CIMA F2 Refresher - Qunber Raza

91

1 1 Financial Management Paper F2 Sir Qunber Raza Rizvi https://www.facebook.com/Qunbe rRaza

Transcript of CIMA F2 Refresher - Qunber Raza

1 1

Financial Management

Paper F2Sir Qunber Raza Rizvihttps://www.facebook.com/QunberRaza

2 2

Introduction to the Paper

3 3

Syllabus

• Prepare consolidated accounts, employing accounting standards 35%

• Evaluate financial statements and analyse performance 35%

• Profit measurement 20%

• Developments in external reporting 10%

4 4

1Session Accounting for Subsidiaries

5 5

What is a Group?

P

S

Control Group

6 6

W1 Group Structure

Parent

%

Subsidiary

7 7

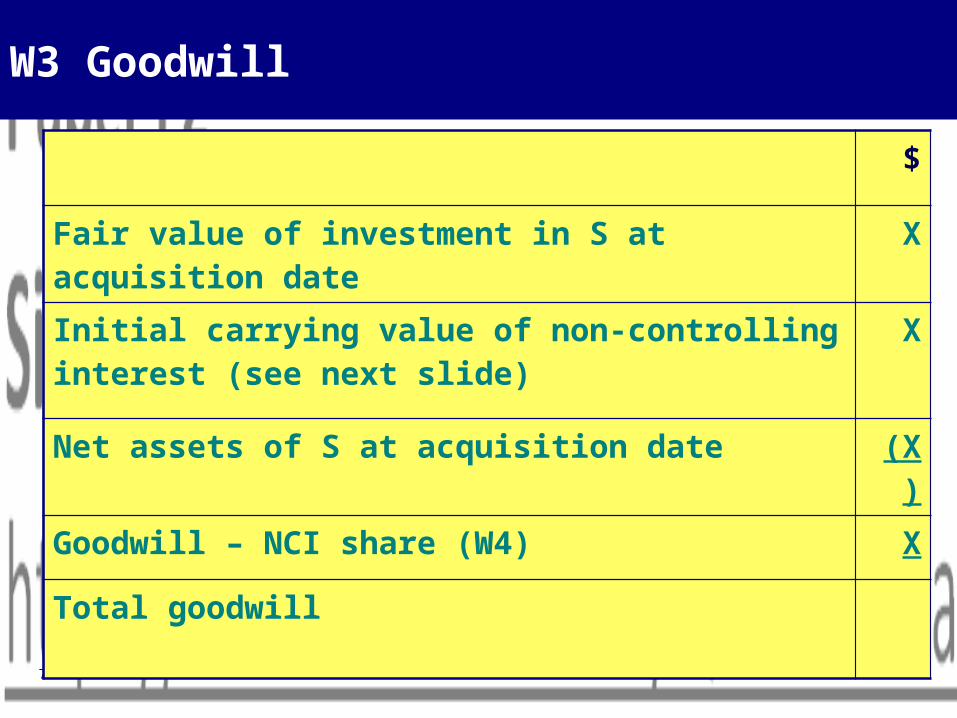

W3 Goodwill

$

Fair value of investment in S at acquisition date X

Initial carrying value of non-controlling interest (see next slide)

X

Net assets of S at acquisition date (X)

Goodwill – NCI share (W4) X

Total goodwill

8 8

Initial carrying value of NCI?

EITHER1. Fair value of S at date of acquisition;

OR2. NCI share of net identifiable assets of S at

date of acquisition.

• Choice made on an acquisition by acquisition basis

9 9

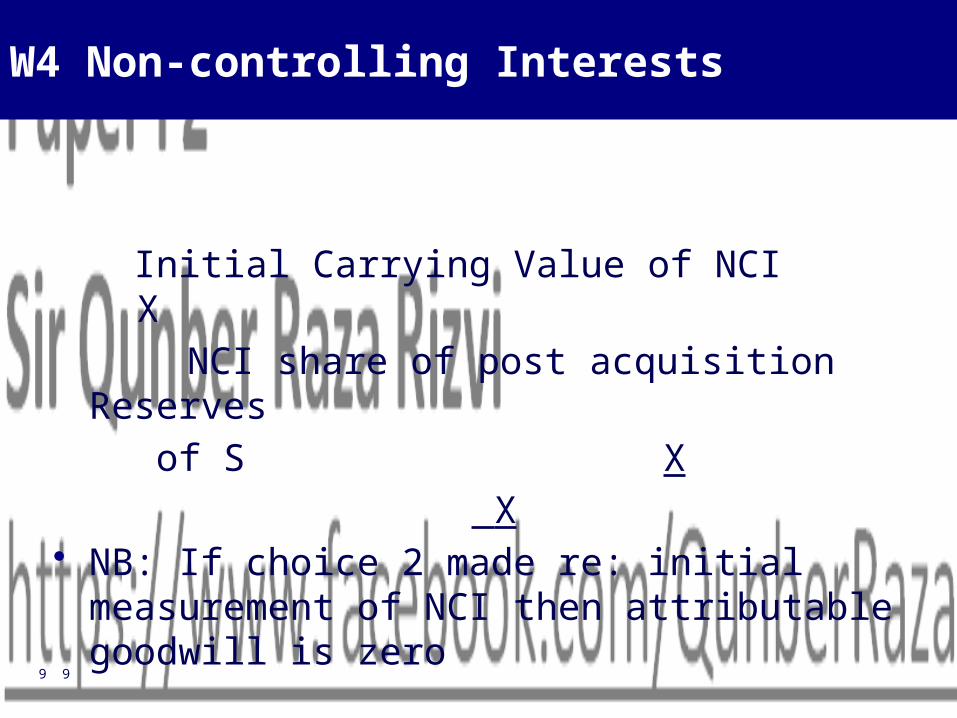

W4 Non-controlling Interests

Initial Carrying Value of NCI X NCI share of post acquisition Reserves

of S X X

• NB: If choice 2 made re: initial measurement of NCI then attributable goodwill is zero

