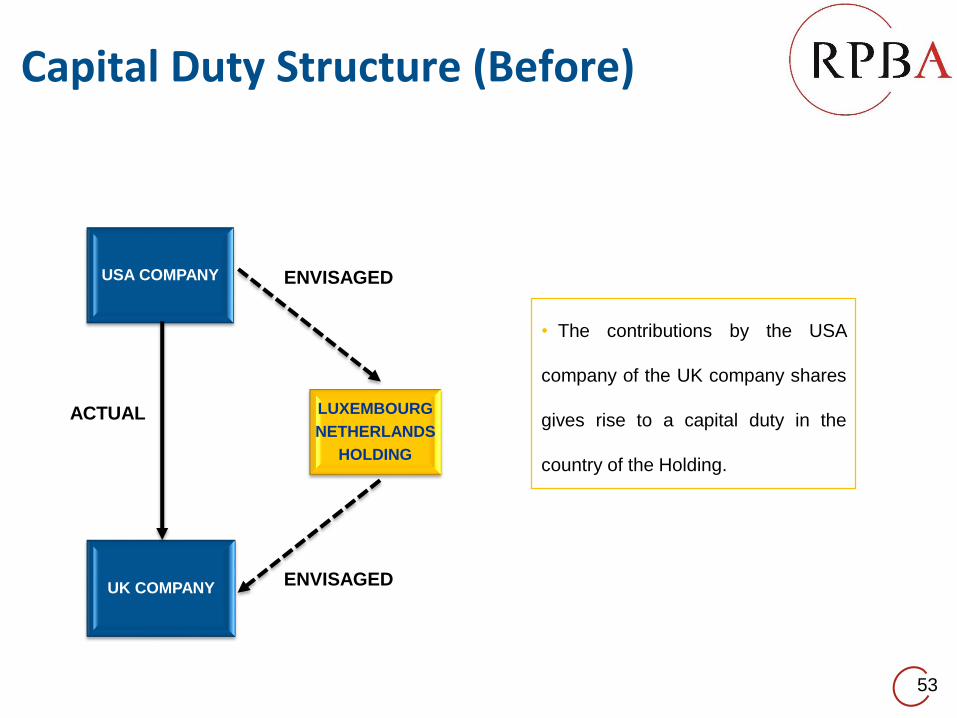

Capital Duty Structure (Before)

• The contributions by the USA

company of the UK company shares

gives rise to a capital duty in the

country of the Holding.

