Perspectivas de la Industria Automotriz PERUaap.org.pe/descarga/ea2017/Presentacion-Guido... ·...

33

© 2017 IHS Markit. All Rights Reserved. © 2017 IHS Markit. All Rights Reserved. Perspectivas de la Industria Automotriz PERU Diciembre, 2017 Guido Vildozo | Senior Manager, Americas +1 781 301 9037, [email protected]

Transcript of Perspectivas de la Industria Automotriz PERUaap.org.pe/descarga/ea2017/Presentacion-Guido... ·...

© 2017 IHS Markit. All Rights Reserved.© 2017 IHS Markit. All Rights Reserved.

Perspectivas de la Industria AutomotrizPERUDiciembre, 2017

Guido Vildozo | Senior Manager, Americas

+1 781 301 9037, [email protected]

© 2017 IHS Markit. All Rights Reserved.

Enfrentado retos del futuro al conectar industrias criticas globales.

MateriasPrimas

Finanzas

Tecnologia yEspecificaciones

TransporteOPERATIONAL RISK

& REGULATORY COMPLIANCE

DIGITAL & WEB SOLUTIONS

MARITIME & TRADE

AEROSPACE,DEFENSE &SECURITY

AUTOMOTIVEENGINEERING &

PRODUCT DESIGN

ECONOMICS & COUNTRY RISKENERGY

CHEMICALFINANCIAL

MARKETS DATA& SERVICES

TECHNOLOGY,MEDIA &TELECOM

© 2016 IHS Markit© 2016 IHS Markit© 2016 IHS Markit – All Rights Reserved

© 2017 IHS Markit. All Rights Reserved.

IHS Markit es un socio estratégico al éxito de nuestros clientes

▪ Nuestra lista de clientes incluye:

▪ Las 20 empresas automotrices mas grandes

▪ 92 de los top 100 Proveedores Tier-1

▪ Cobertura del parque para mas de 1,000 millones de vehículos

▪ 650 clientes automotrices que representan 85% de la industria

© 2016 IHS Markit – All Rights Reserved

Contents

© 2016 IHS Markit

SOCIMÓNOCE SERODACIDNI

AL ED LABOLG AVITCEPSREP INDUSTRIA AUTOMOTRIZ

NOICAZIROTOM NE SOIBMAC

AIRTSUDNI AL ED AVITCEPSREP AUTOMOTRIZ EN AMÉRICA LATINA

SATNEV ED AVITCEPSREP AUTOMOTRICES PARA EL MERCADO PERUANO

NEMUSER

4

© 2017 IHS Markit. All Rights Reserved.

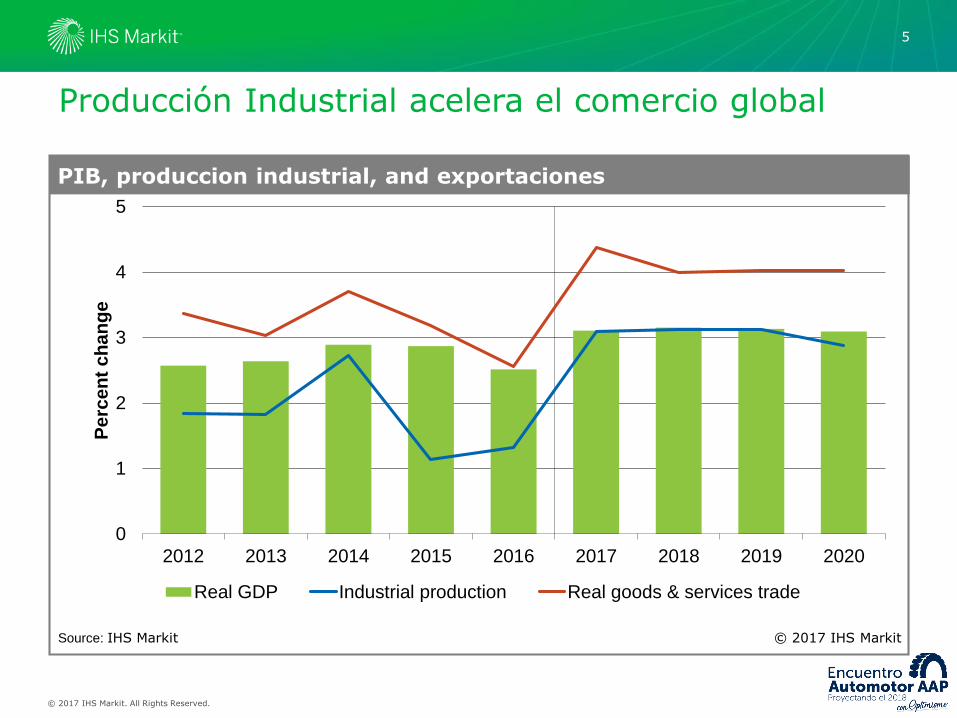

0

1

2

3

4

5

2012 2013 2014 2015 2016 2017 2018 2019 2020

Pe

rce

nt

ch

an

ge

Real GDP Industrial production Real goods & services trade

Producción Industrial acelera el comercio global

PIB, produccion industrial, and exportaciones

Source: IHS Markit © 2017 IHS Markit

5

© 2017 IHS Markit. All Rights Reserved.