10 10

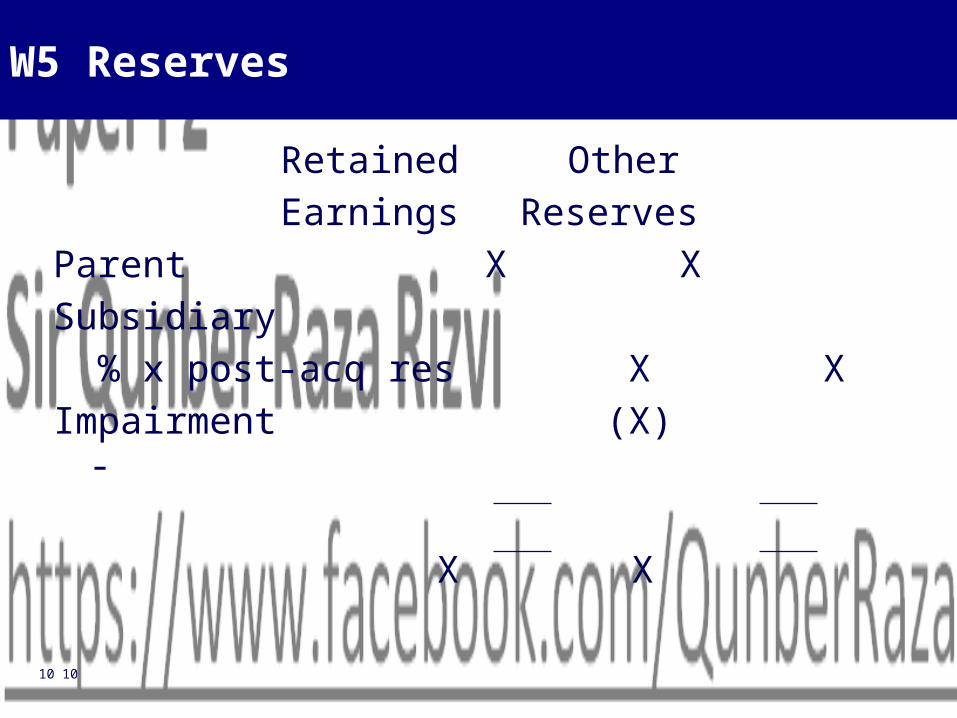

W5 Reserves

Retained OtherEarnings

ReservesParent X XSubsidiary % x post-acq res X XImpairment (X) -

X X

11 11

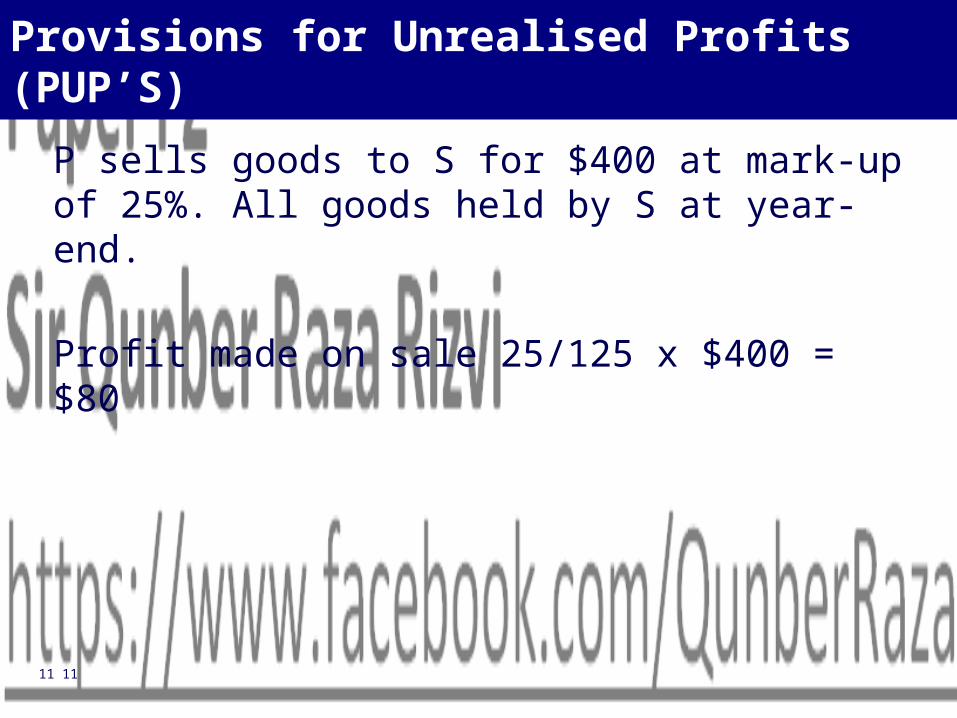

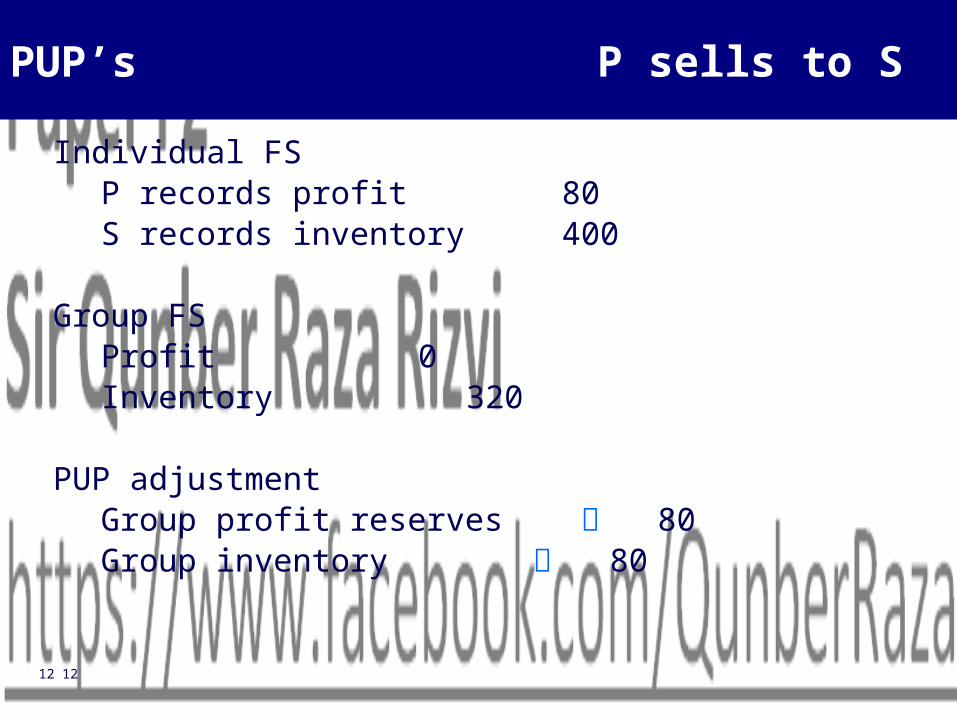

Provisions for Unrealised Profits (PUP’S)

P sells goods to S for $400 at mark-up of 25%. All goods held by S at year-end.

Profit made on sale 25/125 x $400 = $80

12 12

PUP’s P sells to S

Individual FSP records profit 80S records inventory 400

Group FSProfit 0Inventory 320

PUP adjustmentGroup profit reserves 80Group inventory 80

13 13

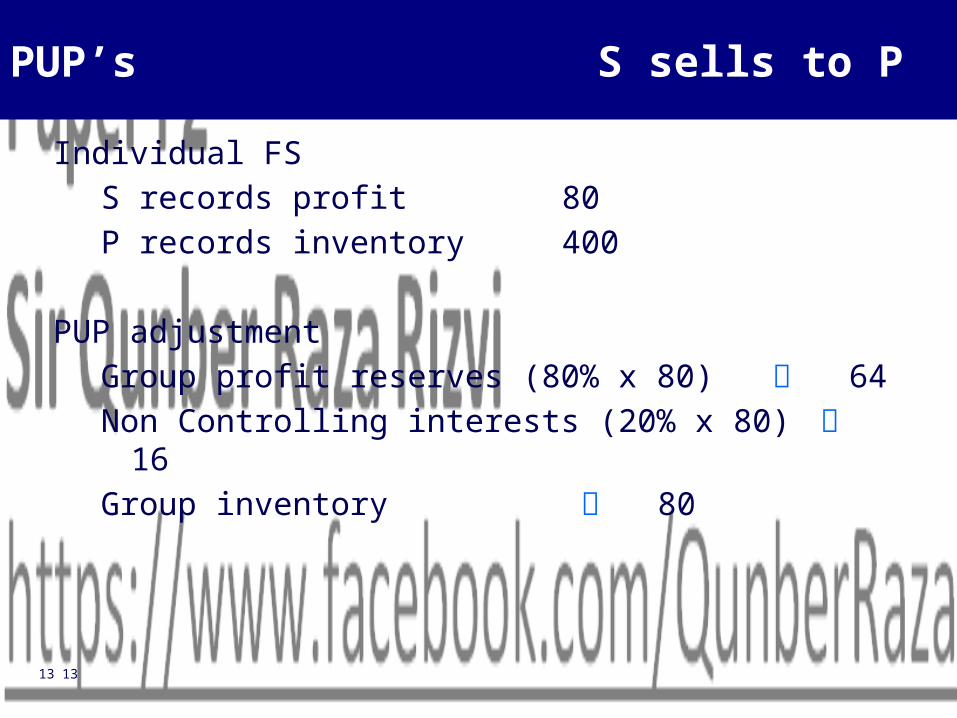

PUP’s S sells to P

Individual FSS records profit 80P records inventory 400

PUP adjustmentGroup profit reserves (80% x 80) 64Non Controlling interests (20% x 80) 16Group inventory 80

14 14

PUP Summary

P Sells to S

Group inventoryGroup reserves

S Sells to P

Group inventoryGroup reserves P%Non controlling

interests NCI%

15 15

2Session Fair Value Adjustments

16 16

Fair Value Adjustments

Fair value of consideration givenCash XShares issued @ FV XDeferred consideration (PV of future CF)XContingent consideration (fair value) XDirectly attributable costs – not included Nil

XP’s share of FV of NA’s of S at DOA (W2) (X)Goodwill – P’s share X

17 17

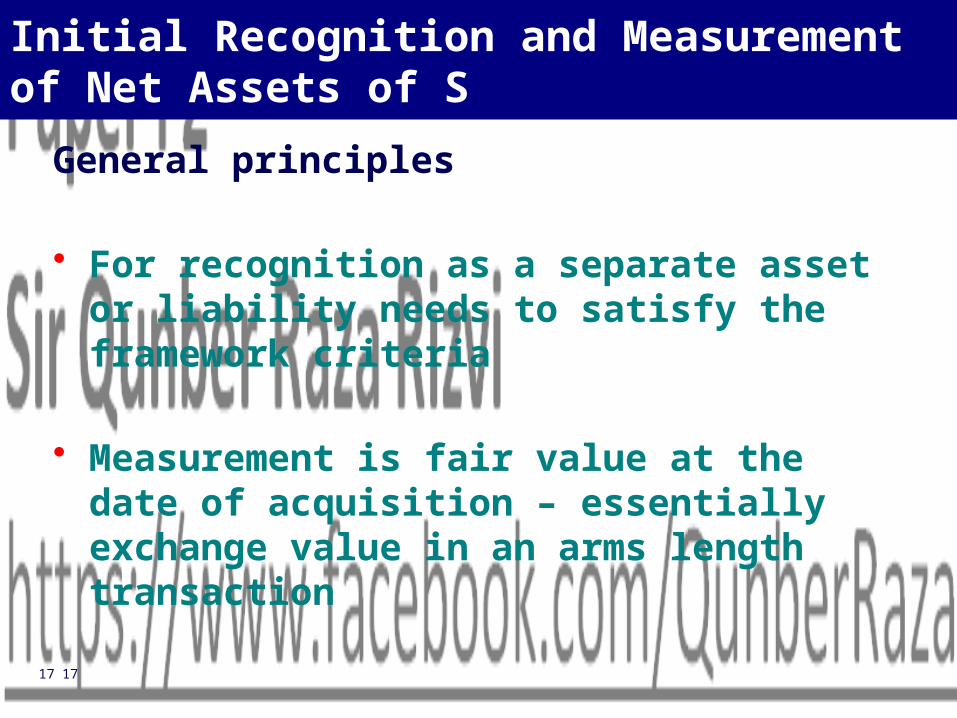

Initial Recognition and Measurement of Net Assets of S

General principles

• For recognition as a separate asset or liability needs to satisfy the framework criteria

• Measurement is fair value at the date of acquisition – essentially exchange value in an arms length transaction

18 18

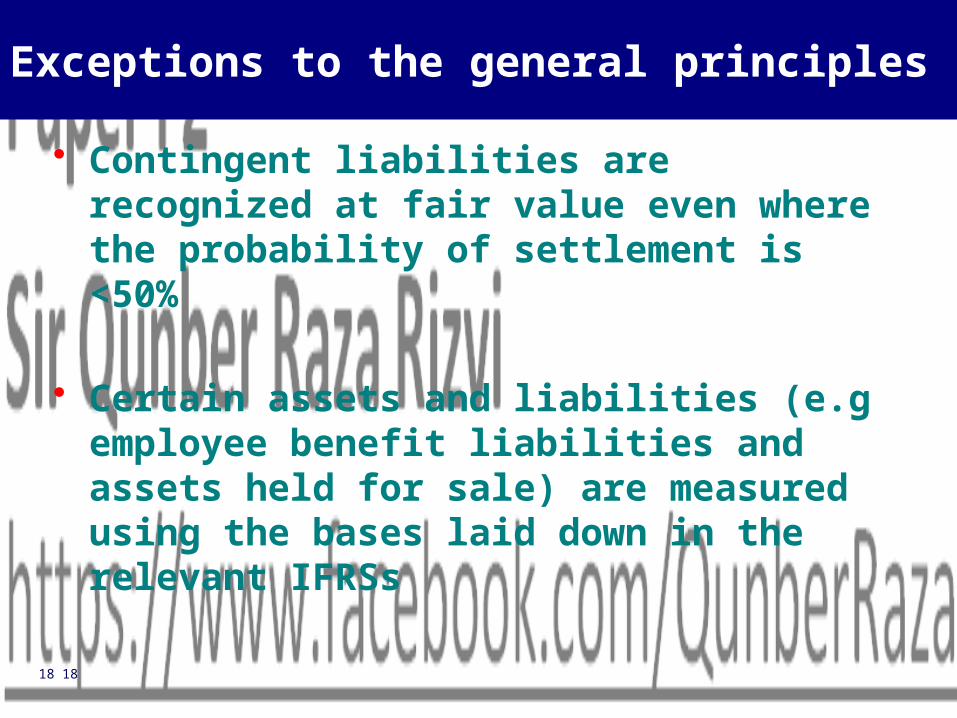

Exceptions to the general principles

• Contingent liabilities are recognized at fair value even where the probability of settlement is <50%