USA COMPANY

LUXEMBOURG

NETHERLANDS

HOLDING

UK COMPANY

ACTUAL

ENVISAGED

ENVISAGED

54

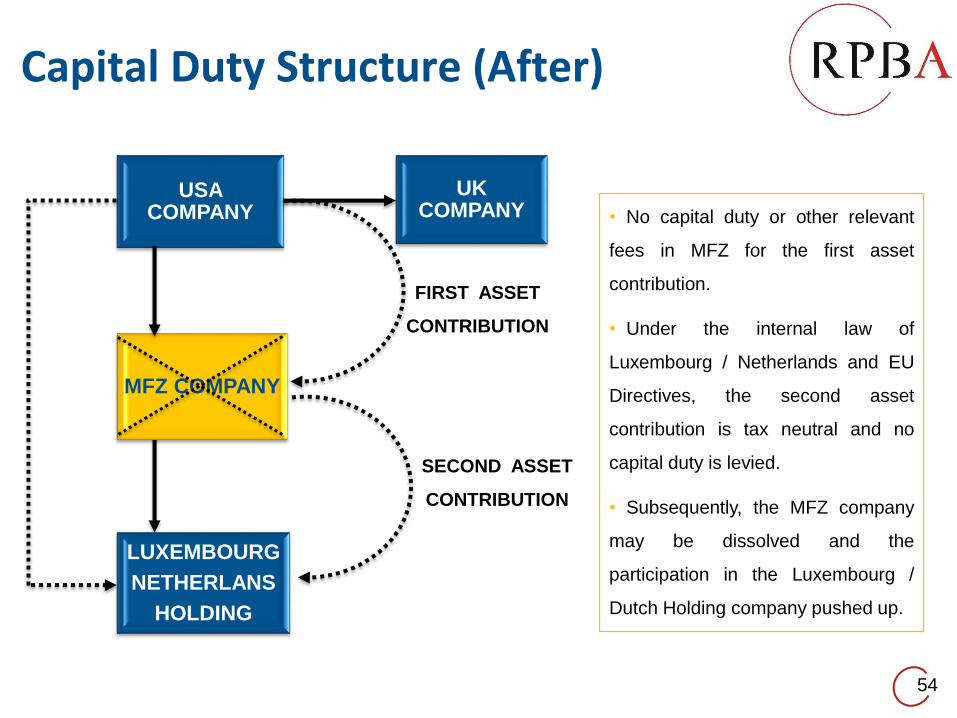

Capital Duty Structure (After)

• No capital duty or other relevant

fees in MFZ for the first asset

contribution.

• Under the internal law of

Luxembourg / Netherlands and EU

Directives, the second asset

contribution is tax neutral and no

capital duty is levied.

• Subsequently, the MFZ company

may be dissolved and the

participation in the Luxembourg /

Dutch Holding company pushed up.

USA COMPANY

UK COMPANY

MFZ COMPANY

LUXEMBOURG

NETHERLANS

HOLDING

FIRST ASSET

CONTRIBUTION

SECOND ASSET

CONTRIBUTION

55

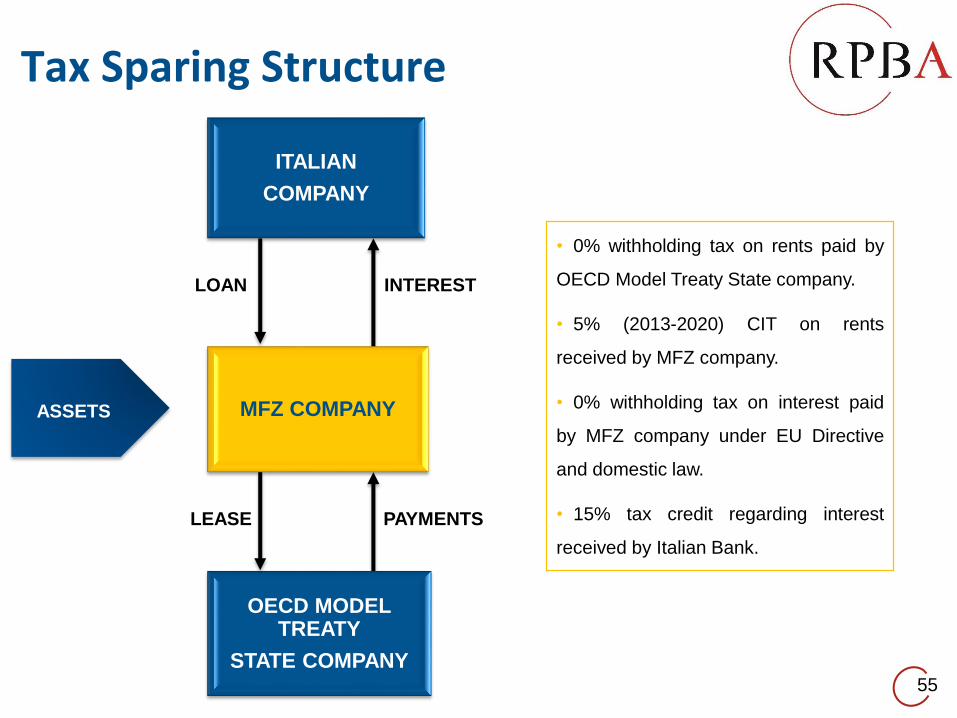

Tax Sparing Structure

• 0% withholding tax on rents paid by

OECD Model Treaty State company.

• 5% (2013-2020) CIT on rents

received by MFZ company.

• 0% withholding tax on interest paid

by MFZ company under EU Directive

and domestic law.