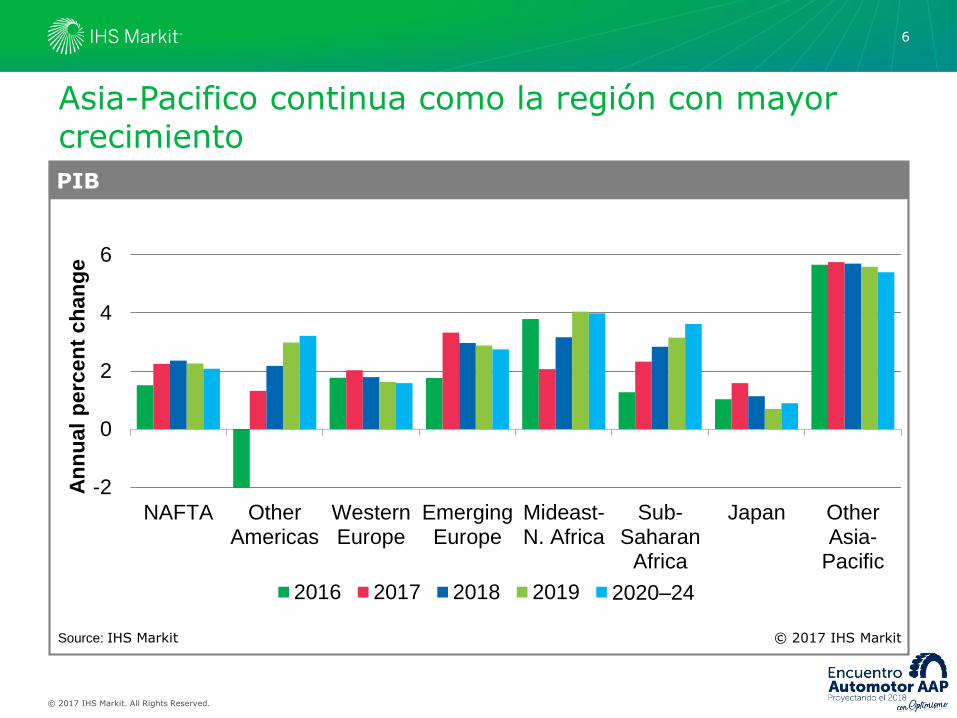

-2

0

2

4

6

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

An

nu

al

perc

en

t ch

an

ge

2016 2017 2018 2019 2020–24

Asia-Pacifico continua como la región con mayor crecimiento

PIB

Source: IHS Markit © 2017 IHS Markit

6

© 2017 IHS Markit. All Rights Reserved.

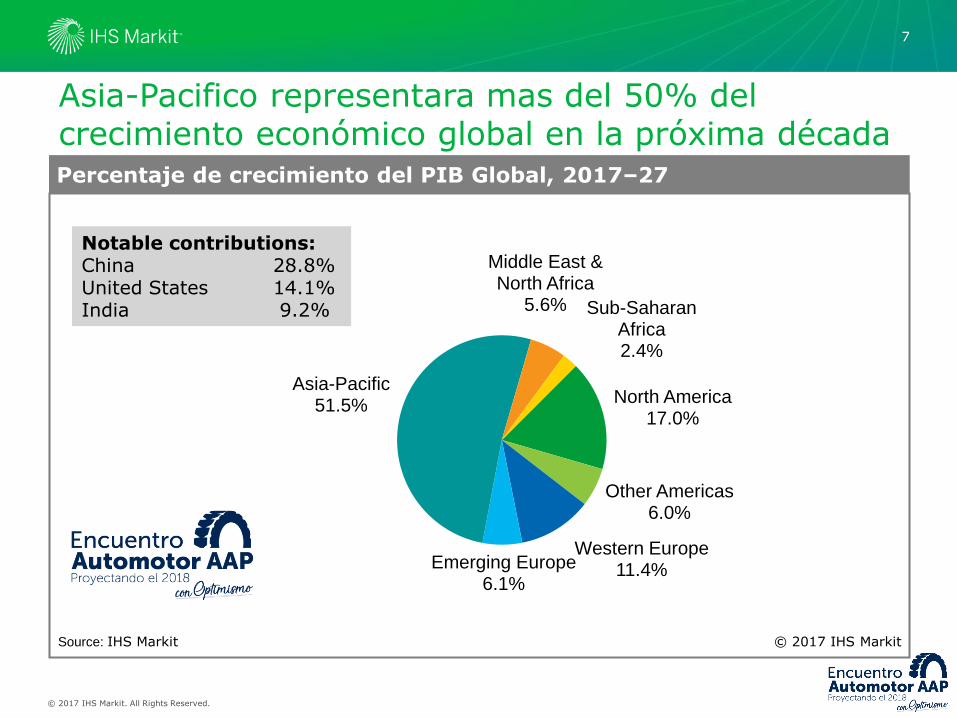

North America17.0%

Other Americas6.0%

Western Europe11.4%Emerging Europe

6.1%

Asia-Pacific51.5%

Middle East & North Africa

5.6% Sub-Saharan Africa2.4%

Asia-Pacifico representara mas del 50% del crecimiento económico global en la próxima décadaPercentaje de crecimiento del PIB Global, 2017–27

Source: IHS Markit © 2017 IHS Markit

Notable contributions:China 28.8%United States 14.1%India 9.2%

7

© 2017 IHS Markit. All Rights Reserved.

30

35

40

45

50

55

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Ind

ex, o

ver

50 s

ign

als

exp

an

sio

n

United States Eurozone China Japan

IHS Markit Índices de Manufactura Global refleja una onda expansivaPurchasing managers’ indexes

Source: IHS Markit © 2017 IHS Markit

8

© 2017 IHS Markit. All Rights Reserved.