• Certain assets and liabilities (e.g employee benefit liabilities and assets held for sale) are measured using the bases laid down in the relevant IFRSs

19 19

3Session Consolidated Income Statement/Statement of Comprehensive Income

20 20

Consolidated Income Statement

Income Statements

Mid-year acquisitions

Intra Group Transactions

Non-controlling Interest

Fair Value Adjustments

Impairments PUP’s

21 21

4Session Associates and Joint Ventures

22 22

Associates and Joint Ventures

Parent

Subsidiary

ControlSignificant Influence

20-50% Voting Rights

IAS 28 Equity Accounting

Associate

23 23

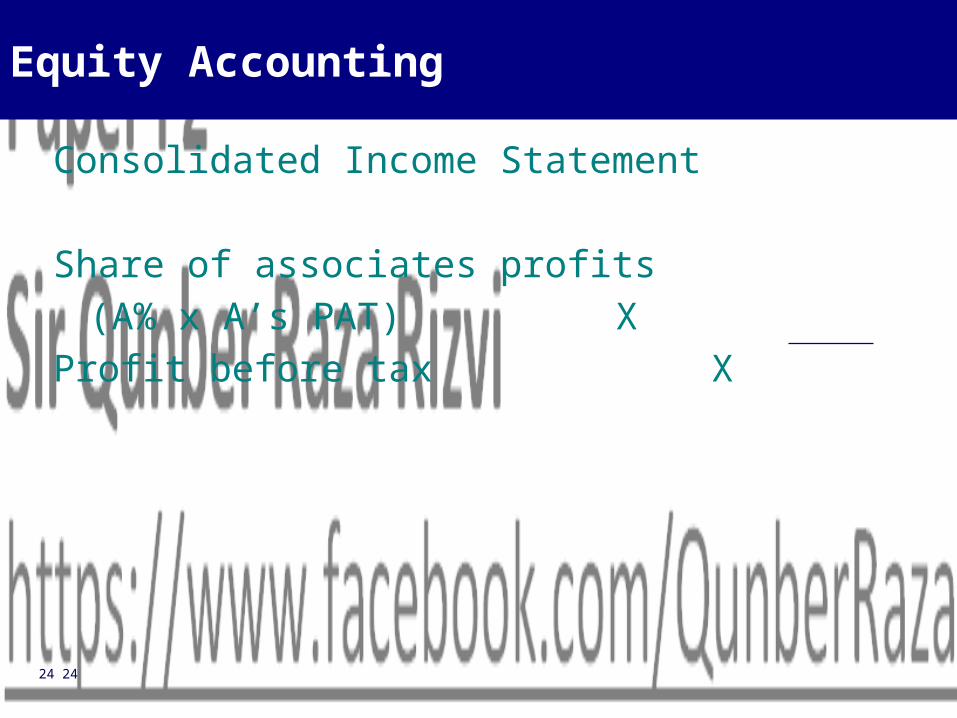

Equity Accounting

Consolidated Statement of Financial Position

Non-current assets Investment in associate Cost of investment X

P’s share of post-acquisition change X in net assets of A Impairment of investment (if any) (X)

X

24 24

Equity Accounting

Consolidated Income Statement

Share of associates profits (A% x A’s PAT) X

Profit before tax X

25 25

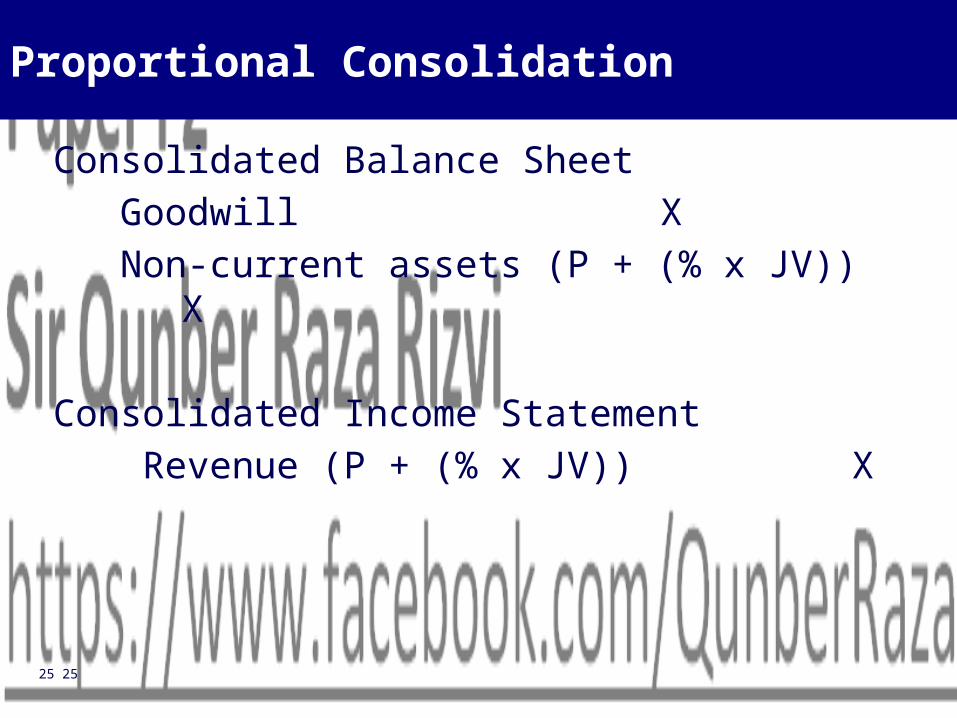

Proportional Consolidation

Consolidated Balance Sheet Goodwill X Non-current assets (P + (% x JV)) X

Consolidated Income Statement Revenue (P + (% x JV)) X

26 26

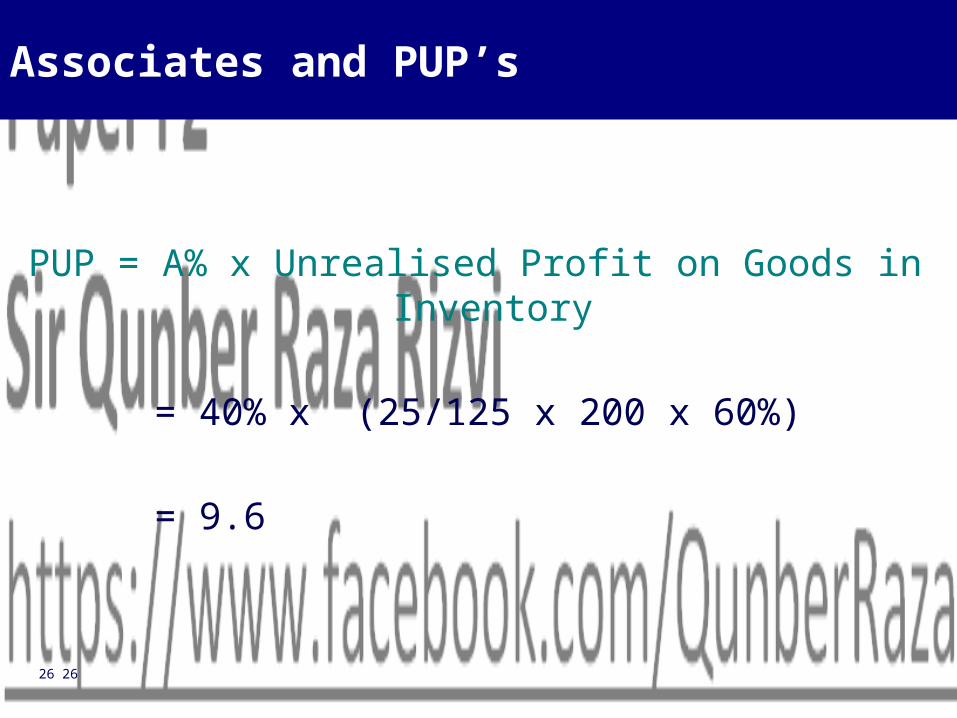

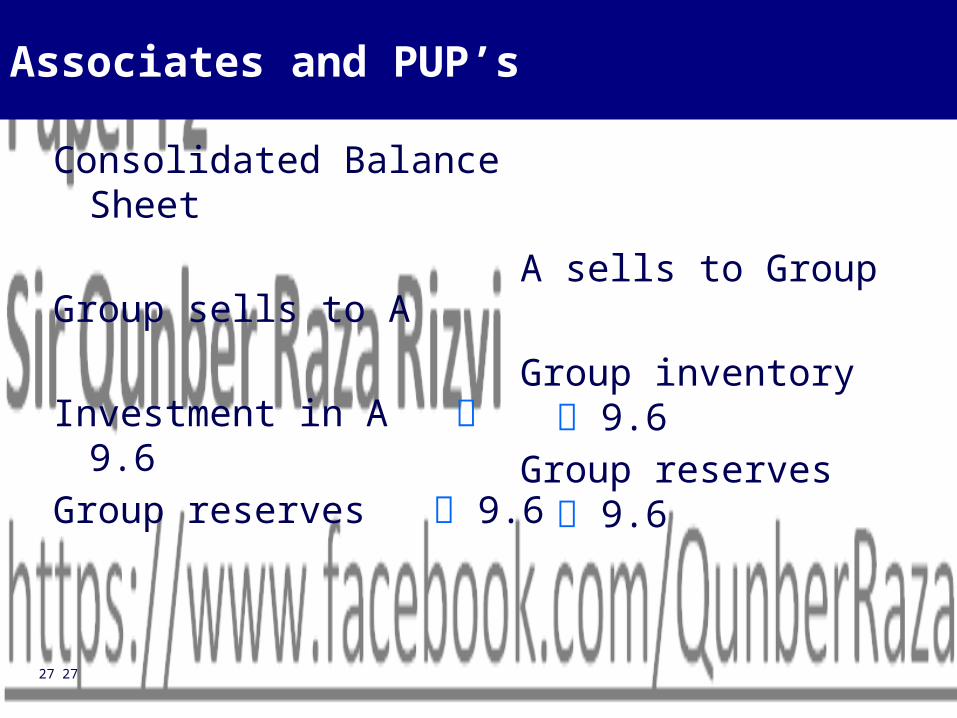

Associates and PUP’s

PUP = A% x Unrealised Profit on Goods in Inventory

= 40% x (25/125 x 200 x 60%)