• 15% tax credit regarding interest

received by Italian Bank.

ITALIAN

COMPANY

MFZ COMPANY

OECD MODEL TREATY

STATE COMPANY

ASSETS

LOAN

LEASE

INTEREST

PAYMENTS

56

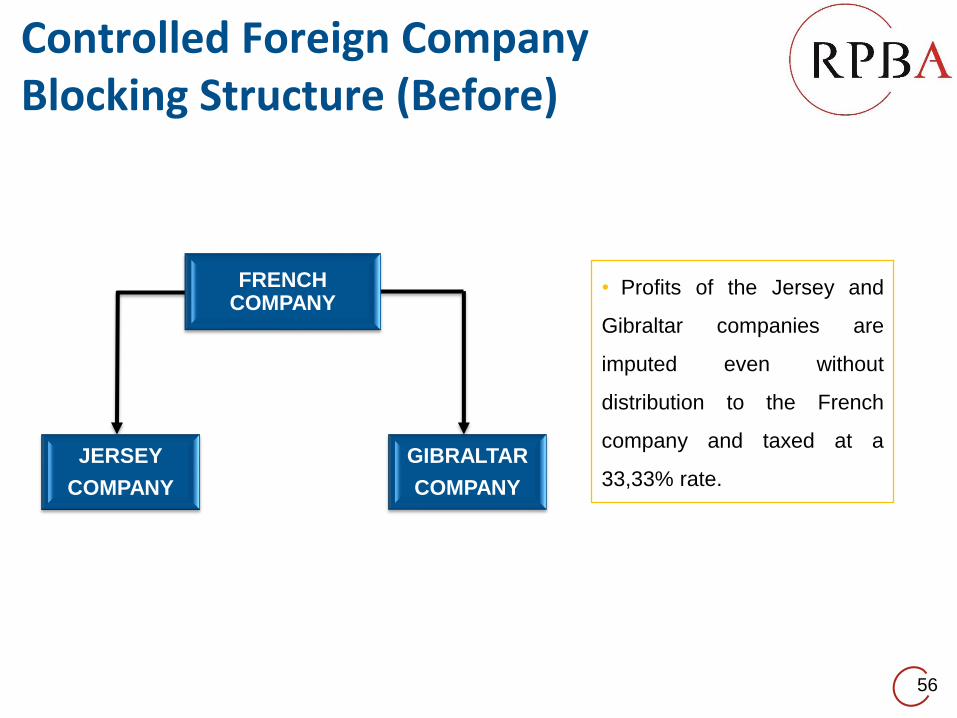

Controlled Foreign Company Blocking Structure (Before)

• Profits of the Jersey and

Gibraltar companies are

imputed even without

distribution to the French

company and taxed at a

33,33% rate.