IHS Markit Índice de Precios de Materias Primas llevan dos años de crecimiento

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

All industrial materials Chemicals Nonferrous metals

IH

S M

arkit

weekly

in

dexes, 2

00

2:1

=1

IHS Markit Materials Price Index

Source: IHS Markit © 2017 IHS Markit

9

© 2017 IHS Markit. All Rights Reserved.

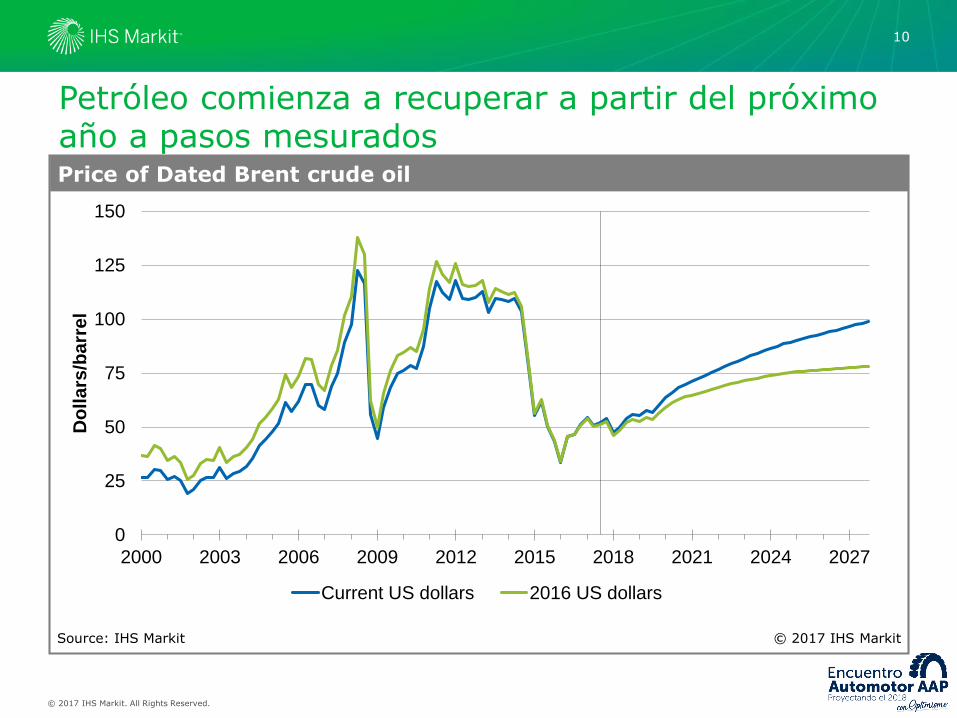

Petróleo comienza a recuperar a partir del próximo año a pasos mesurados

0

25

50

75

100

125

150

2000 2003 2006 2009 2012 2015 2018 2021 2024 2027

Do

lla

rs/b

arr

el

Current US dollars 2016 US dollars

Price of Dated Brent crude oil

Source: IHS Markit © 2017 IHS Markit

10

© 2017 IHS Markit. All Rights Reserved.

Bolsas de Valores con tendencia a la alza

Equity prices, percent change

-20 -10 0 10 20 30

China (SSEA)

Eurozone (FTSE Euro 100)

Japan (Nikkei 225)

World, developed* (MSCI)

Emerging markets* (MSCI)

United States (S&P 500)

United Kingdom (FTSE 100)

Canada (S&P TSX)

2017 year to date (to 11 October) 2016 2015

* In US dollarsSource: The Economist © 2017 IHS Markit

11

© 2017 IHS Markit. All Rights Reserved.