= 9.6

27 27

Associates and PUP’s

Consolidated Balance Sheet

Group sells to A

Investment in A 9.6 Group reserves 9.6

A sells to Group

Group inventory 9.6Group reserves 9.6

28 28

Associates and PUP’s

Consolidated Income Statement

Group sells to A

Revenue (48) Cost of sales 38.4Gross profit (9.6)

A sells to group

Share of A’s profits (9.6)

29 29

5Session Changes in Group Structure

30 30

Changes in Group Structure

Step-by-step (Piecemeal) Acquisition

Simple Investment

Associate

Subsidiary

31 31

Step by step acquisition – the detail

• Date of acquisition = date control gained

• Re-measure any prior interest in S to FV at DOA – gain or loss to profit and loss

• Include FV of any prior interest as part of ‘cost of investment in S’ for goodwill purposes

32 32

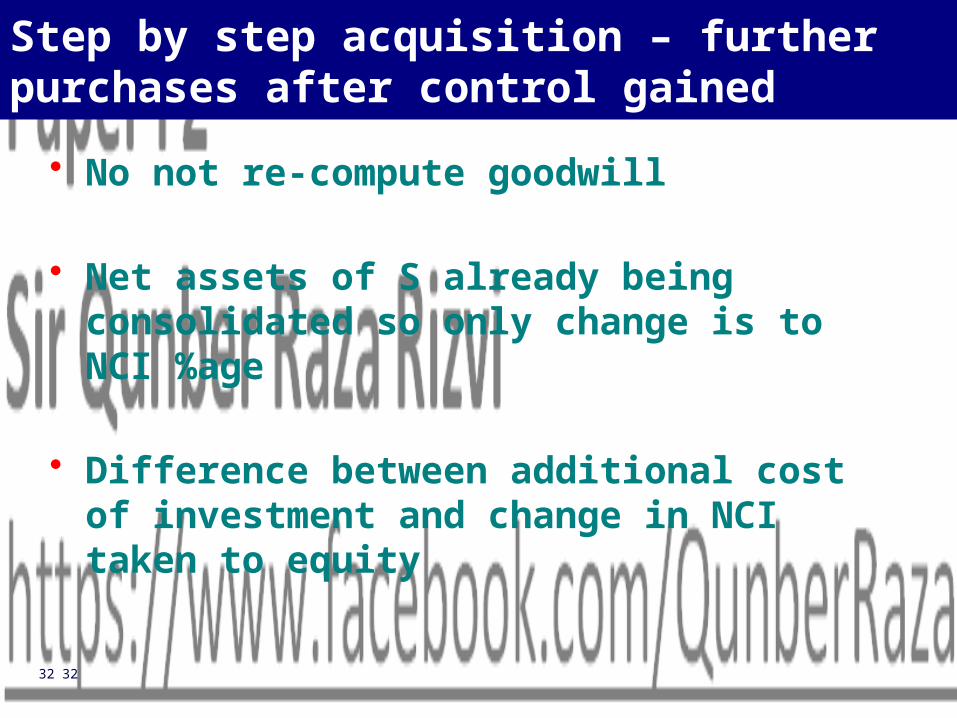

Step by step acquisition – further purchases after control gained

• No not re-compute goodwill

• Net assets of S already being consolidated so only change is to NCI %age

• Difference between additional cost of investment and change in NCI taken to equity

33 33

Changes in Group Structure

Disposal of Subsidiary – Loss of control

Proceeds XFV of retained interest (if any) XNA of S at disposal (X)Goodwill of S at disposal (X)NCI in S no longer recognized XGain/Loss for group X