FRENCH COMPANY

GIBRALTAR

COMPANY

JERSEY

COMPANY

57

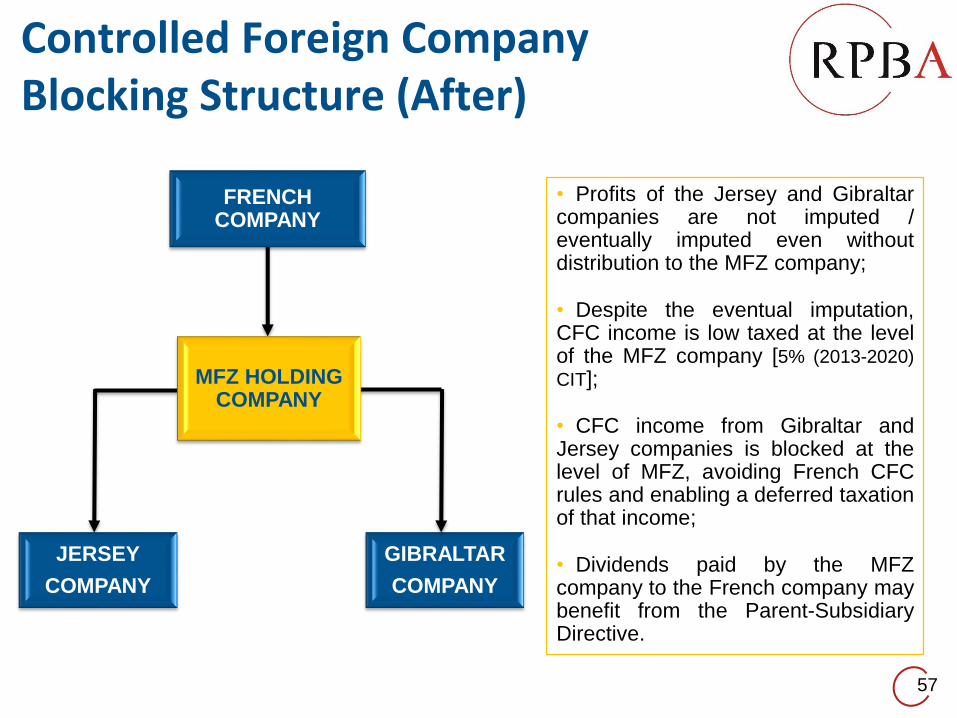

Controlled Foreign Company Blocking Structure (After)

• Profits of the Jersey and Gibraltarcompanies are not imputed /eventually imputed even withoutdistribution to the MFZ company;

• Despite the eventual imputation,CFC income is low taxed at the levelof the MFZ company [5% (2013-2020)

CIT];

• CFC income from Gibraltar andJersey companies is blocked at thelevel of MFZ, avoiding French CFCrules and enabling a deferred taxationof that income;

• Dividends paid by the MFZcompany to the French company maybenefit from the Parent-SubsidiaryDirective.

FRENCH COMPANY

GIBRALTAR

COMPANY

JERSEY

COMPANY

MFZ HOLDING COMPANY

58

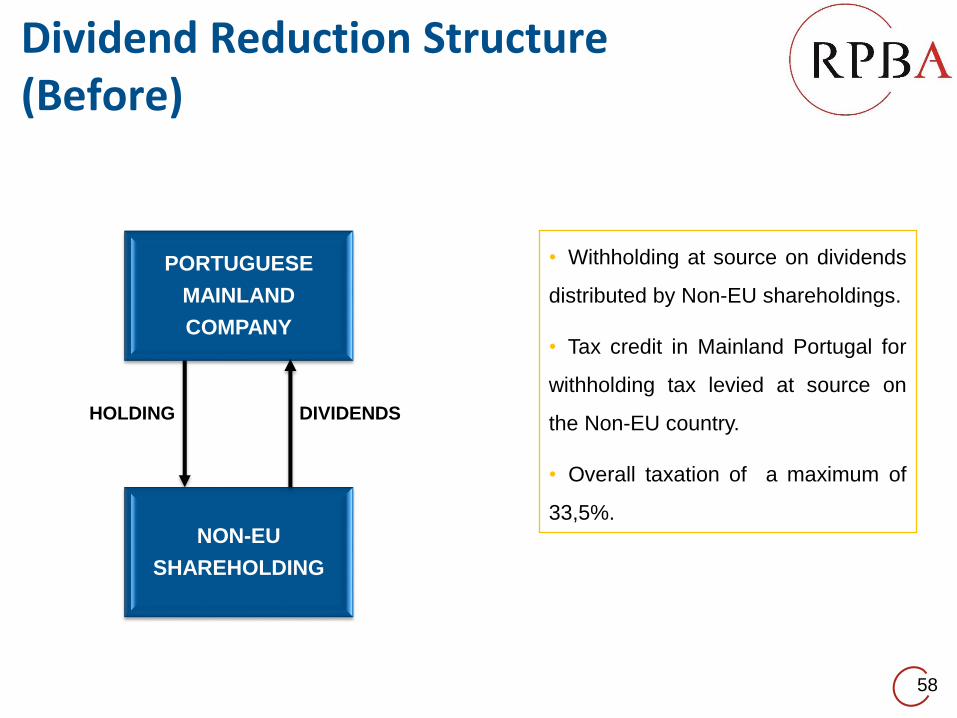

Dividend Reduction Structure (Before)

• Withholding at source on dividends

distributed by Non-EU shareholdings.