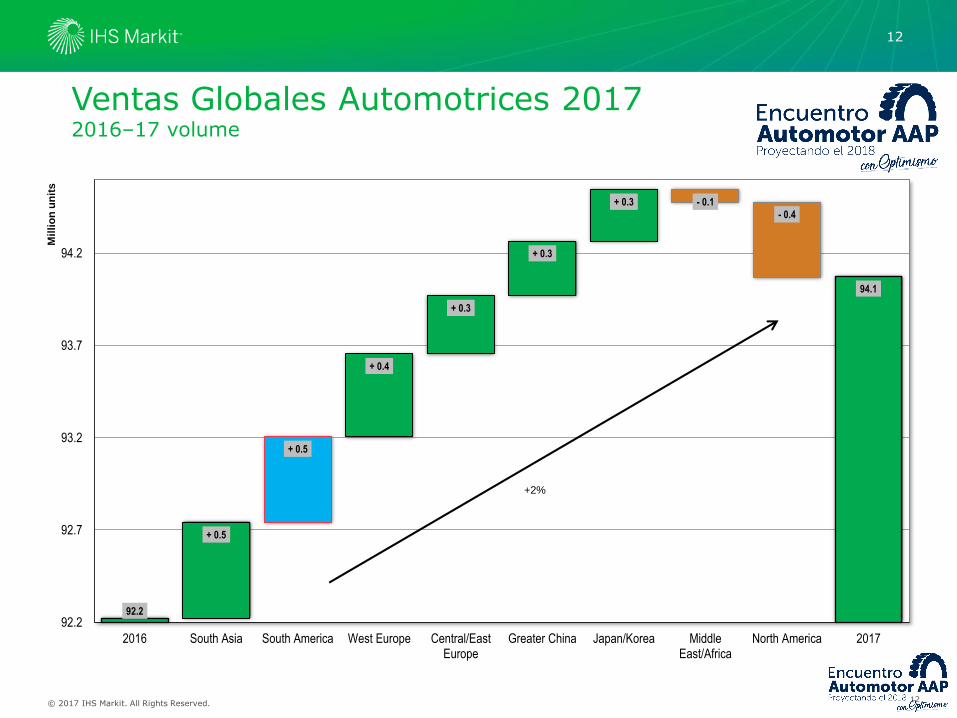

Ventas Globales Automotrices 20172016–17 volume

12

92.2

94.1

+ 0.5

+ 0.5

+ 0.4

+ 0.3

+ 0.3

+ 0.3 - 0.1

- 0.4

92.2

92.7

93.2

93.7

94.2

2016 South Asia South America West Europe Central/EastEurope

Greater China Japan/Korea MiddleEast/Africa

North America 2017

Mil

lio

n u

nit

s

+2%

12

© 2017 IHS Markit. All Rights Reserved.

64

93

108

50

60

70

80

90

100

110

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Global Light Vehicle Sales (Millions)

Source: IHS Markit © 2017 IHS

29million

15million

94

-0.4-0.20.0

0.00.10.40.40.91.2

2.69.3

-2.00.02.04.06.08.010.0

MPV

Wagon

Convertible

Roadster

Coupe

Van

Chassis-Cab

Pickup

Sedan

Hatchback

SUV

Ventas globales se aproximan a 100 millones

13

© 2017 IHS Markit. All Rights Reserved.

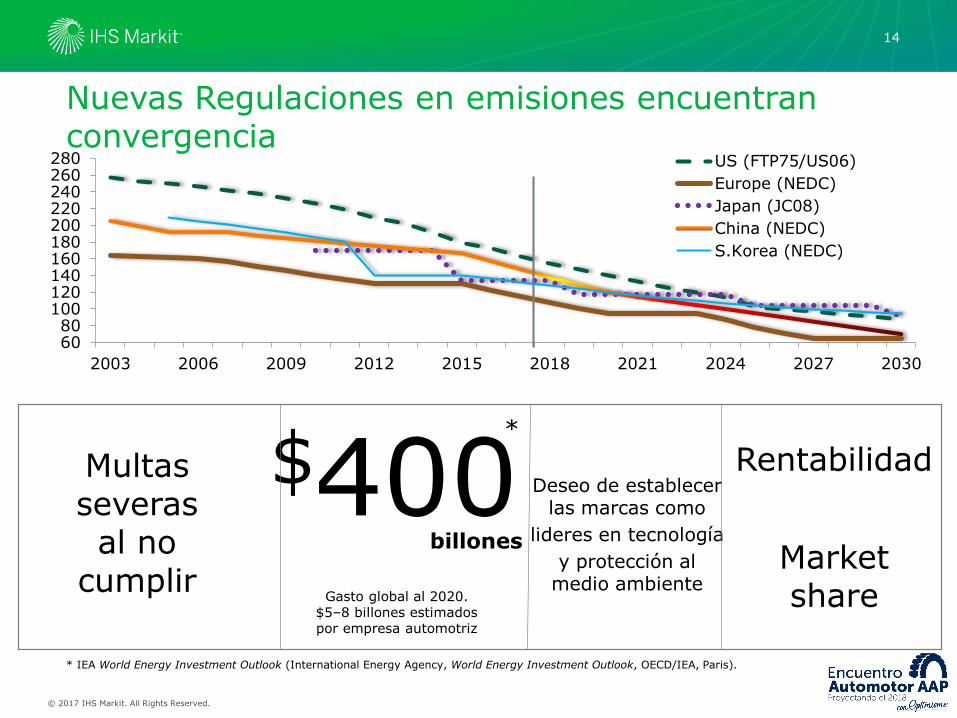

$400Gasto global al 2020.

$5–8 billones estimados por empresa automotriz

Multas severasal no

cumplir

billones

Deseo de establecerlas marcas como

lideres en tecnología

y protección al medio ambiente

Rentabilidad

Market share

*

* IEA World Energy Investment Outlook (International Energy Agency, World Energy Investment Outlook, OECD/IEA, Paris).

6080

100120140160180200220240260280

2003 2006 2009 2012 2015 2018 2021 2024 2027 2030

US (FTP75/US06)

Europe (NEDC)

Japan (JC08)

China (NEDC)

S.Korea (NEDC)

Nuevas Regulaciones en emisiones encuentran convergencia

14

© 2017 IHS Markit. All Rights Reserved.

15

Que es un ZEV?

Hydrogen fuel cell electric

vehicles (FCEVs)

Battery electric vehicles (BEVs)

Plug-in hybrid

vehicles (PHEVs)

Note: ZEV = zero emissions vehicle.

© 2017 IHS Markit. All Rights Reserved.

Disruptivo

–Toyota

–Honda

–Nissan

–Ford

–BMW

–Volkswagen

–Mazda

–Hyundai

– Lexus

–Audi

16

© 2016 IHS16

© 2017 IHS Markit. All Rights Reserved.