34 34

Changes in Group Structure

• Disposal of Subsidiary – no loss of control

• No change to goodwill recognized

• NA of S still consolidated

• NCI in S increases

• Difference between disposal proceeds and increase in NCI taken to equity

35 35

6Session Complex Groups

36 36

Complex Groups

Vertical Group

Parent

Subsidiary

Sub-Subsidiary

Controls

Controls

37 37

Vertical Group

P

S80%

80%Q

38 38

Vertical Group

P

S60%

60%Q

39 39

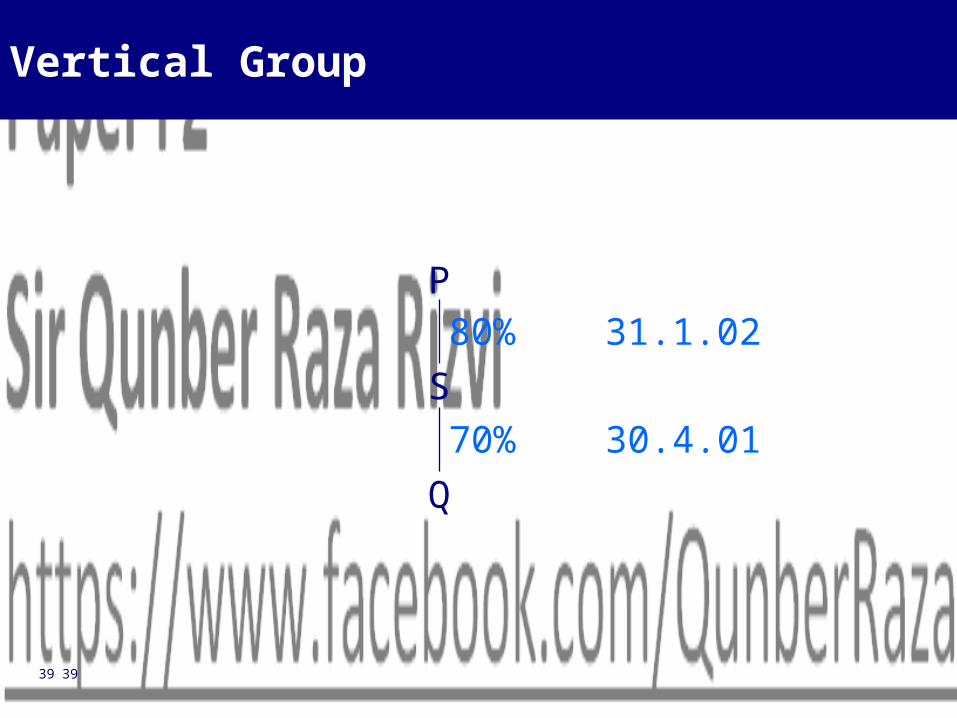

Vertical Group

P

S80% 31.1.02

70% 30.4.01Q

40 40

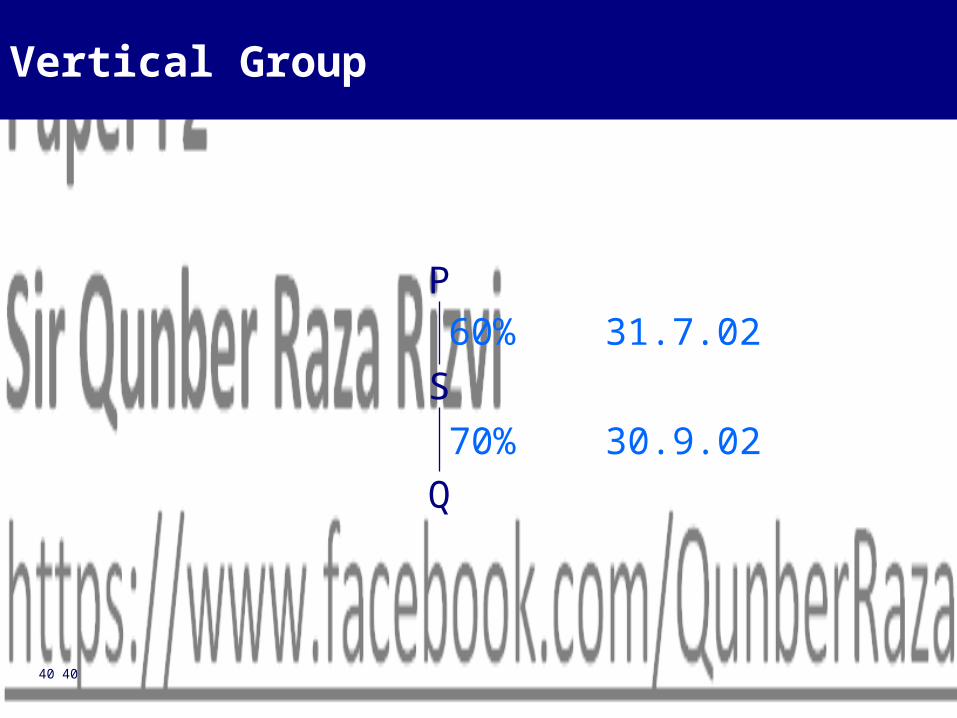

Vertical Group

P

S60% 31.7.02

70% 30.9.02Q

41 41

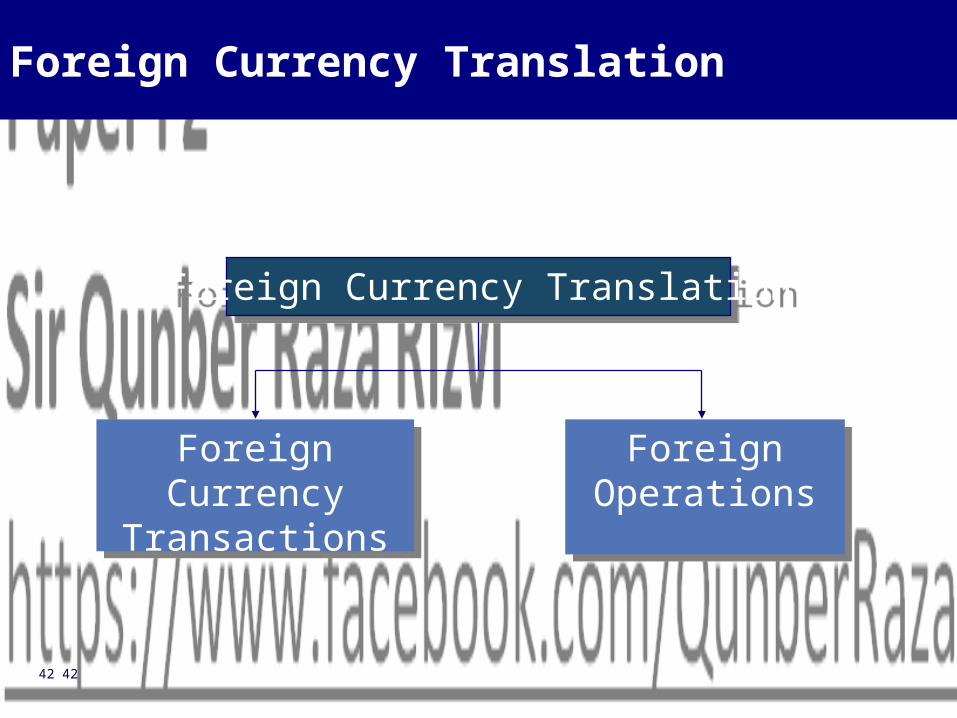

7Session Foreign Currency Translation

42 42

Foreign Currency Translation

Foreign Currency Translation

Foreign Currency Transactions

Foreign Operations

43 43

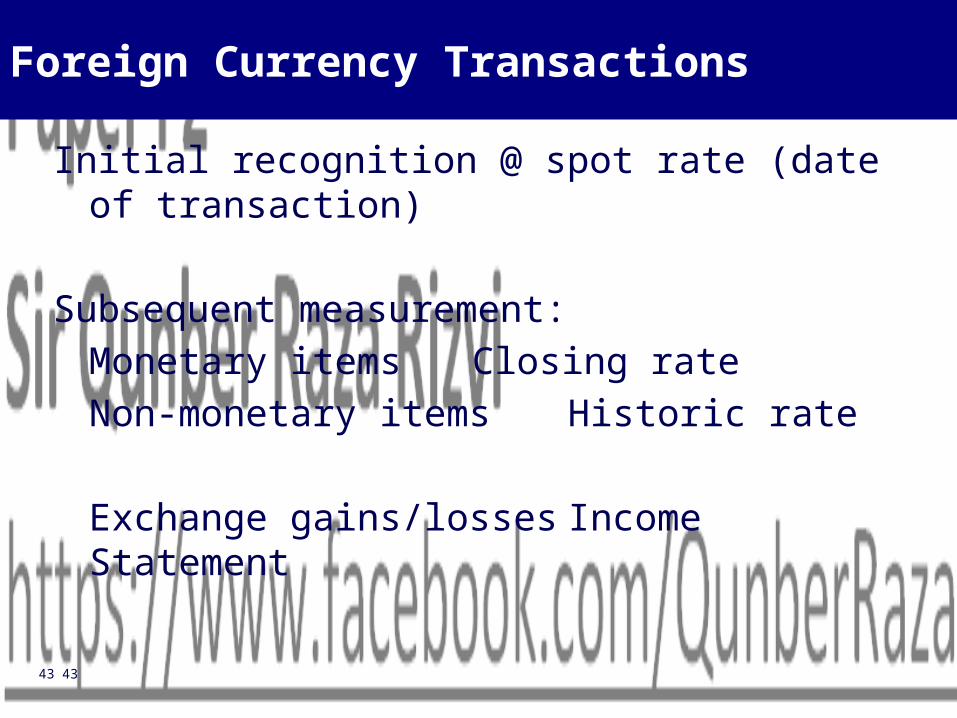

Foreign Currency Transactions

Initial recognition @ spot rate (date of transaction)

Subsequent measurement:Monetary items Closing rateNon-monetary items Historic rate

Exchange gains/lossesIncome Statement

44 44

Closing Rate Method

Translation of foreign operation:

Balance Sheet Closing Rate

Income Statement Average Rate

Exchange gains/losses Other comprehensive income

45 45

Breakdown of exchange gains/losses

Since acquisition:

Sub’s NA’s @ acq’n acq’n rate v. cl rate

Post-acq profits av. rate v. cl. rate

Goodwill acq’n rate v. cl. rate

46 46

Breakdown of exchange gains/losses

For year:

Sub’s NA’s @ Op. Op. rate v. cl rate

Profit for yr av. rate v. cl. rate

Goodwill Op. rate v. cl. rate

47 47

8Session Group Statements of Cash Flow

48 48

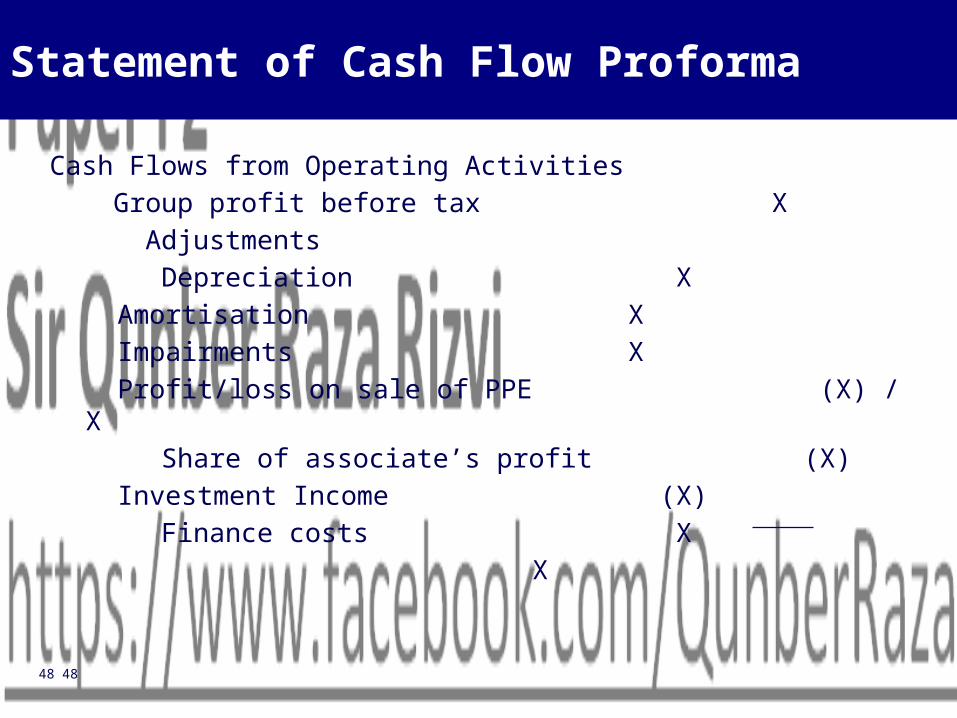

Statement of Cash Flow Proforma

Cash Flows from Operating Activities Group profit before tax X Adjustments Depreciation X

Amortisation X Impairments X Profit/loss on sale of PPE (X) / X

Share of associate’s profit (X) Investment Income (X) Finance costs X

X

49 49

Statement of Cash Flow Proforma

XChange in inventory (X)/XChange in receivables (X)/XChange in payables X/(X)Cash generated from operations XInterest paid (X)Tax paid (X)Net cash from operating activities X

50 50

Statement of Cash Flow Proforma

Cash Flows from Investing ActivitiesSale proceeds from disposal of PPE XPurchases of PPE (X)Interest received XDividends received from Associate XAcq’n/Sale of Sub, net of cash balances (X) / X

X

51 51

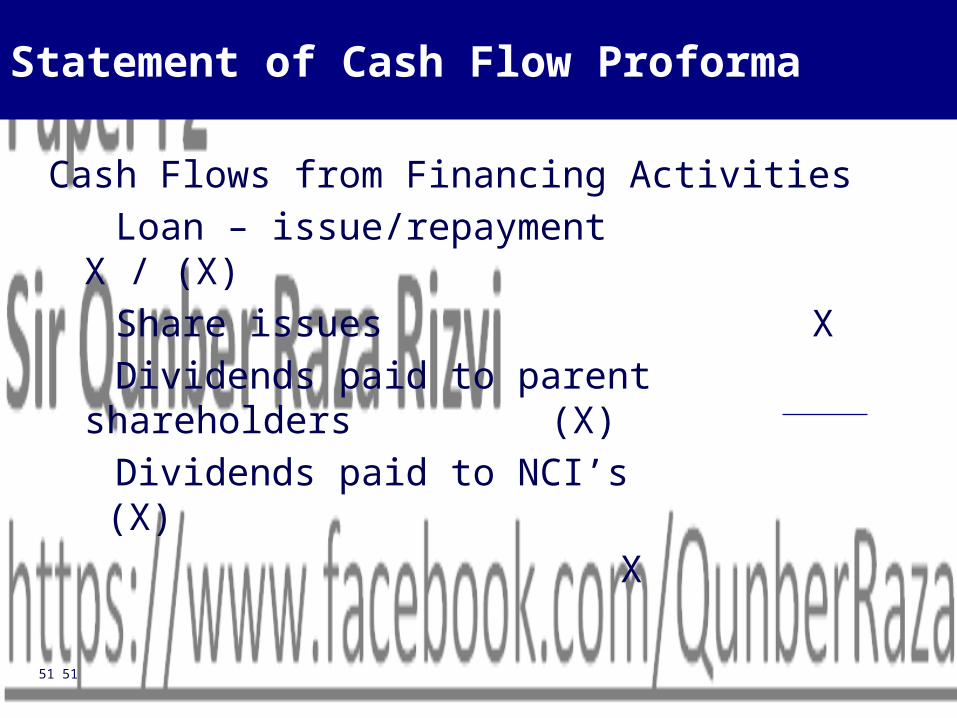

Statement of Cash Flow Proforma

Cash Flows from Financing Activities Loan – issue/repayment X /

(X) Share issues X Dividends paid to parent shareholders (X) Dividends paid to NCI’s (X)