• Tax credit in Mainland Portugal for

withholding tax levied at source on

the Non-EU country.

• Overall taxation of a maximum of

33,5%.NON-EU

SHAREHOLDING

PORTUGUESE

MAINLAND

COMPANY

HOLDING DIVIDENDS

59

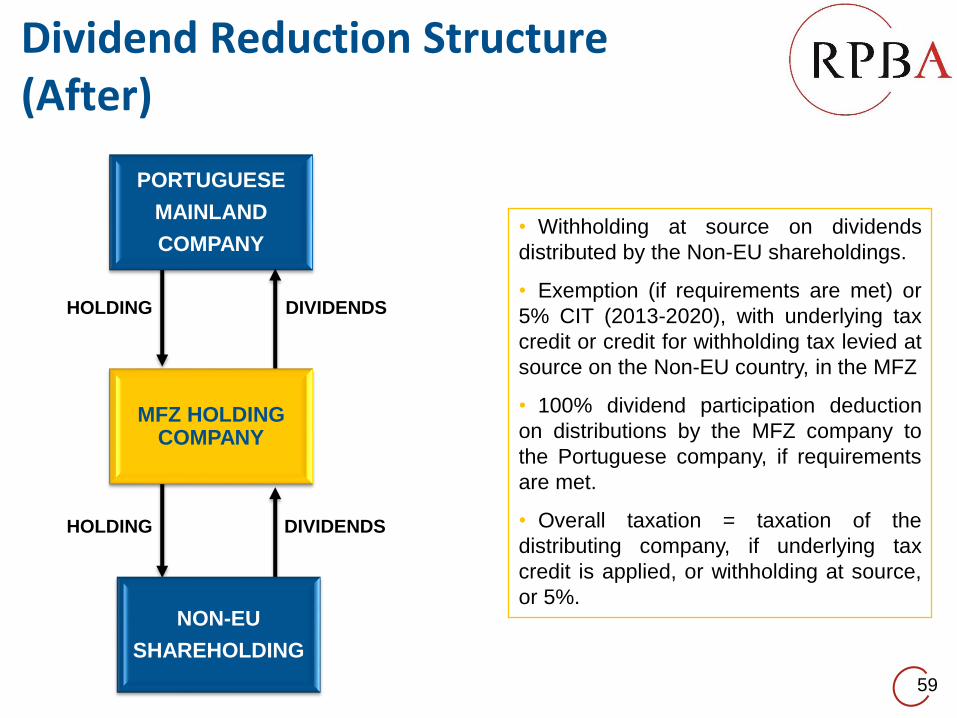

Dividend Reduction Structure (After)

• Withholding at source on dividends

distributed by the Non-EU shareholdings.

• Exemption (if requirements are met) or

5% CIT (2013-2020), with underlying tax

credit or credit for withholding tax levied at

source on the Non-EU country, in the MFZ

• 100% dividend participation deduction

on distributions by the MFZ company to

the Portuguese company, if requirements

are met.

• Overall taxation = taxation of the

distributing company, if underlying tax

credit is applied, or withholding at source,

or 5%.NON-EU

SHAREHOLDING

PORTUGUESE

MAINLAND

COMPANY

MFZ HOLDING COMPANY

HOLDING

HOLDING

DIVIDENDS

DIVIDENDS

Contact details

• Pessoa de Contacto / Contact Person: Ricardo da Palma Borges / [email protected]

- Sócio-Administrador da / Managing Partner of RICARDO da PALMA BORGES & ASSOCIADOS,SOCIEDADE DE ADVOGADOS, R.L.