Photo By: Devin Lindsay

Productos

Evolucion de las Baterias

Infraestructura

Incentivos Gubernamentales

Precio del petroleo

Consumidor

Puntos Criticos

Photos by: Devin Lindsay

Source: Shutterstock

Source: Shutterstock

Source: ShutterstockSource: Shutterstock

17

© 2017 IHS Markit. All Rights Reserved.18

Ventas de Vehículos Ligeros en América LatinaMargen de error 2016 y perspectivas de crecimiento

18

Pais CY 2015 CY 2016 P'16 CY 2017 P'17 CY 2018 P'18

CY 2017

Dic16 MOE '17

Argentina 632,063 676,375 7.0% 859,548 27.1% 850,923 -1.0% 710,291 21.0%

Brazil 2,480,502 1,988,099 -19.9% 2,181,580 9.7% 2,455,054 12.5% 1,969,610 10.8%

Chile 283,497 304,626 7.5% 350,912 15.2% 365,930 4.3% 314,877 11.4%

Colombia 267,821 243,469 -9.1% 239,366 -1.7% 250,011 4.4% 247,472 -3.3%

Ecuador 72,117 68,969 -4.4% 100,969 46.4% 96,955 -4.0% 54,497 85.3%

Mexico 1,351,812 1,601,208 18.4% 1,550,959 -3.1% 1,575,090 1.6% 1,695,393 -8.5%

Peru 147,560 154,335 4.6% 171,350 11.0% 183,824 7.3% 162,531 5.4%

© 2017 IHS Markit. All Rights Reserved.

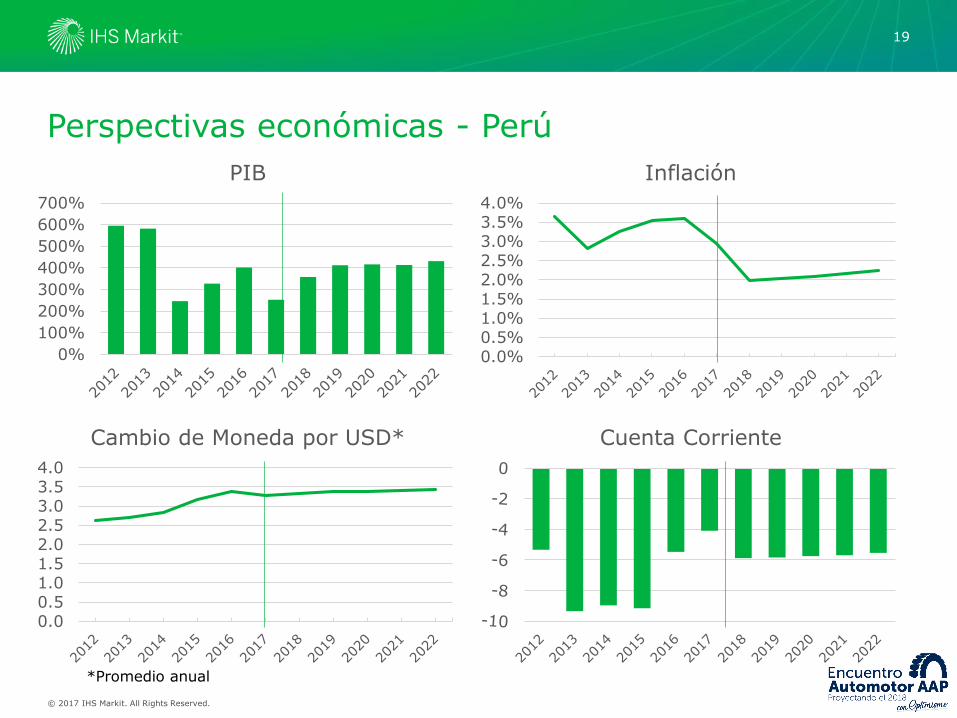

Perspectivas económicas - Perú

19

0%

100%

200%

300%

400%

500%

600%

700%

PIB

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

Inflación

0.00.51.01.52.02.53.03.54.0

Cambio de Moneda por USD* Cuenta Corriente

*Promedio anual

© 2017 IHS Markit. All Rights Reserved.

Venta de Vehículos Ligeros (SAAR) - Perú

20

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Miles

© 2017 IHS Markit. All Rights Reserved.