X

52 52

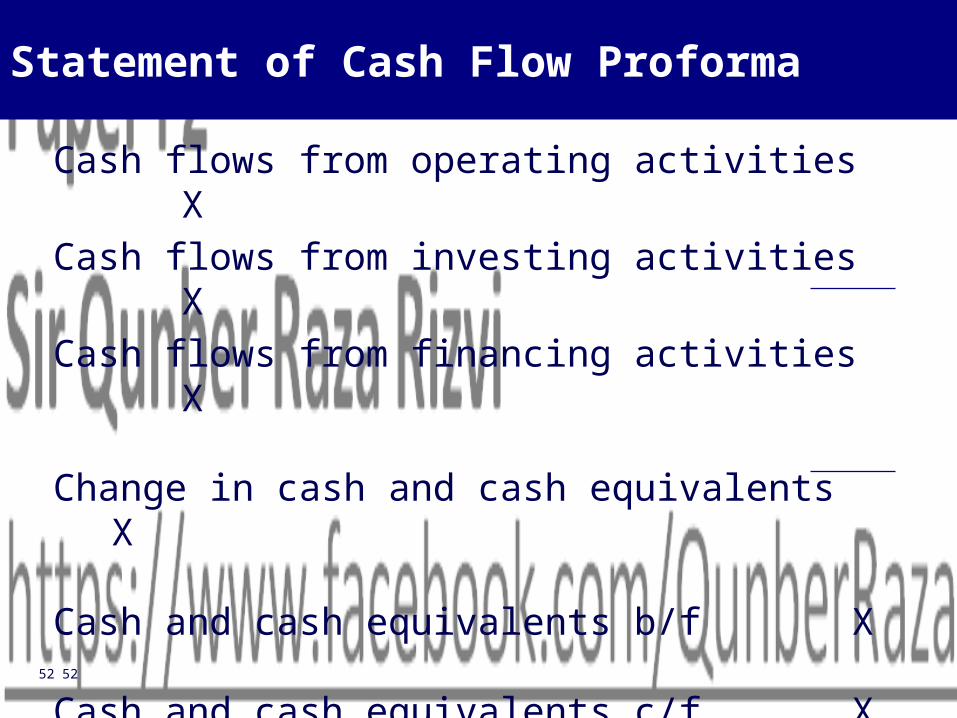

Statement of Cash Flow Proforma

Cash flows from operating activities XCash flows from investing activities XCash flows from financing activities X

Change in cash and cash equivalents X

Cash and cash equivalents b/f X

Cash and cash equivalents c/f X

53 53

9Session Accounting for Employee Benefits

54 54

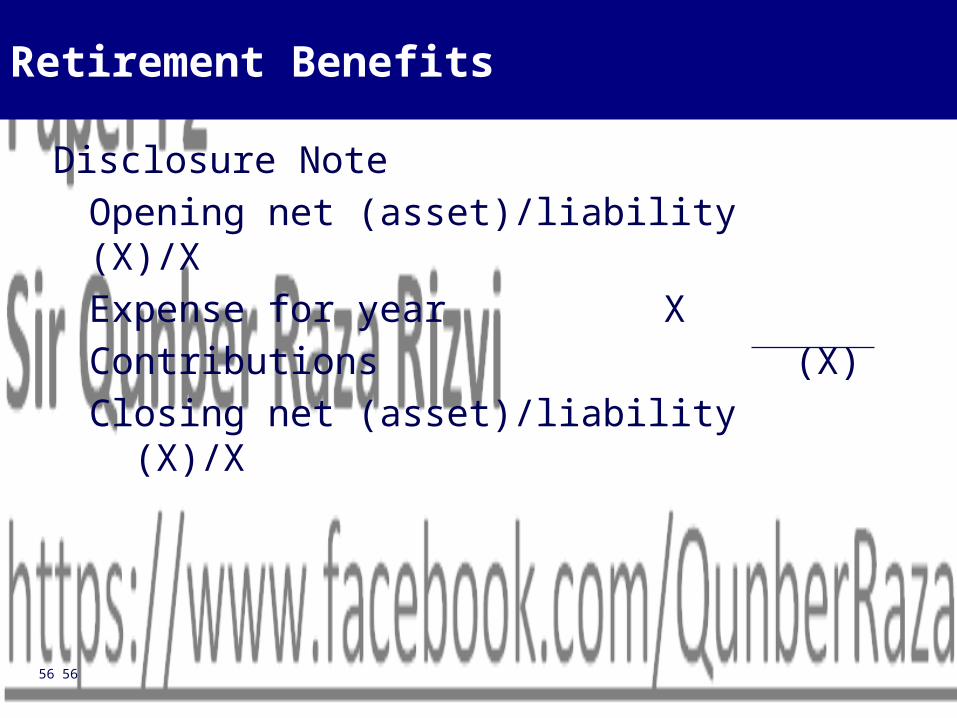

Retirement Benefits

Statement of Financial Position Present value of obligation X Fair value of plan assets

(X)

XUnrecognised actuarial gains/(losses) XNet (asset)/liability X

55 55

Retirement Benefits

Income StatementCurrent service costs XInterest cost XCurtailment costs XExpected return on plan assets (X)Net actuarial (gain)/loss (X)/XExpense X

56 56

Retirement Benefits

Disclosure NoteOpening net (asset)/liability (X)/XExpense for year XContributions (X)Closing net (asset)/liability (X)/X

57 57

Retirement Benefits

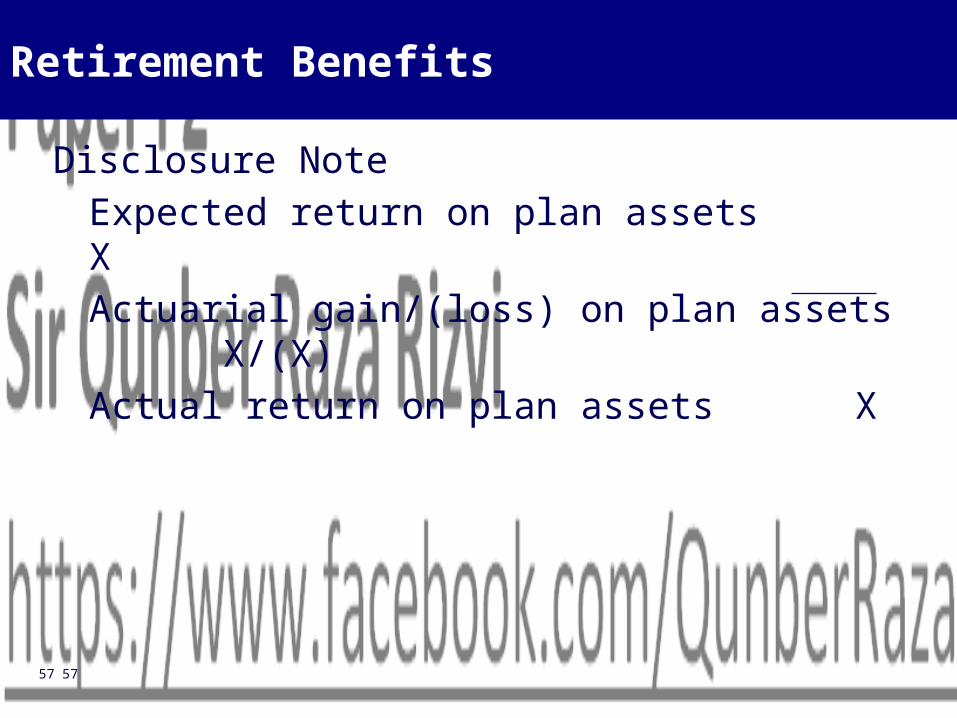

Disclosure NoteExpected return on plan assets XActuarial gain/(loss) on plan assets X/(X)Actual return on plan assets X