- Licenciado e Mestre em Direito Fiscal / J.D. and LL.M. in Tax Law

- Advogado-Especialista em Direito Fiscal pela Ordem dos Advogados / Specialist Lawyer in Tax Law bythe Portuguese Bar Association

- Antigo Assistente da Faculdade de Direito da Universidade de Lisboa / Former Teaching Assistant ofthe Lisbon University School of Law (1994-2007)

- Ex-Tax Manager da Ernst & Young e ex-Adjunto do Secretário de Estado dos Assuntos Fiscais / FormerTax Manager at Ernst & Young and Aid to the Portuguese Secretary of State of Tax Affairs

• Sede social / Registered office: Rua Abranches Ferrão, n.º 10, 9.º Piso, Fracção D, 1600-001 Lisboa,Portugal

• Registada na Ordem dos Advogados Portugueses sob o n.º: 77/2008 / Inscribed on the Portuguese BarAssociation under the registration nr.: 77/2008

• Capital Social em Euros / Stock Capital in Euro: 5.000

• Número Único de Identificação Fiscal e de Pessoa Colectiva / Tax and Corporate Body SingleIdentification Number: PT 508 674 301

60

Proper legal advice is recommended before any decision is taken on this subject. RPBA hasan in-depth knowledge and expertise on the Madeira Free Zone regime. To book aconsultation or to obtain our professional fees on this subject please e-mail us:

Recent tax recognition

• Chambers & Partners – Ricardo Band 1 / RPBA Band 3 (2015)

• Legal 500 – Ricardo and Pedro are Recommended Lawyers / RPBA Band 3 (2015)

• World Tax – Ricardo mentioned / RPBA Tier 3 (2015)

• Best Lawyers – Ricardo ranked under the "Tax Law" practice area and the "Tax Planning"subspecialty (2015)

• World Transfer Pricing – Ricardo mentioned / RPBA Tier 3 (2014)

• Tax Directors Handbook – Ricardo mentioned / RPBA Tier 3 (2015)

• Who´s Who Legal – Ricardo ranked as a top lawyer in the Corporate Tax Lawyers directory (2013)

• Acquisition International Tax Award – RPBA Portuguese Tax Law Boutique Firm of the Year (2015)

• Acquisition International Legal Award – RPBA Boutique Law Firm of the Year – Portugal (2014)

• Corporate Intl Magazine Legal Award – RPBA Boutique Tax Law Firm of the Year in Portugal(2014)

• Global Law Experts - RPBA Boutique Tax Law Firm of the Year – Portugal (2015)

• Corporate Intl - RPBA Tax Law Firm of the Year in Portugal (2014)

61

General warning, disclaimer, copyright and authorised use

• In the preparation of this presentation, every effort has been made to offer current, correct and clearlyexpressed information. However, the said information is intended to afford general guidelines only. Thispresentation reflects information current at 29 October 2014.

• This presentation is distributed with the understanding that RICARDO da PALMA BORGES & ASSOCIADOS,SOCIEDADE DE ADVOGADOS, R.L. is not responsible for the result of any actions taken on the basis ofinformation herein included, nor for any errors or omissions contained herein.

• RICARDO da PALMA BORGES & ASSOCIADOS, SOCIEDADE DE ADVOGADOS, R.L. is not attempting throughthis work to render legal or tax advice and the information in this presentation should be used as a researchtool only, and not in lieu of individual professional study with respect to client legal matters.

• Portuguese domestic legislation, foreign legislation, EU Directives and tax treaties have anti-abuseprovisions, and each actual client structure should be analysed taking those into account.

• RICARDO da PALMA BORGES & ASSOCIADOS, SOCIEDADE DE ADVOGADOS, R.L. is the copyright owner ofthis presentation and hereby grants you a non-exclusive, non-transferable license to use this presentationsolely for your internal business, provided that you do not modify its content in any way and that you donot retain any copyright or other proprietary notices displayed on such content. You may not otherwisereproduce, modify, distribute, transmit, post or disclose the content on this presentation without RICARDOda PALMA BORGES & ASSOCIADOS, SOCIEDADE DE ADVOGADOS, R.L.’s prior written consent.

62

(+351) 212 402 743

www.rpba.pt

www.linkedin.com/company/rpba

www.slideshare.net/rpba

15