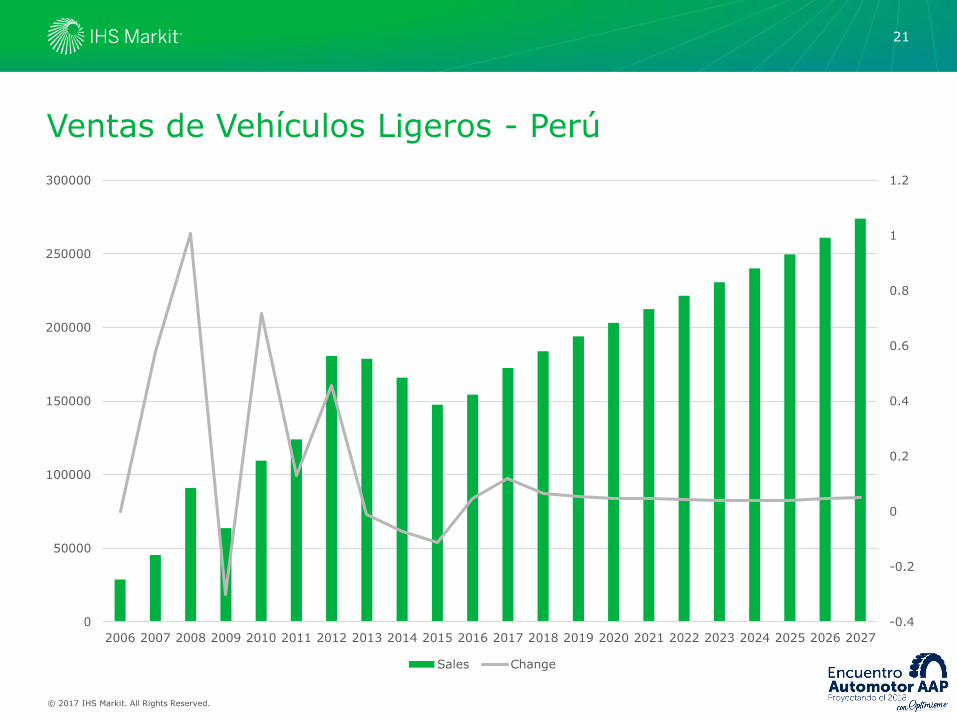

Ventas de Vehículos Ligeros - Perú

21

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

0

50000

100000

150000

200000

250000

300000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Sales Change

© 2017 IHS Markit. All Rights Reserved.

Marcas Mas Vendidas 2017

22

Hyundai Toyota Kia Chevrolet Nissan Suzuki MazdaVolkswage

nRenault Mitsubishi Others

2011 15.1% 28.0% 8.6% 7.5% 9.1% 5.6% 1.3% 5.0% 1.8% 1.8% 16.3%

2016 16.7% 18.8% 13.4% 4.8% 7.6% 6.0% 2.7% 2.4% 2.7% 2.4% 22.5%

2017 15.8% 15.3% 10.7% 7.2% 5.8% 5.7% 3.2% 3.0% 2.6% 2.3% 28.4%

2018 15.4% 15.9% 11.2% 6.3% 5.9% 5.3% 2.8% 2.6% 2.7% 1.8% 30.1%

0%

5%

10%

15%

20%

25%

30%

35%

© 2017 IHS Markit. All Rights Reserved.

Bodytype –SUVs sobrepasaron a sedanes

23

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

SUV Sedan Hatchback Van Pickup MPV Chassis-Cab Coupe Wagon Roadster Convertible

© 2017 IHS Markit. All Rights Reserved.

Peru LigerosHyundai

24

Source: IHS Automotive

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Hyundai 2017

Hyundai 2025

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Portfolio Age

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Grand i10 Accent Elantra i20 Tucson Others

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

0

5000

10000

15000

20000

25000

30000

35000

40000

Hyundai Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

Peru LigerosToyota

25

Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Toyota 2017

Toyota 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yaris Hilux RAV4 Avanza Corolla Others

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Toyota Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

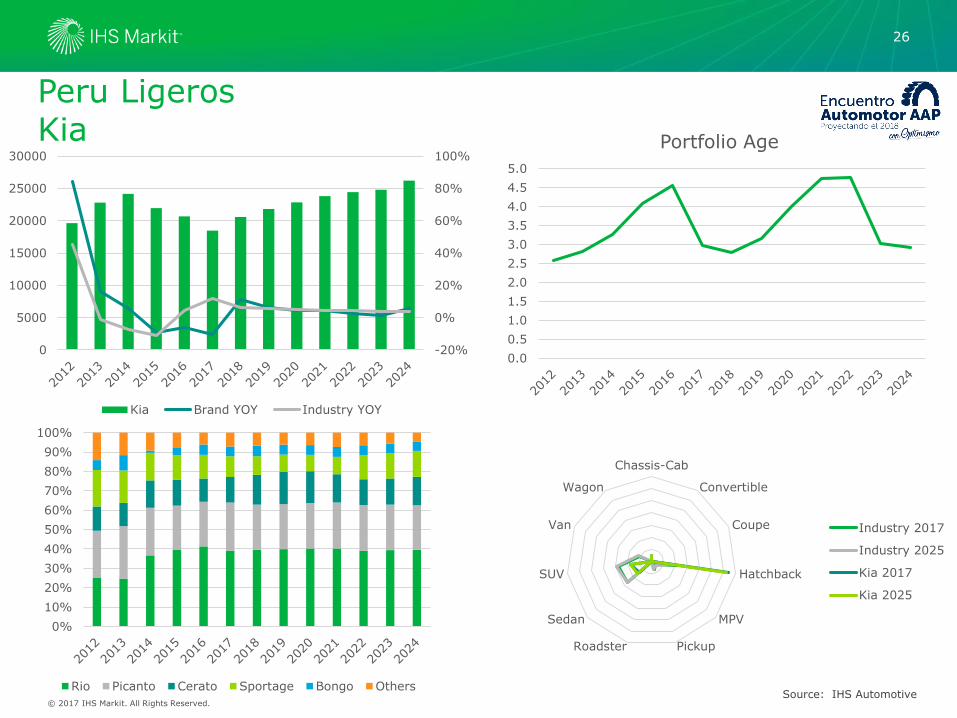

Peru LigerosKia

26

Source: IHS Automotive

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Kia 2017

Kia 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rio Picanto Cerato Sportage Bongo Others