58 58

10Session Substance Over Form

59 59

Factored Receivables

Transfer of Risks and Benefits

None Some

ReceivablesRemain

ReceivablesRemain

ReceivablesRemoved

Cash Inflow = Loan

Cash Inflow = Loan

Cash Inflow = Proceeds

Liability Liability Gain (Loss) in Income Statement

All

60 60

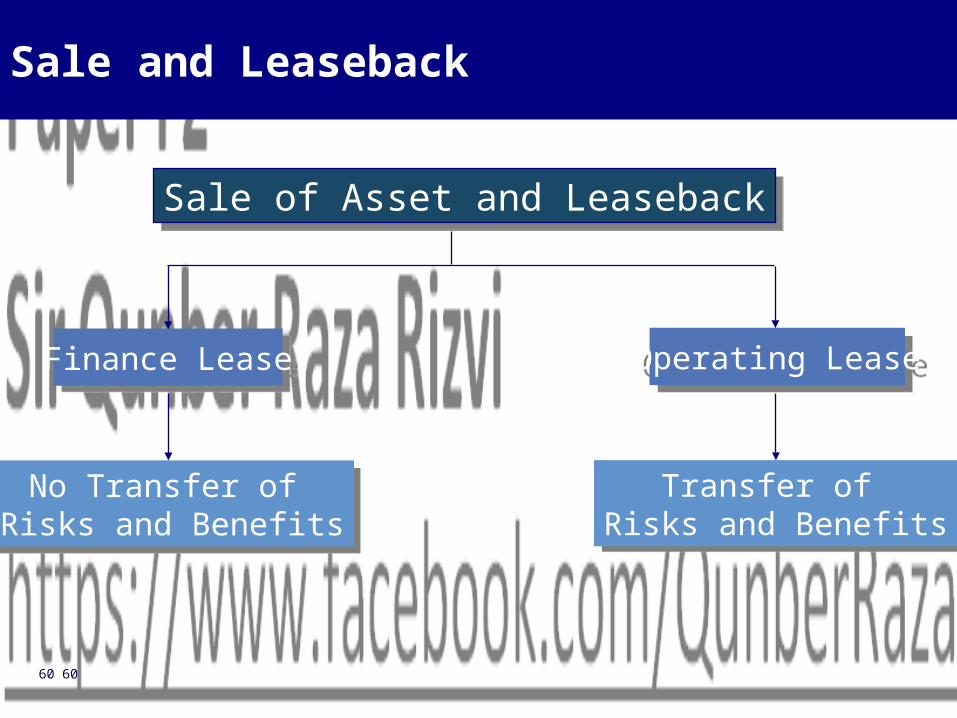

Sale and Leaseback

Sale of Asset and Leaseback

Finance Lease

No Transfer of Risks and Benefits

Transfer of Risks and Benefits

Operating Lease

61 61

11Session Financial Instruments

62 62

Financial Instruments

Definition – IAS 32

Any contract that gives rise to both a financial assets of one entity and a financial liability or equity instrument of another entity.

63 63

Financial Asset

• Cash• Right to receive cash• Equity

64 64

Financial Liability

• Contractual obligation to deliver cash

65 65

Equity Instrument

• Evidence of ownership

66 66

Classification of Financial Instruments

Equity or Liability?• Substance• Responsibility to deliver cash = liability• Mandatory redemption = liability• No responsibility to deliver cash = equity

67 67

12Session Analysis and Interpretation of Financial Accounts

68 68

Performance

Profitability x Efficiency =Returns

GP%

OP% x Asset utilisation =ROCE

NP%

69 69

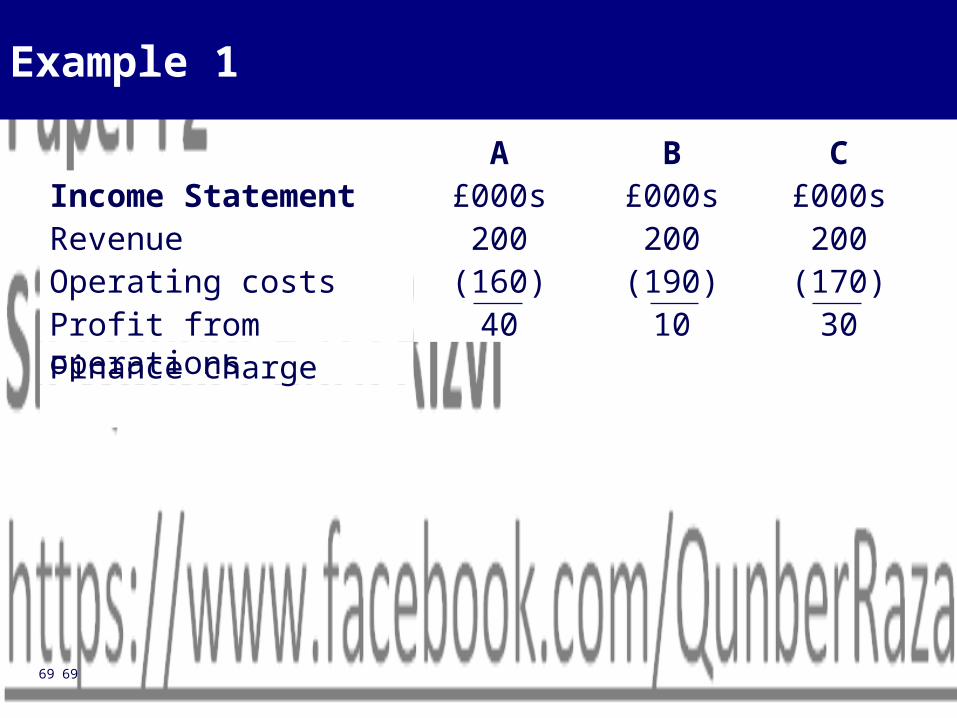

Example 1

Finance charge301040Profit from operations

(170)(190)(160)Operating costs200200200Revenue

£000s£000s£000sIncome StatementCBA

70 70

Example 1

100320140Capital employedFinance lease payable

210Revaluation reserve506090Retained earnings505050Share capital

Statement of Financial Position

CBA

71 71

30%3.1%28.6%Return on capital employed

20.631.43Asset utilisation

15%5%20%Operating profit margin

CBA

Example 1

72 72

Liquidity

Payables Days

Buy Goods

Sell Goods

Cash In Cash Out

InventoryDays

ReceivableDays

73 73

Capital Structure

Equity

Debt

High Gearing Low Interest Cover

74 74

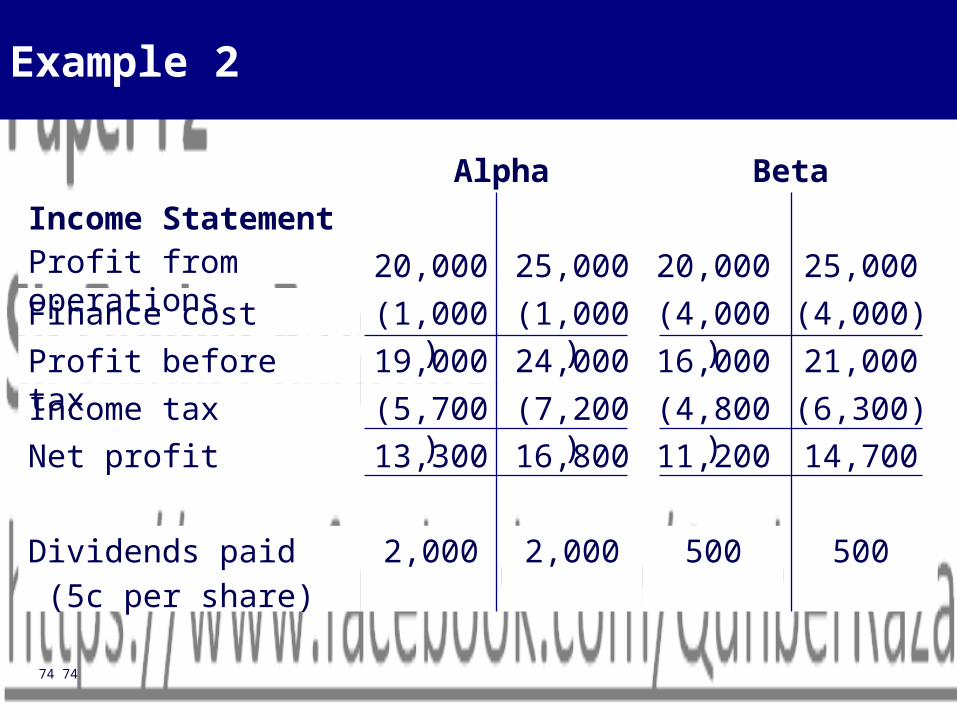

Example 2

500

14,700(6,300)21,000(4,000)25,000

5002,0002,000Dividends paid (5c per share)

11,20016,80013,300Net profit(4,800)(7,200)(5,700)Income tax16,00024,00019,000Profit before tax(4,000)(1,000)(1,000)Finance cost 20,00025,00020,000Profit from operations

Income StatementBetaAlpha

75 75

Example 2

103,50053,500

10,00040,000

100,000103,500100,000Capital employed50,00053,50050,000Reserves

10,00040,00040,000Share capital £1 ordinary shares

40,00010,00010,00010% loan notesStatements of FP

BetaAlpha

76 76

Example 2

Alpha is more highly geared then Beta, but both companies have the same amount of capital employed in total and generate the same returns overall:

Gearing 10% 40%ROCE 20% 20%

BetaAlpha

77 77

Example 2

If there is a 25% increase in the profits of both companies however, the shareholders of Beta benefit more than the shareholder of Alpha:

Return on equity 14.7% 18.0% 18.6% 23.1%+22.4%

+24.2%

EPS 33.25c 42c 112c147c

+26.3%+31.25%

BetaAlpha

78 78

Preparing a Report

To

From

Date

Subject

79 79

Preparing a Report

Introduction

Discussion

Conclusion

80 80

Limitations of Ratio Analysis

• Financial statements• Comparisons of different entities• Ratios• Creative accounting

81 81

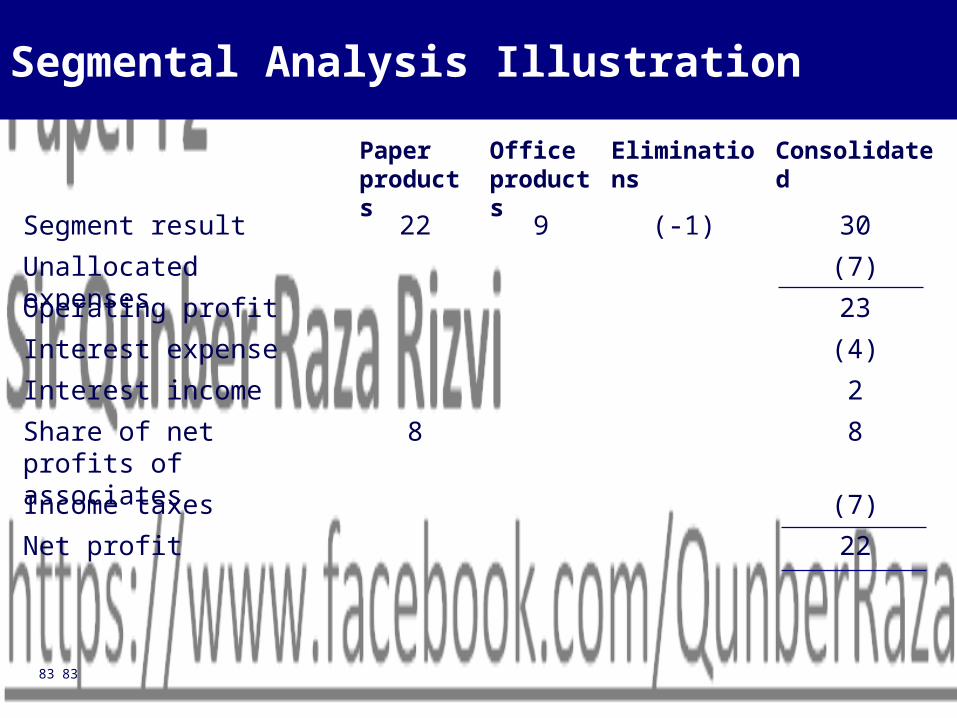

Segmental Analysis

• IFRS 8 requires for listed companies only

• Analysis based on internal information provided to senior management

• Separately analysed segments are those parts of the business whose results are material and whose risk characteristics are distinctive

82 82

Segmental Analysis - Illustration

101(29)3991Total revenue

(29)1217Inter-segment sales

2774External sales

Revenue

ConsolidatedEliminationsOffice products

Paper products

83 83

Segmental Analysis Illustration

30(-1)922Segment result(7)Unallocated expenses23Operating profit(4)Interest expense2Interest income88Share of net profits of

associates(7)Income taxes22Net profit

ConsolidatedEliminationsOffice products

Paper products

84 84

Segmental Analysis Illustration

1084464Segment assets3232Investments in associates 35Un-allocated assets175Total assets

42933 Segment liabilities 40 Un-allocated liabilities82 Total liabilities

ConsolidatedEliminationsOffice products

Paper products

85 85

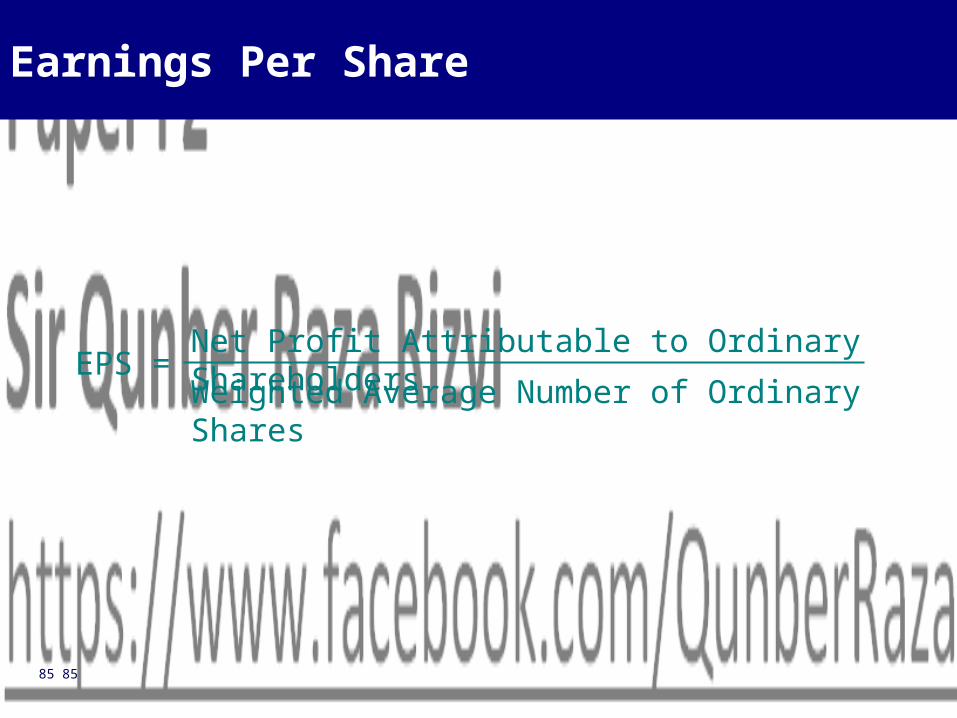

Earnings Per Share

EPS =Net Profit Attributable to Ordinary ShareholdersWeighted Average Number of Ordinary Shares

86 86

Issue of Shares at Market Value

EPS = Earnings(No. Shares Before x ?/12) + (No. Shares After x ?/12)

87 87

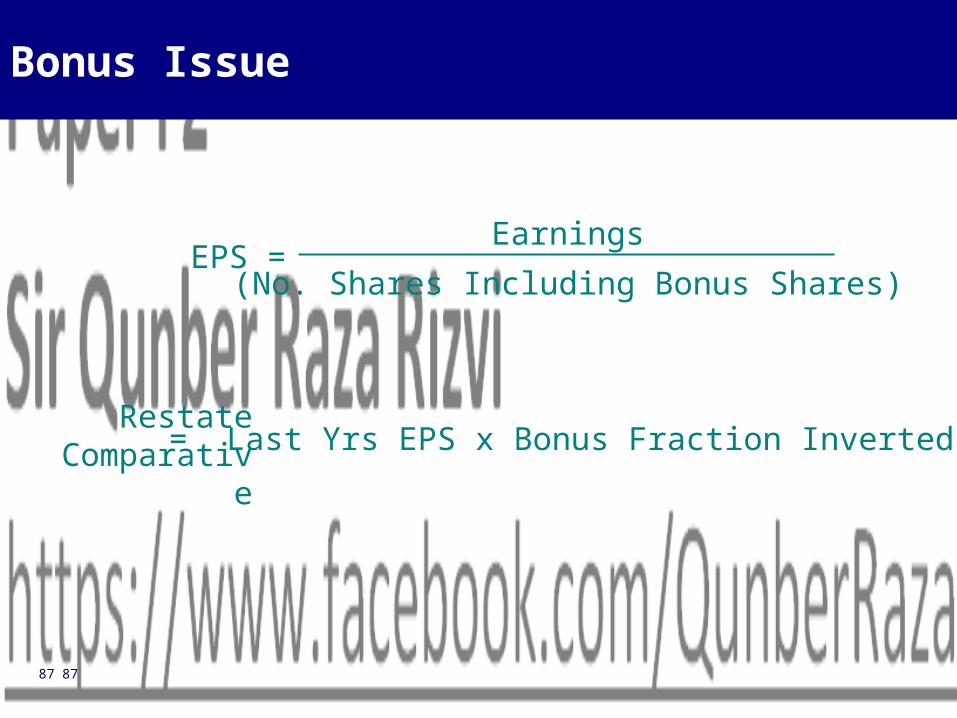

Bonus Issue

EPS =

Restate Comparative = Last Yrs EPS x Bonus Fraction Inverted

Earnings(No. Shares Including Bonus Shares)

88 88

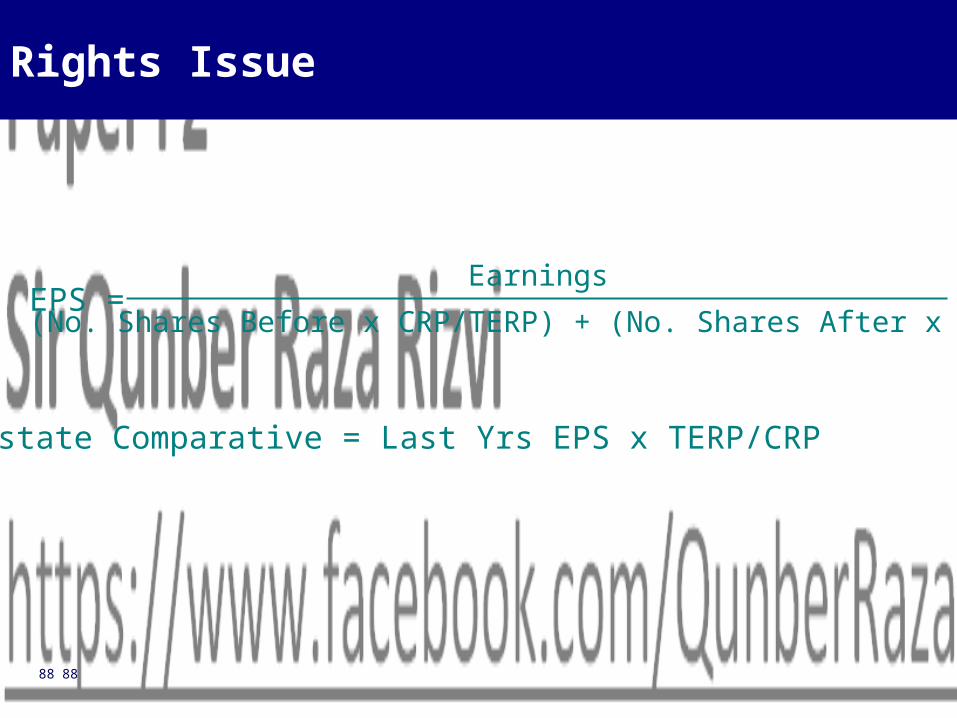

Rights Issue

Restate Comparative = Last Yrs EPS x TERP/CRP

EPS =Earnings

(No. Shares Before x CRP/TERP) + (No. Shares After x ?/12)

89 89

Diluted Earnings Per Share

Options x (FV-Ex) FV

NilOptions

Increase by maximum

+ Preference dividends

Convertible preference shares

Increase by maximum

+ Interest – TaxConvertible debt

No. of Shares AdjEarnings AdjPotential Ordinary Share

90 90

13Session Developments in External Reporting

91 91

Syllabus Content Diagram

Developments in External

Reporting

Non-Financial Environmental and Social Reporting

International Financial Reporting