-20%

0%

20%

40%

60%

80%

100%

0

5000

10000

15000

20000

25000

30000

Kia Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

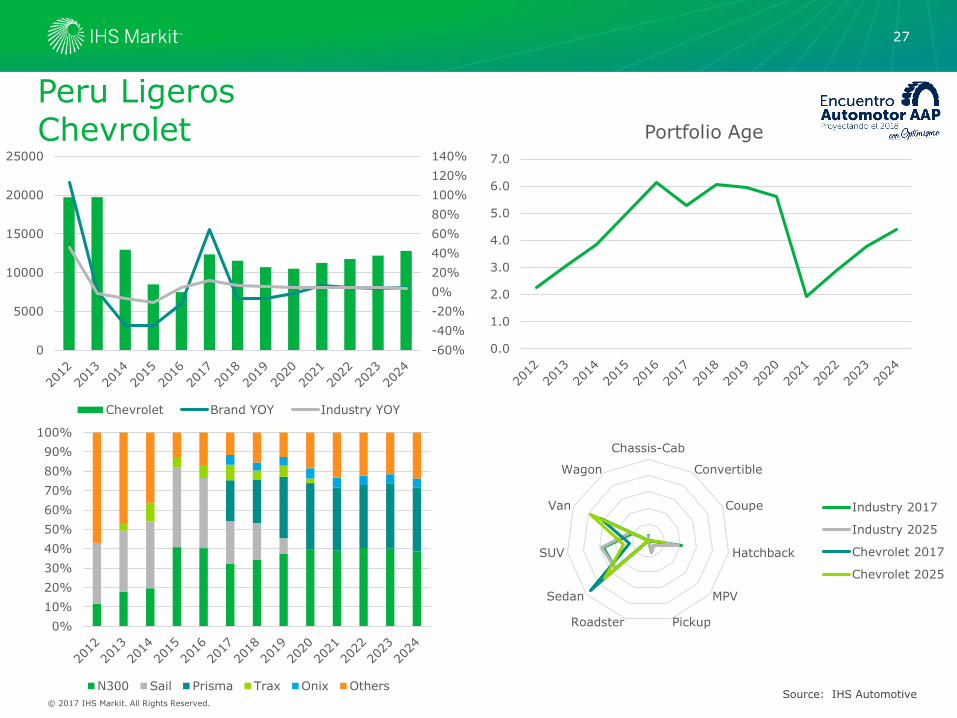

Peru LigerosChevrolet

27

Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Chevrolet 2017

Chevrolet 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

N300 Sail Prisma Trax Onix Others

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

0

5000

10000

15000

20000

25000

Chevrolet Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

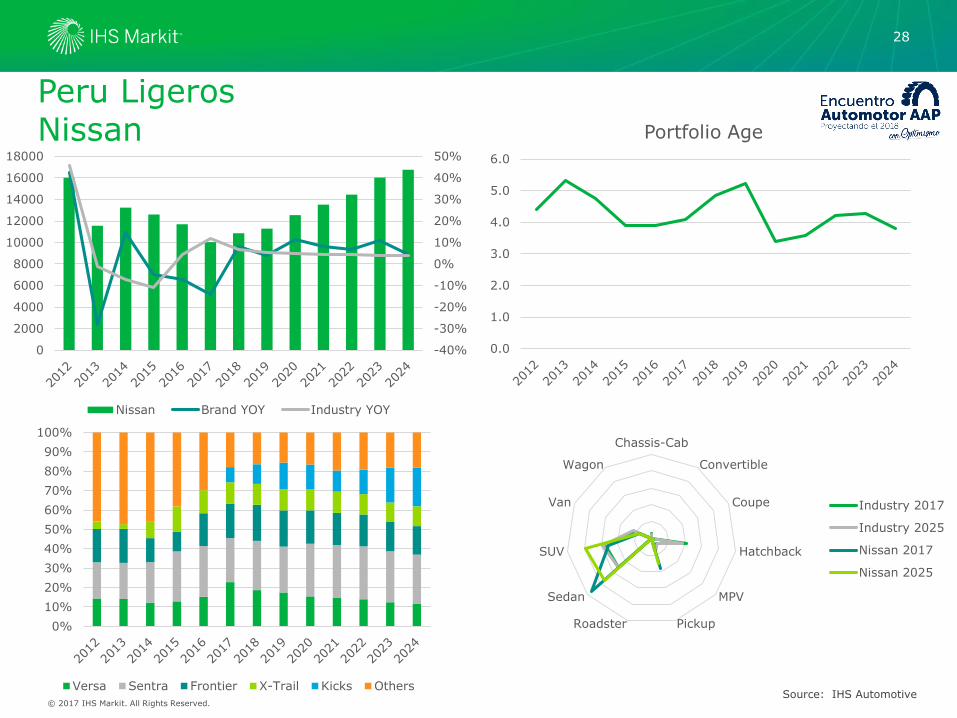

Peru LigerosNissan

28

Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Nissan 2017

Nissan 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Versa Sentra Frontier X-Trail Kicks Others

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

Nissan Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

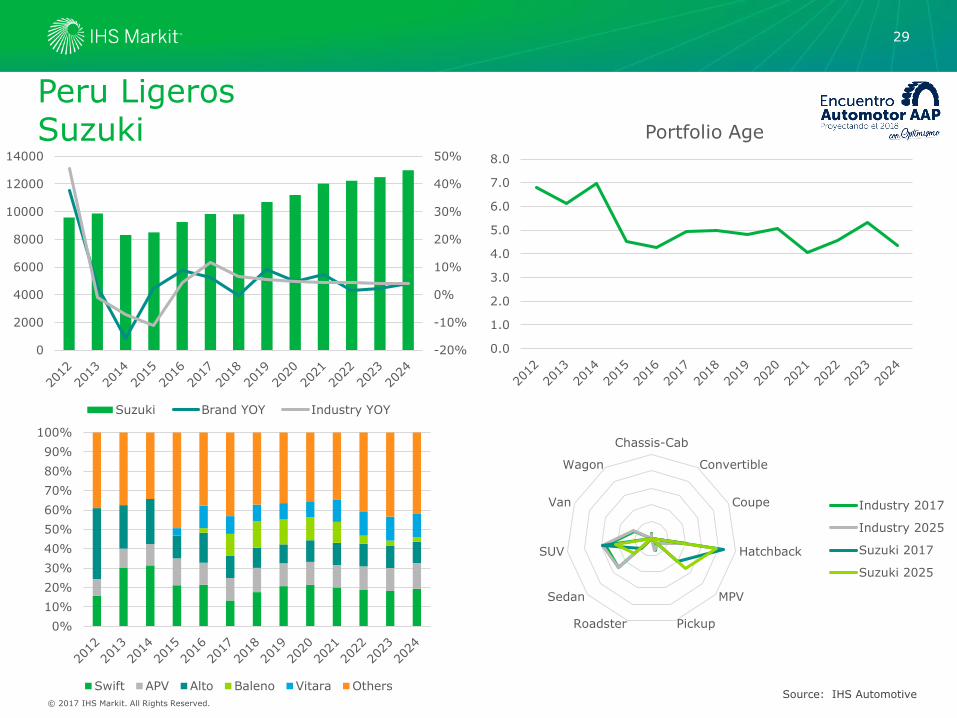

Peru LigerosSuzuki

29

Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Suzuki 2017

Suzuki 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Swift APV Alto Baleno Vitara Others

-20%

-10%

0%

10%

20%

30%

40%

50%

0

2000

4000

6000

8000

10000

12000

14000

Suzuki Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

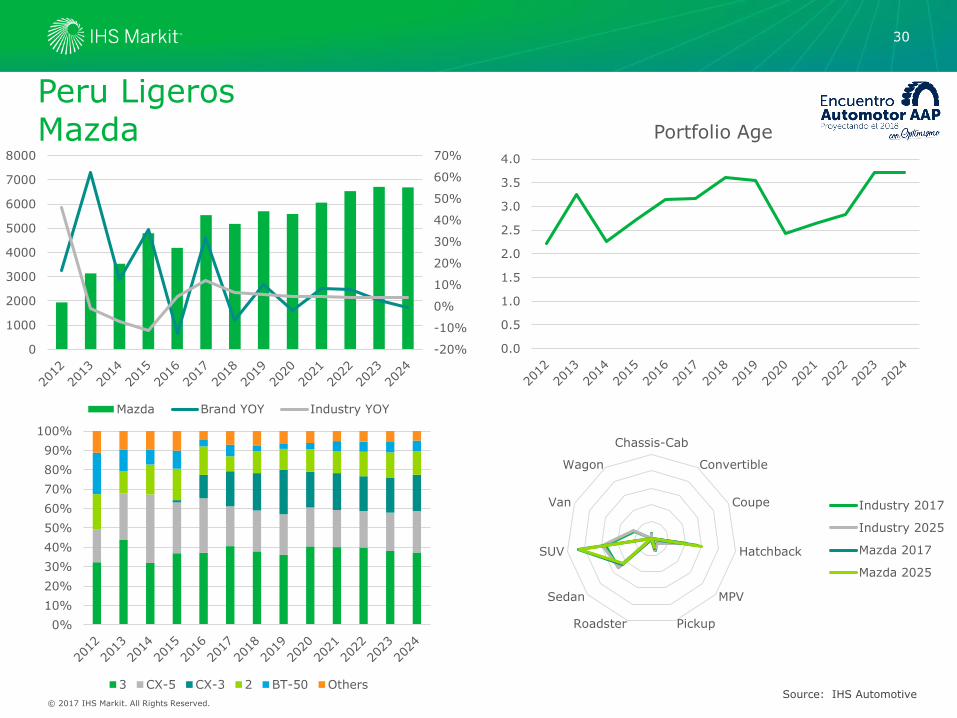

Peru LigerosMazda

30

Source: IHS Automotive

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Mazda 2017

Mazda 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3 CX-5 CX-3 2 BT-50 Others

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

0

1000

2000

3000

4000

5000

6000

7000

8000

Mazda Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

Peru LigerosVolkswagen

31

Source: IHS Automotive

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Volkswagen 2017

Volkswagen 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Gol Fox Amarok Jetta Polo Others

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

1000

2000

3000

4000

5000

6000

7000

8000

Volkswagen Brand YOY Industry YOY

© 2017 IHS Markit. All Rights Reserved.

Peru LigerosRenault

32

Source: IHS Automotive

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Portfolio Age

Chassis-Cab

Convertible

Coupe

Hatchback

MPV

PickupRoadster

Sedan

SUV

Van

Wagon

Industry 2017

Industry 2025

Renault 2017

Renault 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Duster Logan Duster Oroch Master Sandero Others

-20%

-10%

0%

10%

20%

30%

40%

50%

0

1000

2000

3000

4000

5000

6000

7000

Renault Brand YOY Industry YOY

IHS MarkitTM COPYRIGHT NOTICE AND DISCLAIMER © 2016 IHS Markit.

No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS Markit. Content reproduced or redistributed with IHS Markit permission must display IHS Markit legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions and analyses that are based upon it, and to the extent permitted by law, IHS Markit shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially from forecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at your own risk. IHS Markit and the IHS Markit logo are trademarks of IHS Markit.

IHS Markit Customer Care:

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Thank you! Muchas Gracias! Muito Obrigado!

Guido Vildozo, Senior Manager, Americas